Many traders like to make use of price-to-earnings ratios as a short-hand valuation device for each particular person equities and the broad inventory market. More often than not this may be helpful however there are additionally occasions when it may be very deceptive. Sometimes, these occasions are on the prime or the underside of the earnings cycle.

When earnings are unduly depressed attributable to recession or are over-inflated attributable to reverse financial circumstances, the denominator within the ratio is not consultant of sustainable earnings potential. Because of this the metric itself seems dramatically elevated on the backside of the cycle or considerably depressed on the prime of the cycle, sending a false sign relating to worth.

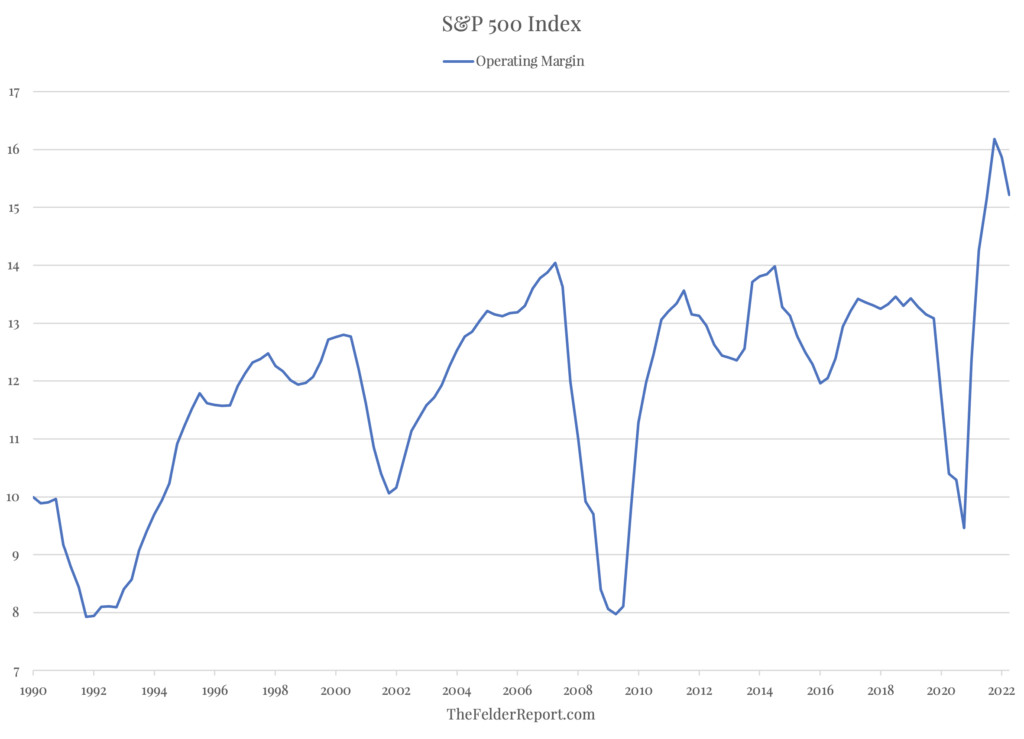

In the present day, the S&P 500 Index sports activities a price-to-earnings ratio of 21 on trailing 12-months’ working earnings and 18 on analyst estimates of working earnings over the following 12 months. Relative to the previous 5 years, these ranges are about common, main many traders to the conclusion that shares, after their decline thus far this yr, are actually pretty valued.

Nevertheless, it’s essential to notice that the revenue margins underlying these earnings at the moment sit at their highest ranges in a long time (if not in historical past). These price-to-earnings ratios then are solely useful to the extent that extraordinarily elevated revenue margins are sustainable. As a result of if revenue margins fall, it can shortly change into obvious that earnings have been over-inflated and thus price-to-earnings ratios have been misleadingly low.

As my good friend, John Hussman, points out (and small companies have been suggesting for months now) there’s a compelling case to be made that that is exactly the case. Labor prices have been surging. Sometimes this places a substantial amount of stress on revenue margins however it has not exerted its regular impact as of but because of large pandemic subsidies. Going ahead, although, it’s probably this relationship reasserts itself and revenue margins normalize, a threat as we speak’s price-to-earnings ratios don’t replicate.

{kind=link}