Joe Hendrickson

Based in 1963, Portillo’s Inc. (NASDAQ:PTLO) operates eating places that serve Chicago-style scorching canine, in addition to grilled burgers, beef sandwiches, and different meals objects. The corporate has continued increasing its restaurant chain nationwide throughout america, displaying fixed good income development.

The corporate’s post-IPO inventory efficiency after the 2021 IPO has been poor, because the inventory has misplaced over two thirds of the worth from its preliminary buying and selling. After the inventory has had such a weak run amid Portillo’s continued nationwide growth, activist agency Engaged Capital has now taken curiosity within the restaurant chain to show the growth technique round.

Inventory Chart From IPO (Looking for Alpha)

Portillo’s Is Rising Ambitiously, However With Too Heavy Capital Investments

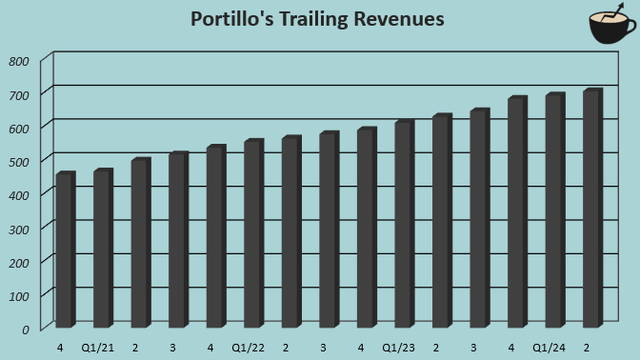

After the IPO, opposite to what the inventory worth suggests, Portillo’s has continued increasing its restaurant footprint with wholesome working earnings. After the firm had a complete of 69 areas on the finish of 2021, primarily situated in Illinois, the corporate has expanded into a complete of 85 areas on the finish of Q2 2024 with new growth being primarily exterior of the Illinois market the place Portillo’s was based. Revenues have grown at a CAGR of 8.9% from 2019 to the Q2 2024 trailing revenues of $702.4 million, with wholesome same-restaurant gross sales development.

The expansion has been achieved with largely wholesome profitability, as Portillo’s present working margin trails at 8.1% with working earnings of $56.6 million. The margin remains to be beneath the 2019 working margin of 10.1% primarily on account of increased pre-opening prices at a trailing $9.9 million, however has expanded healthily from Covid-time margins with slowing inflation and normalized visitors.

The not too long ago reported Q2 comparable gross sales development got here in at only a weak -0.6%, however appears to be associated extra to weak trade visitors as a substitute of Portillo’s-specific points.

Writer’s Calculation Utilizing TIKR Knowledge

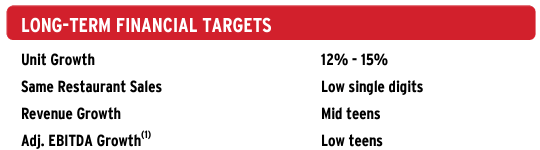

The achieved development is barely the beginning of Portillo’s formidable targets. The corporate targets 12-15% annual unit development with 10+ new items being developed in 2024 alone, totaling for a complete mid-teens annual income development goal when mixed with the gradual same-restaurant gross sales development goal – with solely 85 areas excellent, Portillo’s remains to be fairly a small chain with publicity being largely in Illinois, enabling it for a protracted development runway.

PRTO Q2 Investor Presentation

Whereas Portillo’s development has been good up to now, the inventory hasn’t appreciated with the restaurant community growth. The explanation might depend on Portillo’s capital heavy growth the place the corporate develops its personal actual property – capital expenditures reached $87.9 million in 2023 with the same capital expenditure steering for 2024, pushing money flows unfavourable regardless of wholesome earnings. The heavy actual property growth has additionally weakened capital effectivity significantly right into a present low 6.9% return on fairness, not making the present growth very accretive to traders.

The heavy growth technique has additionally prompted dilution and compelled Portillo’s to tackle important debt, with a present $305.1 million of whole curiosity bearing debt standing on the corporate’s steadiness sheet. Weighted excellent shares have elevated from 35.8 million in 2021 into at the moment trailing 57.5 million.

With the restaurant trade’s fairly cyclical earnings nature and immense competitors, the present quantity of debt is unhealthy, though I do consider that the present actual property portfolio can nonetheless assist such debt with potential sale-and-leasebacks.

Engaged Capital Takes a Stake in Portillo’s

Just lately, activist agency Engaged Capital was introduced to have taken a stake in Portillo’s, sending the refill reasonably. The transfer from the activist investor agency may very well be important for Portillo’s – typical for activist traders, Engaged Capital’s technique revolves round sustaining a very good possession of an organization (at the moment almost 10% of Portillo’s), and pushing for operational adjustments to in the end drive shareholder worth from a long-term proprietor’s perspective. The agency can also be recognized for its profitable turnaround efforts with Shake Shack (SHAK).

Whereas Engaged Capital isn’t pursuing for management adjustments, CNBC’s report on the matter showcases a number of the operational adjustments that Engaged Capital has recognized with Portillo’s. Most notably, the activist funding agency is pushing for a unique growth funding technique – relatively than spending immense quantities of capital on creating company-owned actual property, showcased by Portillo’s present $85-88 million capital expenditure steering for 2024, Engaged Capital is pushing for extra agile growth. Engaged Capital believes that mixed, lighter actual property investments and smaller new location sizes might in the end double new eating places’ cash-on-cash returns from 25% to 50%. With the lighter growth mannequin, Engaged Capital is pushing for accelerated nationwide growth.

