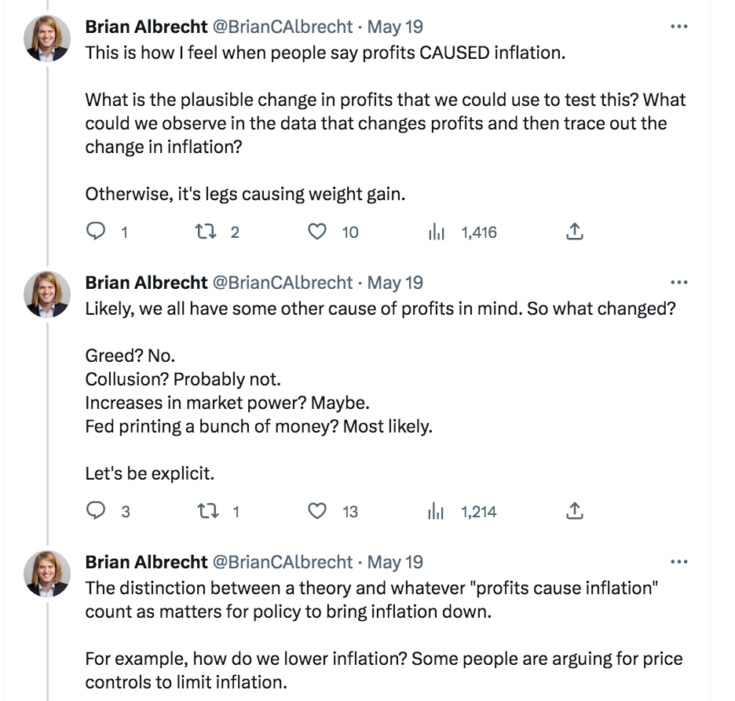

Brian Albrecht has a clever series of tweets comparing inflation and weight gain:

After a sarcastic comment about cutting off legs to lose weight, Albrecht then draws some policy implications:

I’d like to take this analogy a bit further. I can imagine a few cases where it might make sense to attribute weight gain to a specific part of the body. Suppose all of the weight gain occurred in the lower torso, due to a cancerous tumor. In that case, a doctor might recommend that the patient not try to lose weight in other parts of the body to offset the gain in the lower torso. In that case, it might make sense to speak of a tumor as causing weight gain.

In most cases, however, weight gain is caused by eating too much food (combined with not enough exercise.)

Most serious bouts of inflation are caused by excessive aggregate demand—excessively rapid growth in nominal GDP. This is equivalent to excessive consumption of food. In some cases, however, brief periods of inflation can occur due to problems in a specific area of the economy, without any increase in NGDP. An oil shock might raise prices and lower output by an equal amount. Increasingly monopolistic corporations might reduce output to drive up prices. Increasingly powerful labor unions might reduce the total workforce to drive up wages.

In that case, a “monetary doctor” might suggest not offsetting price increases in one sector with deflation in another. Instead, it might be better to allow a temporary rise in inflation, as long as NGDP growth remains on track. This would be like allowing some weight gain from a tumor.

Of course that doesn’t mean that a tumor is not a problem, rather that dieting is not the optimal solution to cancer. Instead, you might try radiation or chemotherapy. Similarly, my claim is not that supply shocks are not a problem; rather the claim is that the resulting rise in the CPI is in some sense optimal, given the existence of the supply problem. You may wish to use other policy tools to boost aggregate supply.

I see a lot of confusion when people speak of inflation being caused by “supply bottlenecks”, or “greed”, or “rising wages”, or “budget deficits”, or “currency depreciation”. What are the relevant policy counterfactuals? What do you mean by “cause”? Just because prices rise before wages doesn’t imply that prices cause wages.

This is from a recent paper by Norbert Michel and Jai Kedia:

Beyond these simple comparisons of percentages, more sophisticated research suggests that there is little reason to expect monetary policy to have much of an effect on prices in the services industry. As a Cato study using a VAR technique finds, Fed policy has hardly mattered in explaining inflation (services or otherwise). Figure 1 below reproduces the breakdown of inflation into its demand, supply, and monetary policy components from 1960 onwards. As the graph shows, supply factors dominate – they account for over 80% of the variation in service‐sector inflation, both in the short‐term and long‐term. In the near term, monetary policy explains less than 2% of inflation. In the longer term, the effects increase but never account for more than 5% of service‐sector inflation.

VAR studies aren’t going to tell you anything about inflation causation, at least in any commonsense meaning of the term “cause”.

