yuriz

I made a decision to throw my hat within the ring for In search of Alpha’s newest competitors: Prime Inventory With A Catalyst. It has been some time since I printed an article and I figured this could be a enjoyable method to make a comeback. Let’s get straight to the purpose.

My submission for the competition is Spectrum Manufacturers Holdings Inc (NYSE:SPB). Spectrum Manufacturers Holdings is a number one international branded shopper merchandise and residential necessities firm. In different phrases, they promote stuff you want or use at house. Their slogan is “We Make Dwelling Higher at House”. They promote every little thing from kitchen taps to indoor grills and curling irons.

The title Spectrum Manufacturers in all probability does not imply a lot to you (former Rayovac) however you in all probability used a few of their merchandise. You’re almost definitely accustomed to a few of their manufacturers reminiscent of: Kwikset, Baldwin, Pfister, Weiser, Black Flag, Sizzling Shot, Spectracide, Remington, George Foreman (the grill), Black + Decker, PowerXL… and there are various extra. I simply listed a few of the ones I acknowledged.

SPB operates as a holding firm and is principally 4 companies:

International Pet Care (GPC)

House & Backyard (H&G)

House & Private Care (HPC) – now referred to as “Empower Manufacturers”

{Hardware} & House Enchancment (HHI)

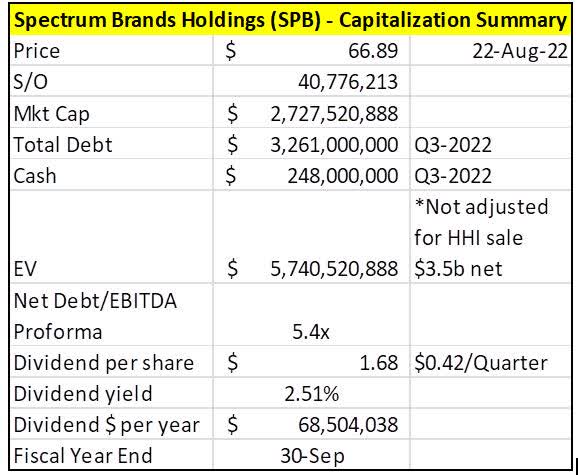

This is a snapshot of SPB’s capitalization abstract:

