Alfio Manciagli/iStock through Getty Photographs

The Q1 Earnings Season for the Gold Miners Index (GDX) has lastly begun, and the primary firm to report is Newmont (NYSE:NEM). From a headline standpoint, gold manufacturing was 8% decrease, however this was not stunning given the decrease Nevada manufacturing pre-reported by Barrick (GOLD). Happily, the next gold worth picked up a number of the slack, and whereas prices had been up within the interval, Newmont maintained stable AISC margins. At a share worth of $78.00, I see restricted short-term upside for Newmont from present ranges. Nonetheless, given its high-quality enterprise mannequin and enticing yield, I’d view sharp pullbacks as shopping for alternatives.

Newmont – Nevada Gold Mines Operations (Barrick Gold Presentation)

This week, Newmont launched its Q1 outcomes, reporting quarterly manufacturing of ~1.34 million ounces of gold and ~350,000 gold-equivalent ounces [GEOs]. This translated to an 8% decline in gold manufacturing and a ten% enhance in GEO gross sales, with greater GEO gross sales helped by higher grades on the firm’s huge Boddington and Penasquito mines. Whereas the outcomes might seem disappointing, with whole manufacturing down year-over-year, these outcomes are passable, for my part. It is because they’re monitoring roughly in keeping with steerage regardless of headwinds introduced on by Omicron, which led to elevated absenteeism ranges for some miners which have pre-reported their outcomes. Let’s take a better look under:

Manufacturing

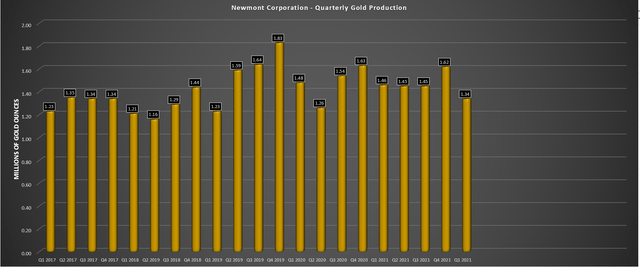

Wanting on the chart under, we will see that Newmont’s quarterly gold manufacturing dipped 8% year-over-year to ~1.34 million ounces of gold, its lowest quarter of manufacturing since Q2 2020, which was severely impacted by COVID-19. Nevertheless, whereas this was definitely a weaker quarter, Newmont virtually stole the remaining ~48% curiosity within the Yanacocha Mine, for my part, paying simply over$100/ozon gold reserves and fewer than 0.50x NPV (5%) at spot costs, whereas choosing up all of the upside without cost.

Newmont Quarterly Gold Manufacturing (Firm Filings, Writer’s Chart)

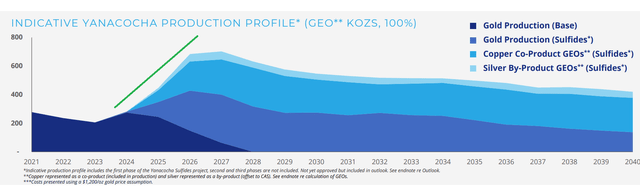

Whereas this may present a slight elevate in manufacturing this yr primarily based on its elevated possession (~48% – 100%) of the mine, it is going to present a large enhance in manufacturing later this decade. Notably, this manufacturing upside will come at industry-leading prices, with the mission anticipated so as to add 500,000+ GEOs each year at all-in sustaining prices under $800/oz (2027-2031). In the meantime, there may be the potential to increase the mine life nicely past 2040 with its second and third phases, and Yanacocha will even add copper manufacturing. Added publicity to this metallic later this decade will present a pleasant enhance to Newmont’s manufacturing combine when copper costs proceed to hover above $4.50/lb.

Yanacocha Manufacturing Profile (Firm Presentation)

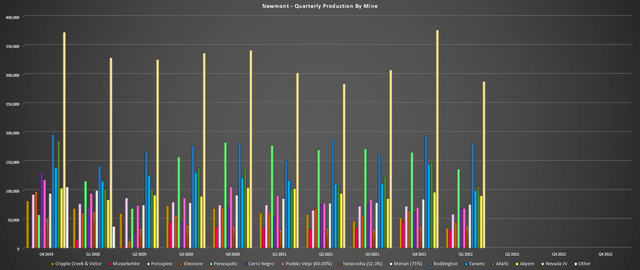

Circling again to the gold operations, all of Newmont’s operations noticed decrease manufacturing in Q1 on a year-over-year foundation, apart from its Boddington Mine in Australia and Cerro Negro in Argentina. At Cripple Creek & Victor in Colorado, manufacturing fell sharply to only ~35,000 ounces attributable to decrease leach pad recoveries and fewer ore milled as a result of mill shut down and non permanent idling within the present yr.