In my view, almost all of the inflation since 1960 has been due to monetary policy. If real GDP grows at 3% since 1960, and nominal GDP grows at 7%, then you’ll have a 4% average inflation rate. Monetary policy drives NGDP growth, and hence explains the excess of NGDP over RGDP growth. With less expansionary monetary policy we would have had less inflation (both total and services.) Furthermore, monetary policy is not an alternative theory to “demand”, it’s what determines demand. Once you’ve isolated the supply and demand “components”, there’s nothing left.

Brian Albrecht is exactly right when he suggests that in economics it’s most useful to think of causation in terms of policy counterfactuals:

I don’t want to get into semantic disputes, but a theory of inflation should be *causal*. A causes inflation generally. B caused inflation here. At the heart of causation is the counterfactual. If X had been different, then Y would have been different.

It’s theoretically possible that our recent inflation was caused by something other than monetary policy, such as increased greed, or increasingly powerful labor unions. But it just so happens that the recent overshoot of NGDP growth is quite similar to the recent overshoot of inflation. That means that in this case the cause is simply “overeating”, no need to search out mysterious “tumors” in the body.

My daughter recently sent me a San Francisco Fed paper by Adam Hale Shapiro looking at the effect of wage inflation on overall inflation. The abstract suggests little impact:

Labor-cost growth has no meaningful effect on goods or housing services inflation. Overall, labor-cost growth is responsible for only about 0.1 percentage point of recent core PCE inflation.

The opening paragraph quotes Jay Powell:

In a November 2022 speech, Federal Reserve Chair Jerome Powell mentioned that it is helpful to explain elevated inflation levels by examining three underlying categories: goods, housing services, and nonhousing services. He paid particular attention to the last category, stating that it “may be the most important category for understanding the future evolution of core inflation. Because wages make up the largest cost in delivering these services, the labor market holds the key to understanding inflation in this category” (Powell 2022).

And Shapiro concludes as follows:

For instance, recent evidence shows that wage growth tends to follow inflation, as well as expectations of future inflation (Glick, Leduc, and Pepper 2022). Overall, the results highlight that recent labor-cost growth is likely to be a poor gauge of risks to the inflation outlook.

I suspect that some readers might conclude that Shapiro is contradicting Powell. But I don’t see it that way—I think they are both correct. Wages are not causing inflation. Wages don’t predict changes in the path of core inflation. But there is a sense that wages are the essence of the current inflation problem (as Powell is implicitly suggesting.)

Here’s how I look at inflation. An optimal monetary policy (say 3.5% NGDP growth) would lead to steady nominal wage growth at about 3%/year. Because of productivity growth of roughly 1%, that will deliver 2% inflation, on average. Actual inflation will fluctuate due to supply shocks. But any periods of above 2% inflation will be “transitory”, as long as monetary policy keeps nominal wages growing at 3%. And not just transitory; the excess inflation will also be appropriate—that is, better than the alternative of forcing down some prices to offset spikes in other prices.

The fact that nominal wage growth has risen to roughly 5% is an indication that monetary policy has been too expansionary. The resulting inflation is not transitory, and won’t go away on its own. It will take a monetary policy that is tight enough to at least somewhat depress the labor market. (Hopefully not extreme enough to cause a significant recession.) We need to get wage growth down to 3%.

When monetary policy is too expansionary, the effects show up first in flexible prices and nominal GDP. Nominal wages respond with a lag. Thus in any statistical test it won’t look like wages are causing inflation. But because stable wage growth is a roughly optimal monetary policy, wages are in a sense the essence of the inflation problem, without being the cause.

I’m struggling to think of an analogy with weight gain, but let’s suppose that when eating too much the weight first went to your stomach, and then later to your thighs. Also suppose that it’s easier to get the weight back down when it’s still in your stomach, but harder once it adds to your thighs. Excessive wage growth is sort of like the fat thighs; once wages begin growing too fast it’s harder to reduce inflation without a recession.

The question of causation in macroeconomics is trickier than many people suspect. Economists that I respect will say, “It’s silly to say inflation is caused by soaring oil prices, as rising prices are the definition of inflation. That’s like saying inflation is caused by inflation.” Yes, but it’s also true that under certain appropriate monetary policy regimes, certain types of supply shocks can create temporary inflation. All these recent theories of bottlenecks, greed, and wages causing inflation aren’t wrong because they can’t be right, they are wrong because they don’t happen to be right in this case—it’s almost all excess NGDP growth (since 2019).

As a country we ate too much, gorging on monetary stimulus. And now we need to sacrifice with an unpleasant period of dieting.

")

{kind=link}