Creator’s Work

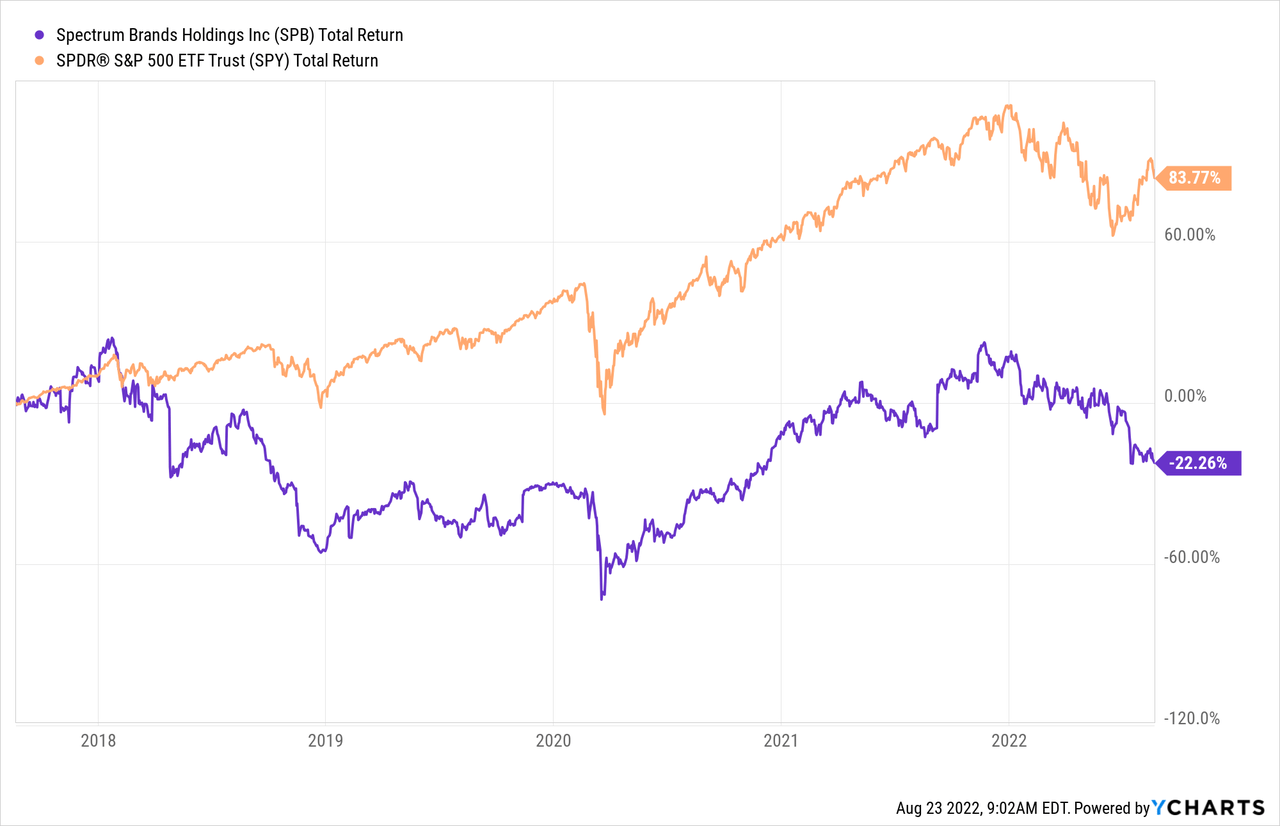

SPB’s inventory has been a laggard. If you’re a long-term shareholder, you were not properly rewarded. This yr SPB has offered off together with different housing-related names, on fears that interest-rate hikes will sink its enterprise. SPB is down -33.95% YTD, -37% from its peak of $107.22, and -28% for the reason that HHI sale was introduced.

The 5-year chart signifies that SPB hasn’t achieved a lot and lags the S&P 500. I would not attempt to kind a conclusion by previous efficiency. Spectrum is placing behind them a legacy of issues. The long run seems to be brighter.

For traders, it is time to cease excited about what Spectrum was and as an alternative look forward to what it is going to be. Let me lay out the thesis.

Thesis/Catalysts

Spectrum has two “laborious” catalysts that I can determine that the market hasn’t already absolutely anticipated or understood.

Spectrum is at the moment promoting their {Hardware} & House Enchancment (HHI) enterprise to ASSA ABLOY (OTCPK:ASAZY) for $4.3 billion in money ($3.5b internet).

Spectrum is exploring the thought of separating their House & Private Care (HPC) enterprise. That could possibly be by a possible spin-off or different transaction. For the time being they’ve “carved-out” the enterprise.

Due to these two developments, I consider that the shares of SPB will probably be pushed increased for the next causes:

SPB is within the course of of making a pure play International Pet Care (GPC) and House & Backyard Firm (H&G). These two companies are the gem of SPB. As soon as the catalysts are accomplished the narrative round SPB will change from an “overstretched levered difficult shopper product conglomerate firm” to a pure play GPC and H&G firm.

A extra centered, leaner, and less complicated enterprise ought to warrant a better valuation from the market. The maths behind the Sum-of-The-Components is compelling. Together with a 20% margin of security, I consider there is a minimal upside of 21.6%. There is a detailed valuation beneath.

The catalysts ought to unlock vital shareholder worth. SPB is getting an incredible value for his or her HHI section. ASSA ABLOY is paying 14x FY21 Adjusted EBITDA for $4.3 billion. SPB expects to obtain roughly $3.5 billion in internet proceeds. That is greater than the present market cap of $2.7b. SPB purchased the division for $1.4b in 2012. This is sensible from a worth creation perspective.

As soon as the transaction closes, SPB’s stability sheet will probably be reworked. SPB will go from a Internet Debt place to Gross Money. SPD targets a gross leverage ratio of ~2.5x Internet Debt/Adjusted EBITDA. Presently proforma internet leverage was at 5.4x for Q3-2022.

SPB expects to have a money stability of roughly $2b as soon as present indebtedness is paid off.

Extra proceeds will probably be used to speculate for natural development, fund complementary acquisitions, and return capital to shareholders. In different phrases, extra environment friendly capital allocation.