In Canada, at Musselwhite, Porcupine, and Eleonore, manufacturing fell greater than 10% at every asset associated to labor shortages attributable to COVID-19 (Musselwhite), decrease grades and throughput (Porcupine), and decrease grades and a construct of in-circuit stock in comparison with a drawdown within the prior yr (Eleonore). Transferring south to Mexico at Penasquito, manufacturing was 23% decrease attributable to decrease grades and decrease restoration charges, partially offset by greater GEO manufacturing attributable to elevated mill throughput.

Newmont – Quarterly Manufacturing by Mine (Firm Filings, Writer’s Chart)

Elsewhere, in South America, manufacturing has rebounded properly at Cerro Negro following a troublesome FY2020 attributable to COVID-19 headwinds, with 4 consecutive quarters of 60,000+ ounces produced. In Q1, the upper manufacturing (68,000 ounces vs. 56,000 ounces) was helped by greater grades milled. Nevertheless, this was largely offset by a a lot weaker quarter at Merian, with decrease mill throughput and a drawdown of in-circuit stock offsetting the upper grades within the interval.

Lastly, taking a look at two of the corporate’s two largest areas, Australia and the USA, outcomes had been combined. In Australia, Boddington had an distinctive quarter, with manufacturing coming in at 182,000 ounces of gold, helped by greater grades, whereas GEO manufacturing additionally elevated meaningfully. Nevertheless, Tanami noticed a 15% decline in manufacturing attributable to decrease throughput, with simply 100,000 ounces produced in Q1.

Nevada Gold Mines Operations (Barrick Presentation)

In the meantime, at Nevada Gold Mines LLC, the joint-venture between Barrick and Newmont, Newmont’s attributable manufacturing got here in at simply ~288,000 ounces, down from ~303,000 ounces in Q1 2021. As mentioned in my latest Barrick replace, decrease manufacturing was associated to deliberate upkeep at Turquoise Ridge. On a sequential foundation, the sharp decline in manufacturing (~288,000 ounces vs. ~377,000 ounces) on the Nevada operations was associated to the depletion of stockpiled high-grade underground ore that was processed in This fall following the mechanical mill failure final yr.

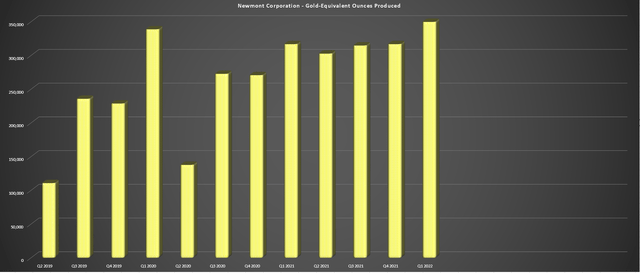

Newmont – Quarterly GEO Manufacturing (Firm Filings, Writer’s Chart)

Happily, whereas gold manufacturing was decrease, GEO manufacturing from co-products elevated meaningfully (350,000 vs. 317,000 ounces) and continues to pattern greater, a constructive signal. This was associated to greater manufacturing at each Boddington and Penasquito, with Boddington’s GEO manufacturing growing almost 60% to 51,000 GEOs in Q1 2022. When factoring within the 10% enhance in GEO manufacturing, Newmont’s whole manufacturing in Q1 was down roughly 5% to ~1.68 million ounces vs. ~1.77 million ounces in Q1 2021.

