Darren415/iStock through Getty Photographs

By Blu Putnam

At A Look

- The labor market continues to develop regardless of two quarters of damaging actual GDP

- Gradual labor pressure development plus low labor pressure participation charges are each working to maintain the job market tight

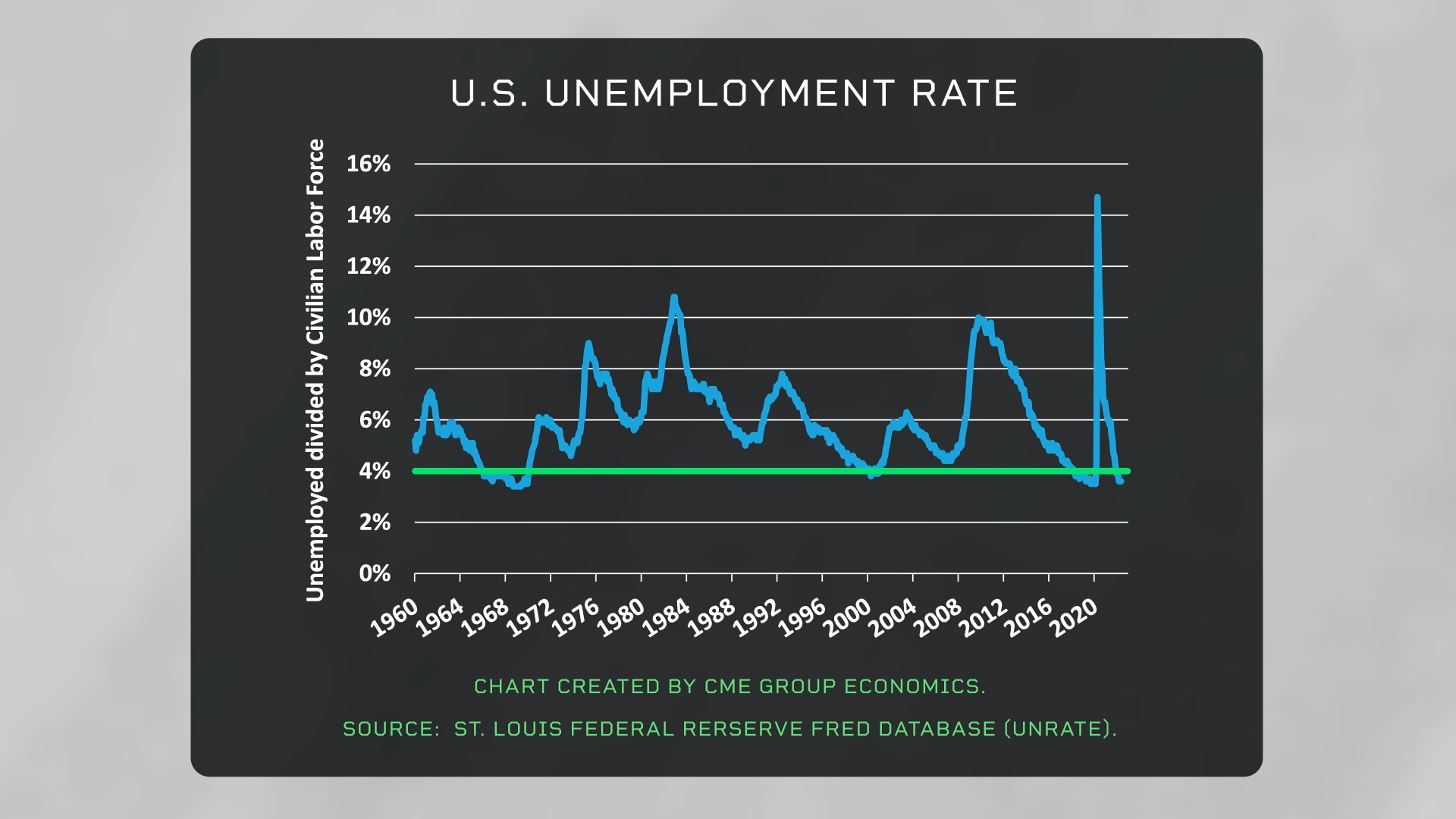

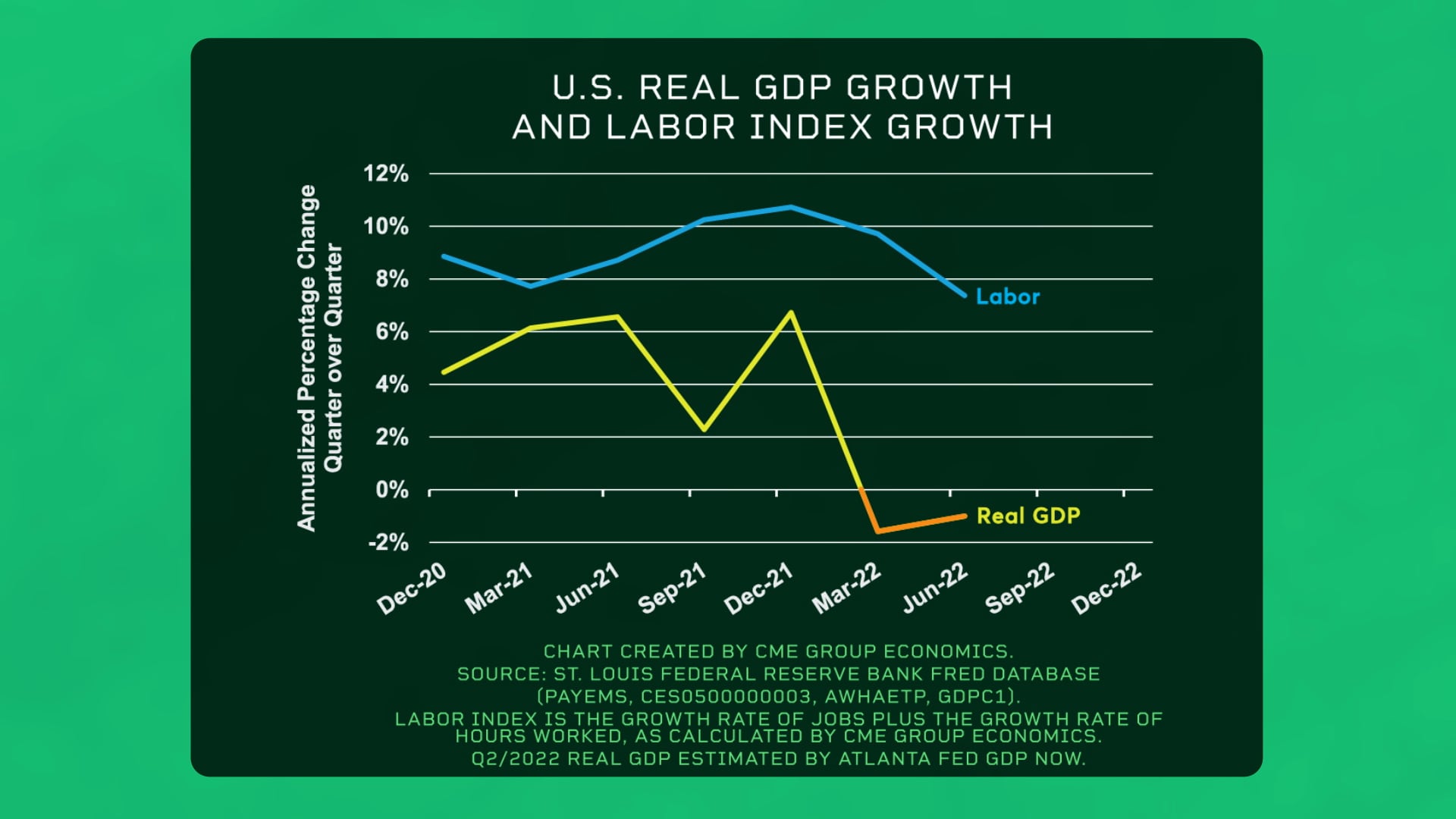

There’s a disconnect between U.S. actual GDP and the labor market. The U.S. job market stays fairly wholesome, with the unemployment charge below 4%, and job development, whereas slowing, stays above the seemingly long-run development. In contrast, U.S. actual GDP was damaging for Q1 2022, and in line with the Atlanta Fed’s GDPNow estimate could also be damaging in Q2 as nicely.

There are 4 key elements to observe on this disconnect.

- Some might select to name two back-to-back quarters of actual GDP declines a recession. However the Nationwide Bureau of Financial Analysis’s recession relationship committee will most likely disagree since they focus extra on actual private earnings and nonfarm payroll employment, the latter of which stays very sturdy.

Writer

2. The Fed’s jobs mandate is particularly to encourage full employment. So, the roles information takes precedence over GDP information within the calculus of how briskly rates of interest is perhaps raised to fight elevated inflation.