The International Pet Care enterprise is their “crown jewel” asset. It is the section that may drive the corporate ahead and it isn’t being correctly valued by the market. The same comp, Central Backyard & Pet Firm (CENT), is buying and selling upward of 10.5x EV/EBITDA.

The enterprise rationale for conserving International Pet Care and House & Backyard is that capital will be extra effectively allotted. These companies have a unique development trajectory and danger profile. HHI grows with the housing market. Promoting the HHI section will make them much less correlated with the housing market. HPC is linked to the buyer financial system. GPC is benefiting from the present pet growth. H&G confirmed that it is recession resilient.

Every enterprise may also have their very own shareholder base. Individually they’re good companies, however as a result of the financials are advanced, the various transferring elements, and traders spending an inordinate period of time evaluating it, traders aren’t seeing the complete potential. SPB 2.0 will probably be less complicated.

And if you happen to might, there are some “softer” catalysts to think about. SPB accomplished their “International Productiveness Enchancment Program”. It is principally a flowery time period for a value saving program and a revamped enterprise mannequin. The plan geared toward enhancing the corporate’s working effectivity and effectiveness. The unique objective was to realize $150m in financial savings, by the top of FY2022 (September 30). That was raised $200m and is essentially accomplished. The financial savings are more likely to be reinvested into development initiatives and shopper insights, R&D, and advertising throughout every enterprise. Additionally final quarter, Spectrum eradicated 17% of its international salaried positions through the quarter, and that may drive over $30 million of annualized financial savings. However let’s work with $200m in financial savings. A 10x a number of would suggest $2b in further worth. A 15x a number of would imply $1.5b. Nonetheless I do not assume we’re seeing the complete profit. The implementation of the Program is current and SPB has been hit by provide chain points and inflation. As soon as the catalysts are accomplished, we should always have entry to “cleaner” and less complicated monetary statements.

Dangers & Uncertainties

This isn’t an ideal story. There are hiccups. Listed here are a few of the explanation why the market is just not absolutely appreciating the story. The Spectrum Manufacturers story has been bumpy and messy.

The transaction with ASSA ABLOY is taking longer than anticipated. Introduced in September 2021, the transaction was initially anticipated to shut in 2022. Nonetheless, the US regulator continues to evaluate the proposed acquisition. Each firms agreed to increase their settlement to June 30, 2023. The 4.3 billion greenback query is “Will it take that lengthy?” Each firms have reiterated that they’re assured that the transaction will shut.

There is a danger that the transaction falls by. That would not be the top of the world as a result of there’s different potential consumers for that division (they carried out an public sale). In case this occurs, it will push the thesis out and SPB would doubtless get a cheaper price.

SPB is promoting their largest enterprise. HHI accounts for the biggest portion of gross sales and earnings (~43% EBITDA Q3-21). Buyers have questions. Why? And what’s going to this new enterprise appear like when it comes to development and FCF era. However it is sensible from a pure value-creation perspective. SPB purchased the division for $1.4b in 2012. You’re getting 14x EBITDA and pivoting the stability sheet from a internet debt to gross money.

The ghosts from the previous are nonetheless there. SPB filed for chapter in 2009 and excessive debt was the problem. Since then, the debt has fluctuated loads. As we speak’s debt is manageable. The debt is roofed by working earnings (~1.5x to ~3x relying on the quarter) and internet debt has been trending down over the previous couple of years. This attitude downside ought to reverse as soon as the stability sheet is gross money.

Buyers are excited about the outdated Spectrum. As an alternative they need to look forward to what it is going to be. However I do not blame them for the explanations talked about above.

- Who is aware of the place shopper demand will probably be in 6 months? Like most shopper product firms and retailers, they’re going through shopper demand unpredictability and softer demand. Simply ask Walmart (WMT) and Goal (TGT). It is fairly a headache.

Spectrum is not any stranger to transactions. They purchase and divest on a regular basis. It may be laborious to comply with. Typically a transaction is strategic, generally it is to scale back leverage. Typically they promote “non-core” property, generally they purchase to pad a portfolio (just like the Tristar acquisition). All this provides a layer of complexity to the story.

SPB is a really seasonal enterprise. SPB generates nearly all its money within the fiscal third and fourth quarters (which ends on September 30).