Prices and Margins

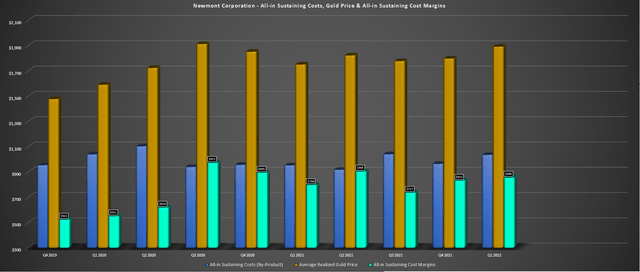

Transferring over to prices, Newmont’s all-in sustaining prices per gold ounce got here in at $1,156/ozvs. $1,039/ozwithin the year-ago interval, a greater than 11% enhance. On a by-product AISC foundation, we additionally noticed a pointy enhance with prices growing to $1,036/ozfrom $936/ozin Q1 2021. A few of that is associated to inflationary pressures, with rising gasoline, consumables, and labor prices pushing prices greater for almost all operations. This has not been helped by the rising diesel costs, that are up excessive double-digits on a year-over-year foundation.

Nevertheless, like different multi-million-ounce producers, Newmont differentiates itself. It is because it, and others, profit from economies of scale, the power to take a position aggressively in know-how and innovation, and enormous provider networks that place it in a greater place than its smaller friends to claw again any margin losses over the subsequent few years. Some examples embrace pushing ahead high-margin initiatives like Ahafo North with 300,000 ounces each year of contribution in 2024 at sub $700/ozcosts and investments in issues like Autonomous Haulage at Boddington, and plenty of different initiatives being thought of to make operations leaner.

Newmont – All-in Sustaining Prices & AISC Margins (Firm Filings, Writer’s Chart)

Happily, whereas prices had been up, the gold worth was additionally up sharply in Q1, coming in at $1,892/oz, a greater than $110/ozincrease from $1,751/ozwithin the year-ago interval. This helped Newmont report slight margin enlargement on a year-over-year foundation, with AISC margins (by-product foundation) coming in at $856/oz, up from $798/ozin Q1 2021. Given the power within the gold worth in Q2, and assuming the metallic can keep above $1,900/ozfor the rest of the quarter, we must always see one other quarter of margin enlargement, with a mean realized gold worth that is more likely to be a minimum of $100/ozhigher within the Q2 outcomes (~$1,925/ozvs. ~$1,823/oz).

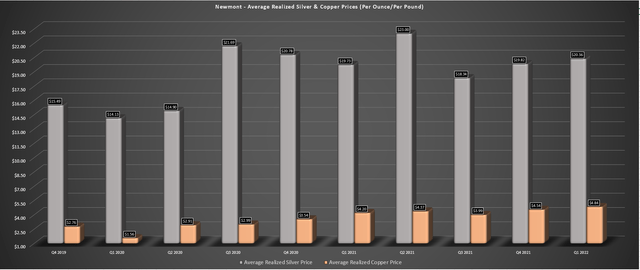

Newmont – Common Realized Silver/Copper Costs (Firm Filings, Writer’s Chart)

Lastly, if we take a look at the corporate’s common realized silver, copper, and zinc costs, these are additionally trending in the fitting route, with copper coming in at $4.84/pound and silver coming in at $20.36/oz. The main winner was zinc, although, which at the moment sits close to $2.00/pound and clocked in at $1.75/pound in Q1 2021. Assuming power in these metals continues from property like Penasquito, this could assist with prices with greater by-product credit from lead, zinc, and silver in a position to offset inflationary pressures, which look to be a minimum of a 5% headwind this yr.

Medium-Time period Outlook

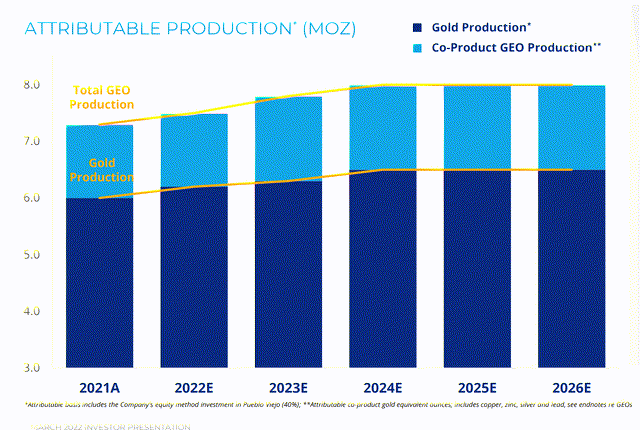

Newmont’s medium-term outlook, there is likely to be some cause to be much less optimistic given the price will increase if the outlook was for flat to declining manufacturing with little room to claw again prices. Nevertheless, as famous, Newmont is predicted to see rising manufacturing over the subsequent a number of years, even when it is solely a reasonable enhance, helped by new initiatives just like the Tanami Enlargement, elevated manufacturing from Yanacocha as a result of consolidation of the asset, and Ahafo North. There’s additional upside from the Cerro Negro District Enlargement and Yanacocha Sulfides, with each initiatives additionally anticipated to have industry-leading prices.