Writer

3. Actual GDP recovered its pre-pandemic peak again in Q2 2021, so it was naturally going to decelerate after such a fast rebound. For jobs, the pre-pandemic peak is simply now being absolutely recovered, with job vacancies abound and wages rising.

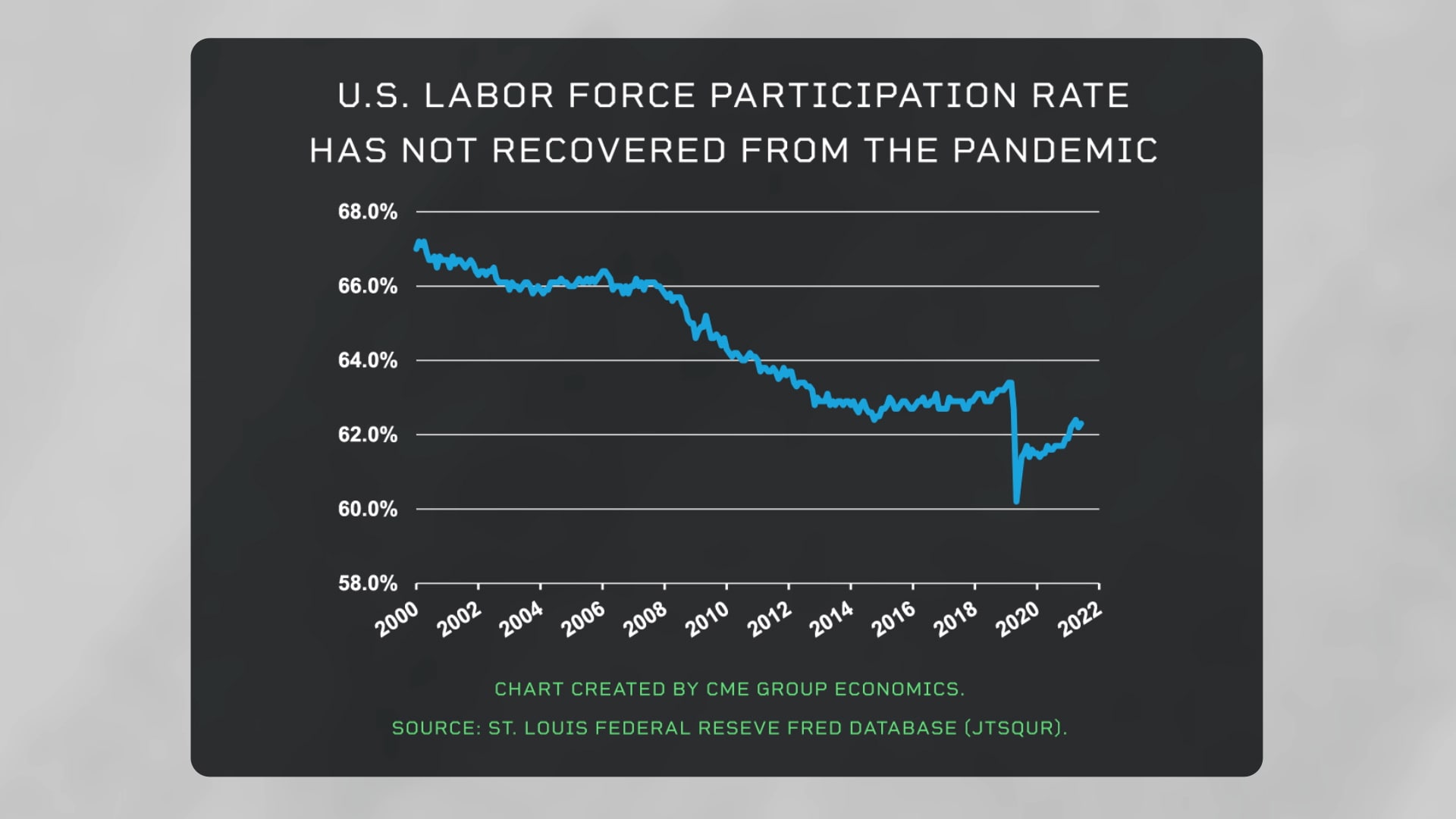

4. Labor pressure development is prone to be very sluggish, and labor pressure participation charges are low, each working to maintain the job market tight.

Writer

The underside line is {that a} sturdy labor market is just not essentially going away simply due to just a little GDP weak spot after a really fast rebound.

Authentic Publish

Editor’s Be aware: The abstract bullets for this text had been chosen by Searching for Alpha editors.

")

{kind=link}