I consider that Engaged Capital’s involvement is superb for Portillo’s. Whereas I’ve been bearish on Shake Shack on account of its extremely excessive valuation, the activist agency’s involvement has pushed enhancements within the firm’s earnings. The proposed, smaller-location growth technique for Portillo’s additionally appears to make sense for an informal eating scorching canine & sandwich restaurant chain, and as capital expenditures have ballooned on account of costly actual property growth. A lighter growth technique might additionally put an finish to Portillo’s fairly excessive prior dilution.

Portillo’s administration’s and board’s reception of the proposed turnaround remains to be unknown, however as per CNBC’s sources, Engaged Capital’s and Portillo’s administration’s conversations have up to now been constructive – I consider that Engaged Capital’s engagement ought to put ahead at the very least some adjustments.

Engaged Capital believes that with its solutions applied, the inventory may very well be value at the very least 100% greater than it’s at the moment.

PRTO Inventory Valuation

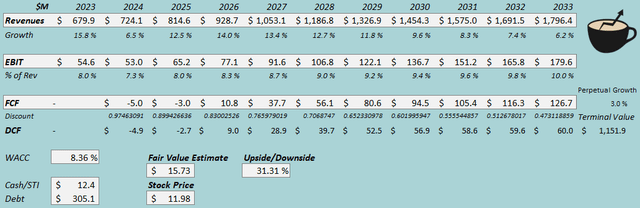

I constructed a reduced money stream [DCF] mannequin for Portillo’s to estimate a good worth for the inventory. Within the mannequin, I account for adjustments within the firm’s growth technique as urged by Engaged Capital.

For income development, I estimate a CAGR of 10.2% from 2023 to 2033 and three.0% perpetual development afterwards, nonetheless trailing from Portillo’s personal long-term goal degree as I consider that some conservatism is due. The income estimates might nonetheless effectively become too low, particularly if Engaged Capital’s accelerated, agile development technique is applied effectively.

I estimate the EBIT margin to slowly climb again into 10.0%, close to the corporate’s pre-pandemic 10.1% degree. The margin ought to, in my view, broaden effectively via higher mid-term visitors with an trade restoration from an ultimately higher shopper sentiment, in addition to nice working leverage from bigger operations that permit for extra environment friendly advertising and marketing, sourcing, and company prices. Additionally, the slowing development ought to push down Portillo’s at the moment significantly excessive pre-opening value degree, probably permitting for the ten.0% estimate in the long run regardless of much less owned actual property growth within the estimates.

By means of the corporate’s traditionally nice working capital administration, I consider that Portillo’s has the prospect for a very good money stream conversion even amid aggressive growth, if the corporate strikes to the extra agile growth technique that Engaged Capital suggests – the DCF mannequin contains the idea that Portillo’s strikes extra onto rented properties in its development technique in upcoming years, slowly enhancing the conversion.

DCF Mannequin (Writer’s Calculation)

The estimates put Portillo’s truthful worth estimate at $15.73, 31% above the inventory worth on the time of writing – I consider that if Engaged Capital’s solutions undergo, the inventory might lastly have seen a backside and may very well be a gorgeous funding alternative.

The income estimates might additionally become too conservative within the DCF mannequin if Portillo’s development technique picks up higher than anticipated.

CAPM

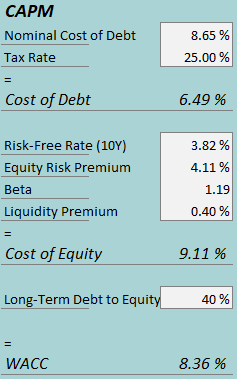

A weighted common value of capital of 8.36% is used within the DCF mannequin. The used WACC is derived from a capital asset pricing mannequin:

CAPM (Writer’s Calculation)

In Q2, Portillo’s had $6.6 million in curiosity bills, making the corporate’s rate of interest 8.65% with the present quantity of interest-bearing debt. I estimate fairly a excessive 40% long-term debt-to-equity, as Portillo’s leverages fairly a excessive quantity of debt.

To estimate the price of fairness, I exploit the 10-year bond yield of three.82% because the risk-free price. The fairness threat premium of 4.11% is Professor Aswath Damodaran’s estimate for the US, up to date in July. I exploit Aswath Damodaran’s restaurant trade beta estimate of 1.19 for Portillo’s. With a liquidity premium of 0.4%, the price of fairness stands at 9.11% and the WACC at 8.36%.

Takeaway

Portillo’s has grown its restaurant footprint at a very good tempo, however the inventory hasn’t appreciated with the chain’s development, as heavy actual property growth investments and its required financing have made the growth weakly accretive to traders with a poor return on invested capital. Engaged Capital, an activist investor agency, has now taken discover of the underperforming development technique and is pushing for adjustments within the technique into extra agile growth, being an amazing issue in my view. With much less actual property growth and smaller unit sizes, the restaurant chain’s underlying worth may very well be surfaced higher, probably making the inventory a gorgeous funding on the at the moment low inventory worth. As such, I provoke Portillo’s with a Purchase ranking.

")

{kind=link}