Brief-term worries dominate the inventory efficiency. The market likes visibility and certitude. Cash flows in the wrong way. Cash likes an excellent story. Cash likes development. And proper now with SPB it is difficult. Right here we’ve incertitude on three fronts: 1) if and when the deal will shut 2) the difficult shopper habits and deteriorating macro backdrop 3) what’s going to the post-transaction enterprise appear like whenever you take away 43% of EBITDA and 35% of revenues and have carved out HPC. So it is cloudy and the market hates it.

An absence of “visibility” mixed with recurrent “non-recurrent” points has plagued SPB for years. You need to be a monetary assertion ninja to make sense of their reporting. “One-time” points reminiscent of recognition of loss on asset sale, write-off of impairment of intangible property and goodwill, non-cash bills right here and there are too widespread.

It was obvious that SPB suffered from underlying structural points that took years to resolve and plenty of cash. Which led to the “International Productiveness Enchancment Program”. SPB is just not out of the woods but, however there’s mild on the finish of the tunnel.

While you add all of this up, I perceive why the market is down on SPB.

However if you’re affected person this works in your favor. As a result of as soon as we transfer previous all of that, you might be left with a a lot better enterprise. Additionally all this cloudiness gives a chance to purchase SPB at a second when the market is just not pricing within the catalysts.

International Pet Care (GPC) – House & Backyard (H&G)

This is a quick overview of what the longer term firm will appear like.

After the 2 transactions are accomplished, Spectrum may have two companies, 1) International Pet Care and a pair of) House & Backyard. These are Spectrum’s two greatest companies. Virtually talking, which means it is rising, it has excessive margins, high-velocity consumable companies which have traditionally been recession-resilient.

GPC ought to proceed to profit from the present pet growth. The demographics of pet possession have trended in the direction of millennials and Gen Z, and so they spend loads on their pets. In accordance with a 2021 survey from the American Pet Merchandise Affiliation (APPA), the proportion of U.S. households that had pets elevated in 2020 from 67% to an all-time excessive of 70%. The survey additionally says that they’re spending 11% extra on pet meals.

For Q3-2022, GPC delivered a document fifteenth consecutive quarter of income development. The enterprise delivered one other robust income quarter with reported and natural internet gross sales development of 12.8% and 17.3%. The pet enterprise is a traditionally recession-resistant enterprise with large upside potential. The present EBITDA run-rate for GPC is $200m/yr.

As for the H&G enterprise, unfavorable climate situations throughout america took a success on Q3-2022 outcomes. H&G could be recession resilient, nevertheless it’s not climate resilient. Regardless of drought situations in massive elements of the US, they did alright. Unhealthy climate impacts shopper demand and retailer replenishment (much less visits to the shop). H&G is a diversified section. You’ve a group of cleansing merchandise, pest management merchandise which incorporates repellant, herbicides and pesticides, and you’ve got soil and plant stuff. However pest management is a key driver and it is secure to say that folks hating bugs is just not going away. Cleansing and pest management are attention-grabbing classes as a result of they’re extra related to repeat high-velocity purchases versus classes reminiscent of mild bulbs. This section has been recession-resistant previously as outside dwelling and gardening each usually do properly in robust financial instances (it grew within the final recession). One of many excellent news is that H&G is profitable lots of distribution for subsequent yr. Administration believes that H&G can generate greater than $120 million of EBITDA per yr.

Regardless of the near-term headwinds, these companies stay competitively positioned. Unencumbered by the previous, the brand new Spectrum has the potential to compete extra fiercely than the outdated cumbersome firm it was. What’s extra, a greater stability sheet and extra environment friendly capital allocation choices ought to earn the brand new Spectrum a better inventory market valuation.

Dividends & Share Buybacks

SPB pays a dividend of $0.42 per quarter which equals to $1.68 on an annual foundation. This can be a $68m annual dedication. It has been the identical payout since 2018. SPB has been an everyday purchaser of their very own shares too. As a result of earnings and FCF are in every single place quarter to quarter, it is laborious to make sense of the payout ratio. Would not it have made extra sense to pay down some debt as an alternative of buybacks? SPB spent $121m on buybacks in 2021, $268m in 2020, and $134m for the primary three quarters of FY2022.

As for the dividend, administration’s language suggests they’re non-committal (“topic to evaluate infrequently”). My interpretation is they’d discover the thought of “resetting” the dividend as soon as the HHI is offered and HPC is carved out.