Newmont – 5-Yr Outlook (Firm Presentation)

Lastly, whereas Newmont did not develop reserves year-over-year if we exclude the non-organic progress from its consolidation of Yanacocha, it did maintain the road kind of. This was a stable achievement, on condition that it maintained its conservative gold worth assumption of $1,200/ozto calculate reserves.

With Newmont having a steadiness sheet that may simply assist upwards of $300 million in exploration per yr, a powerful growth pipeline, and the power to meaningfully enhance reserves simply by adjusting to a $1,400/ozgold worth, which remains to be extraordinarily conservative, I do not see any cause to fret about Newmont’s long-term manufacturing outlook.

Monetary Outcomes

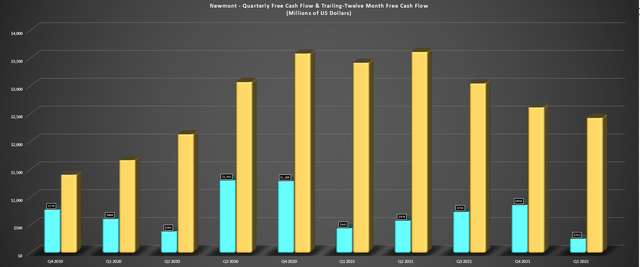

Whereas Newmont reported income of ~$3.02 billion, up 5% year-over-year, free money circulation fell to only $252 million, a greater than 40% decline from the year-ago interval. This was associated to greater capital expenditures and decrease working money circulation, and it additionally dragged down Newmont’s trailing twelve-month free money circulation to only ~$2.4 billion. Nevertheless, with manufacturing being back-end weighted and the gold worth definitely being a tailwind, I’d count on to see a major enchancment in free money circulation era because the yr progresses.

Newmont – Quarterly & Trailing-Twelve-Month Free Money Stream (Firm Filings, Writer’s Chart)

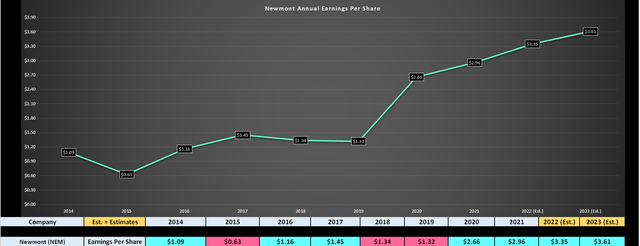

Transferring over to earnings, Newmont reported quarterly earnings per share [EPS] of $0.69 vs. $0.74 final yr, which was somewhat disappointing. Nevertheless, assuming the gold worth can proceed to hang around above the $1,900/ozlevel, Newmont ought to be capable to report a minimum of $3.35 in annual EPS this yr, which might translate to greater than 10% progress on a year-over-year foundation for the second consecutive yr, and after lapping 100% progress ($2.66 vs. $1.32) in FY2020. Waiting for FY2023, I’d not be stunned to see annual EPS are available in north of $3.60. So, whereas it is simple to get hung up on the decline in quarterly EPS in Q1, the earnings pattern nonetheless stays fairly stable on an annual foundation regardless of this miss.

Newmont – Annual Earnings Pattern & Ahead Estimates (Firm Filings, Writer’s Chart)

Valuation

Primarily based on ~800 million shares excellent and a share worth of $78.00, Newmont is the biggest gold producer by a large margin, valued at ~$62.4 billion. This premium valuation definitely is sensible when contemplating that Newmont produces considerably extra gold than its peer group (~6.0 million ounces each year) and has a declining price profile over the subsequent few years. As well as, the corporate has a large growth pipeline, which incorporates Espresso, Akyem Underground, plus Cerro Negro District Expansions on the gold facet, in addition to Saddle North, and its Galore Creek Norte Abierto and Nueva Union joint-ventures on the copper facet.

