DNY59/iStock via Getty Images

Anyone following our research over the last few months knows that SoFi Technologies (NASDAQ:SOFI) doesn’t need a change in the Biden Administrations stance on student debt forgiveness to reward shareholders. The good news for shareholders is that the Supreme Court appears set to block the debt forgiveness plan by June. My investment thesis remains ultra Bullish on the stock after the dip back below $6 following contagion fears due to the SVB Financial Group (SIVB) collapse.

Source: Finviz

Supreme Court Case

Last week, the Supreme Court heard the oral arguments on why the Biden Administration student debt loan forgiveness plan was illegal. The plan involves forgiving student debt of up to $20,000 per borrower when meeting certain income requirements.

The initial comments by the Supreme Court suggest several questions on the authority of President Biden to forgive $400 billion worth of debt without the approval of Congress. The President doesn’t have the authority to just randomly dismiss large amounts of debt.

Either way, SoFi is more concerned about resolution of the student debt moratorium issue than whether the Supreme Court blocks the forgiveness plan. The moratorium on student debt repayment and this lawsuit has delayed potential high income members of the fintech from refinancing student debt with SoFi.

The company works with borrowers excluded by the loan forgiveness plan due to high incomes, but the legal case has caused an extension of the moratorium. SoFi wants the lawsuit to end whether blocked by the Supreme Court or not and the bank subsidiary just sued the Biden Admin. in order to remove the moratorium on student loan payments, especially for those not even a part of the cancellation plan.

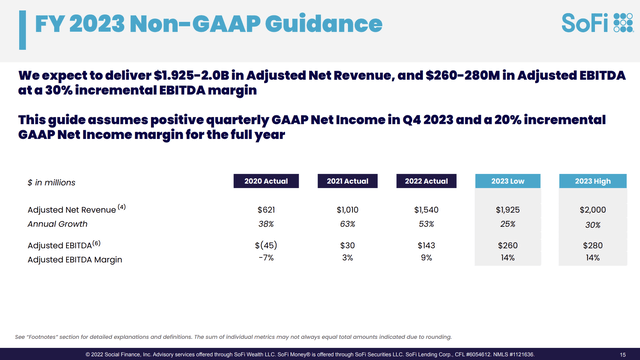

The fintech provided the following strong guidance for 2023 on January 30 when reporting Q4’22 earnings.

Source: SoFi Q4’22 presentation

Most importantly, the guidance included the following macro assumptions:

- Interest rates: assuming an outlook consistent with the consensus forward curve, with a peak Fed funds rate reaching approximately 5% in Q2 2023, with two rate cuts in the back half of the year to get us to a 4.5% exit rate in 2023.

- Economy: a 2.5% contraction in GDP and a normalization of unemployment to around 5%.

- Credit: continuation of elevated credit spreads across capital markets and a continued normalization of consumer credit.

In essence, SoFi guided to impressive revenue growth of up to 30% with an adjusted EBITDA margin of 14%. As outlined in the previous research, these adjusted EBITDA numbers approximate adjusted profits.

These growth numbers assume a sizable recession with a huge spike in unemployment this year. The fintech has possibly assumed the worst possible outcome while not forecasting any tailwinds from the Supreme Court blocking the Biden Admin’s loan forgiveness plan, or at least ending the pause on payments.

Booming Business

SoFi entered covid lockdowns with a booming business reliant on student debt refinancing. The fintech acquires new members with $170K+ in income and help these Doctors, Lawyers, MBAs or software engineers to refinance student debt and eventually build a financial product suite with the fintech.

The company grew revenues over 58% in Q4’22 while the student debt issue continues to constrain growth. Investors appear to be holding back the stock due to the student debt moratorium, yet SoFi continues to report explosive growth.

The digital charter has allowed SoFi to collect a large amount of member deposits to fund loan growth. The fintech ended 2022 with a deposit base of $7.3 billion. The bank now offers a 3.75% interest rate to depositors, which still provides the bank with a 190 basis point benefit from other sources of capital like warehouse loans.

Source: SoFi website

A big key to the current deposits is that SoFi offers already competitive interest rates and isn’t at risk to clients moving relationships to another bank. Also, the fintech is focused generally on student debt refinancing limiting the amount of large depositors anywhere close to the FDIC insurance levels of up $250,000 per member.

Source: SoFi website

The CFO participated at the KBW Fintech Payments Conference back on March 3. Chris Lapointe didn’t provide any indication of business impacts from the SVB bank blowup, but most of the issues occurred in the last week following the conference appearance.

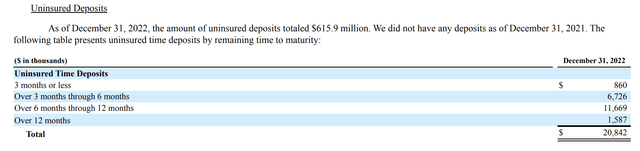

At the end of 2022, SoFi listed less than 10% of the deposit base as uninsured. In theory, the bank would only have up to $616 million in deposits at risk of being withdrawn under any bank run fear similar to what occurred at SVB.

Source: SoFi 10-K

The good news is that CEO Anthony Noto spent nearly $1 million buying more SoFi shares at $5.53 in a huge sign of confidence in the business. The CEO bought over $4 million worth of shares back in December when the stock fell into the $4s.

Takeaway

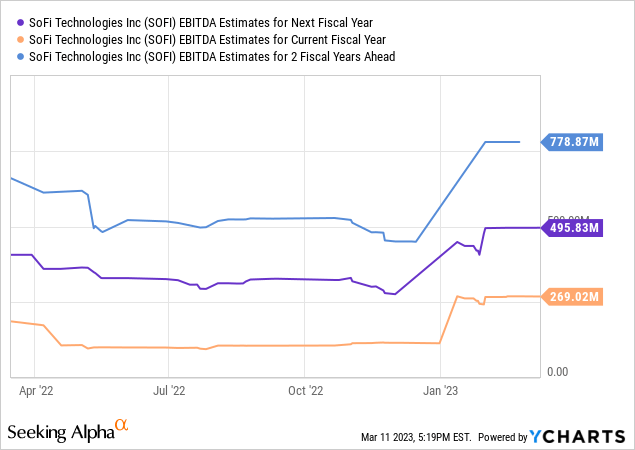

The key investor takeaway is that SoFi is falling due to irrational fears from the bank contagion fears when the market should be focused on the likely possible positive outcomes from the Supreme Court ruling on student debt. SOFI stock only trades at ~10x 2024 adjusted EBITDA targets of $496 million offering an extreme bargain to new shareholders.

")

{kind=link}