Spectrum appears carnivorous in its personal nature. My take is to look how a lot inventory they purchased with a levered enterprise. Think about as soon as they’re in a gross money place.

CEO David Maura did add this gem through the Q3-21 incomes name:

Hypothetically, to reply your query, I imply, if we got here right into a bunch of money at this time, if it simply fell out of a helicopter, I might purchase again lots of inventory. I do know everybody is aware of this, and I do know that I nonetheless look incorrect within the brief time period, however I feel our safety — I feel our inventory value is materially undervalued.

Valuation

Let’s add all of it up. The straightforward strategy can be to use a a number of to a normalized adjusted EBITDA and name it a day. Not solely am I weary of firms with advanced financials utilizing adjusted EBITDA, that strategy would not provide you with a correct valuation evaluation of Spectrum. SPB is 4 companies with totally different money circulate profiles, danger, and margins. On the highest of that it’s a must to consider the 2 catalysts that may change the narrative and profile of the enterprise.

My most well-liked valuation technique is counting the free money circulate. However over the past couple years, there have been many mis-steps and the script for SPB has modified from dependable FCF era to a extra cyclical firm in “transition”. Given the cyclicality of the portfolio doubtless leading to unsteady money flows over time, I take advantage of a EV/EBITDA strategy for the totally different elements of the enterprise to derive worth.

As for the EBITDA, if you happen to have a look at Q2 and Q3 outcomes, it is just a little little bit of a multitude. I would not attempt to learn an excessive amount of into these numbers and kind a conclusion. For Q3-2022 gross sales elevated 10% (4.4% natural). However SPB has been hit by inflationary stress. Among the improve in value is short-term, reminiscent of increased transportation and distribution value, in addition to further storage value. SPB has responded by eliminating 17% of their international salaried positions and that may drive over $30m of annualized financial savings. On the highest of that SPB has been trimming down stock stage and ran operations to maximise money circulate as an alternative of reported earnings. This negatively impacted margins and contributed to the shortfall to their unique earnings outlook. SPB additionally will increase costs to satisfy their focused inflation protection that may begin to present in This fall. Administration mentioned that issues have stabilized in July, the primary month of This fall. I do know it is only one month, however with costs going up and prices stabilizing, we should always count on expanded EBITDA margins going ahead.

In different phrases, for SPD to raised place themselves for FY2023 and long run success, they determined to maximise money circulate era on the expense of near-term EBITDA. As CEO David Maura put it on the current analyst name:

“And so there isn’t any query that we’ve in all probability taken actions which are extra Draconian than our opponents. However my view of the world is, I need to take my drugs quick as a result of I need to get wholesome quicker.”

SPB took some aggressive steps as a result of they need to enter the brand new fiscal yr as lean from an expense and stock place as doable. SPB’s fiscal yr ends on September 30. That is only a couple weeks away. Then it is the vacation season. SPB doubtless needs to enter the vacation season in an excellent place.

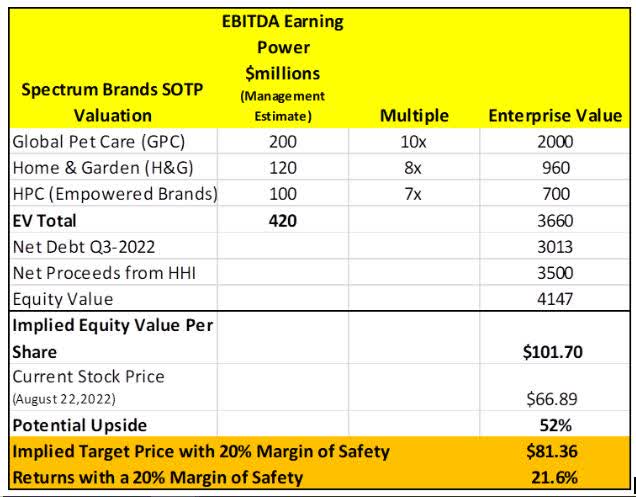

Again to EBITDA. Due to the various changes required, the totally different transferring elements, and the issue pinning down the precise mixture of enterprise unit contribution, I’ve as an alternative relied on what administration calls EBITDA incomes energy. Administration firmly believes SPB has over $400m of EBITDA incomes energy (excluding HHI).