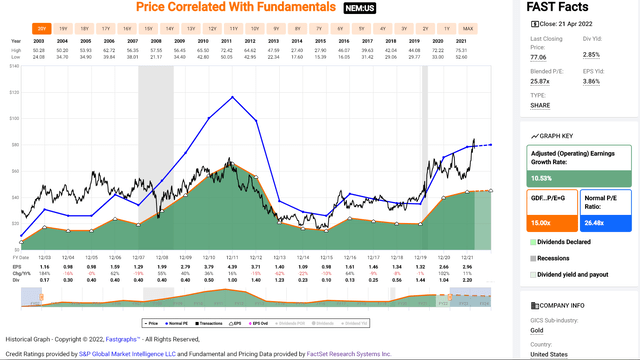

Nevertheless, whereas the corporate has no friends from a dimension standpoint and has a high-quality enterprise predominantly targeted on Tier-1 jurisdictions, the inventory is trying pretty valued after its greater than 45% rally. It is because the inventory is now buying and selling at ~21.6x FY2023 earnings estimates, which is barely above what I consider to be a conservative earnings a number of of 21, pointing to a conservative truthful worth of $75.80. The truth that Newmont is buying and selling simply above conservative truthful worth doesn’t suggest that it could actually’t head greater, however it is going to want extra assist from the gold worth to justify this or a lift to internet asset worth by means of an acquisition.

Newmont – Historic Earnings A number of (FASTGraphs.com)

Some traders may argue that with the gold worth buying and selling within the higher portion of its 20-year vary, Newmont can simply justify an earnings a number of nearer to its historic common of 26. Whereas I do not disagree with this, I desire to be conservative with my worth targets to construct a significant margin of security into any new purchases and restrict drawdowns as a lot as potential. So, whereas I feel Newmont is well a top-5 gold producer and a staple for a valuable metals portfolio, I proceed to see the inventory as a Maintain and at the moment favor million-ounce producers like Agnico Eagle (AEM) that commerce at a reduction to truthful worth.

Technical Image

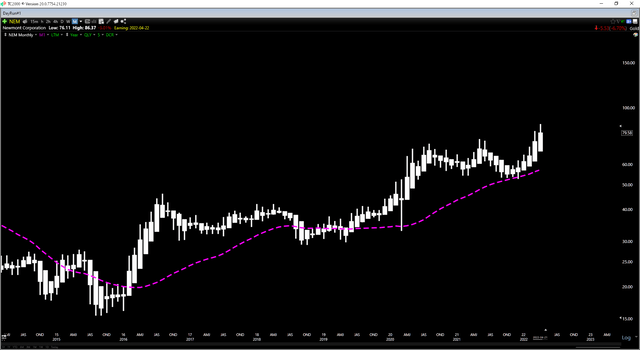

Transferring to the technical image, the under month-to-month chart corroborates that Newmont is nowhere close to a low-risk purchase zone, with the inventory now greater than 30% above its month-to-month shifting common (pink line). I desire to purchase Newmont inside 5% of this long-term assist degree, and this space got here in at $58.00 or decrease after I highlighted the inventory a number of occasions final yr. So, for Newmont to turn out to be extra fascinating from a technical standpoint, this shifting common might want to play some catch-up, or Newmont might want to appropriate a minimum of one other 15% to maneuver nearer to this shifting common.

Newmont – Month-to-month Chart (TC2000.com)

The excellent news is that with this shifting common rising and Newmont making all-time highs, it is one of many few S&P-500 (SPY) shares in a transparent weekly and month-to-month uptrend, suggesting an growing chance of sharp pullbacks being purchased up. In the meantime, traders that bought under $58.00 are sitting on a virtually 4% yield on price, boosting returns even when the inventory does undergo a interval of consolidation to arrange one other base for greater costs down the highway. Given this industry-leading dividend yield and favorable technical outlook from a long-term standpoint, I proceed to carry a place within the inventory.

Newmont Gold Pour (Firm Presentation)

Newmont’s had a passable Q1 report, producing ~1.34 million ounces of gold and benefited from a lot greater metals costs within the interval. Nevertheless, with the inventory working up significantly into the report, I’d argue that even a beat was priced into the inventory, which didn’t favor being obese the inventory heading into the report. The excellent news is that with a positive outlook for gold, given the place of actual charges, and an enhancing price profile with rising manufacturing, Newmont has a really vibrant future. So, if we had been to see some weak point in what’s seasonally a softer interval for miners, I’d view sharp pullbacks within the inventory as shopping for alternatives.

")

")

{kind=link}