Administration believes GPC has the flexibility to generate better than $200m of EBITDA per yr, H&G can generate better than $120m of EBITDA per yr, and HPC (now referred to as Empowered Manufacturers) has the flexibility to generate at the very least $100m per yr. These numbers do not come out of skinny air. GPC already has a $200m/yr EBITDA run price.

This is a Sum-Of-The-Components (SOTP) strategy:

Creator’s Work

Underneath this strategy, Spectrum is price between $81.36 a share to $101.70, which suggests a return between 21.6% and 52%. The vary hole is because of a 20% of margin security I utilized. The margin of security is very subjective from investor to investor, and from firms to firms. I used 20% to be conservative, to keep in mind potential errors of judgment, the uncertainty surrounding Spectrum, and the messy macro backdrop (inflation, financial slowdown, rising charges, lack of shopper predictability, and Spectrum doing Spectrum issues). I additionally consider that utilizing a 10x a number of of Globe Pet Care enterprise is conservative contemplating the expansion profile and high quality of the enterprise. A takeover would warrant a better a number of.

I additionally used this strategy for simplicity’s sake. I may develop bull-base-bear situations and run an 800 line spreadsheet, however I’ve sufficient expertise that on the finish of the day only some key variables drive values.

The lazy again of the serviette strategy is making use of a a number of of 7x to an estimated adjusted EBITDA of $420m. That will suggest a share value of $84 per share or a 25% upside.

As for the comparable:

Creator’s Work

The ratios recommend that Spectrum is buying and selling beneath its comps. SPB trades at 0.9x Worth/Gross sales, beneath the comps common of 1.5x. And the typical EV/EBITDA ratio of 13x is approach increased than what I used for my valuation (7x-10x).

Spectrum is a kind of firms the place you’ll be able to slice and cube the numbers for a very very long time. On the finish of the day, a conservative strategy with a margin of security means that Spectrum is undervalued by at the very least 21.6%. The mix of administration executing properly and catalysts unlocking worth may reward shareholders much more. As soon as SPB 2.0 is established, traders ought to count on higher visibility on FCF, extra buybacks, and the market correctly valuing the remaining enterprise.

Abstract

Time is your pal right here. Attending to that increased valuation will imply persevering by some tough instances. Spectrum is coping with a few of the identical supply-chain and inflation-related points which have damage different firms. These pressures are beginning to wane, and SPB has been capable of cross alongside value will increase to shoppers. We must always begin seeing value hikes hitting the underside line within the subsequent couple quarters.

Even if you happen to clearly determine worth, fairly often the market does not absolutely embrace it except there’s an occasion or an motion to unlock, which is also known as a catalyst.

This text has recognized that Spectrum has two laborious catalysts that may unlock vital shareholder worth. I additionally defined why the market hasn’t already absolutely anticipated or understood the scenario.

Spectrum is the place it’s at this time due to choices made previously. As we speak Spectrum is making choices which are transformational. There’s Spectrum at this time and the place it is going to be. In between these two factors is time. You need to await the catalysts to be accomplished and for the market to reassess.

If you’d like totally different funding outcomes from the gang, it’s a must to be investing in issues that others have not flocked to, inflicting it to be absolutely valued. SPB is a kind of alternatives that I wish to say fell off the orbit. It is off the orbit as a result of no person is paying consideration. No person cares. A fast look is sufficient to flip you off. Therefore the chance. The market will come again as soon as every little thing is squeaky clear. By then it is going to be too late. What the market is just not absolutely appreciating is the makeover story. Fundamentals win. And the basics are getting higher.

The outdated SPB gives an eclectic and diversified portfolio of mishmash merchandise. After years of working by challenges partly because of inadequate capital allocation to innovation and advertising, operational missteps, and a extremely levered stability sheet, Spectrum Manufacturers is refocusing to grow to be a pure play International Pet Care and House & Backyard enterprise. As soon as that occurs, the markets will re-rate the valuation of the corporate.

I am satisfied over time that the dimensions of the low cost between how the market values SPB at this time and the SOTP will slender as soon as the image is clearer.

The long run new SPB will probably be extra centered, leaner, and less complicated with improved fundamentals and a stronger basis. As we glance forward, Spectrum’s future seems to be brighter.

")

{kind=link}