jetcityimage/iStock Editorial by way of Getty Photographs

If all people listed, the one phrase you would use is chaos, disaster… the markets would fail.

– John Bogle, Might 2017

Attempt to purchase belongings at a reduction fairly than earnings. Earnings can change dramatically in a short while. Often, belongings change slowly. One has to know way more about an organization if one buys earnings.

– Walter Schloss

Introduction

Vitality equities have outperformed considerably year-to-date in 2022, with the Vitality Choose Sector SPDR Fund (XLE) up 45.3% in 2022. This compares very favorably to a 7.5% YTD decline within the SPDR S&P 500 ETF (SPY), a 14.8% decline within the Invesco QQQ Belief (QQQ), a 18.2% decline within the iShares 20+Yr Treasury ETF (TLT), and a 37.6% decline within the ARK Innovation ETF (ARKK).

XLE SPY QQQ TLT ARKK (Creator, StockCharts)

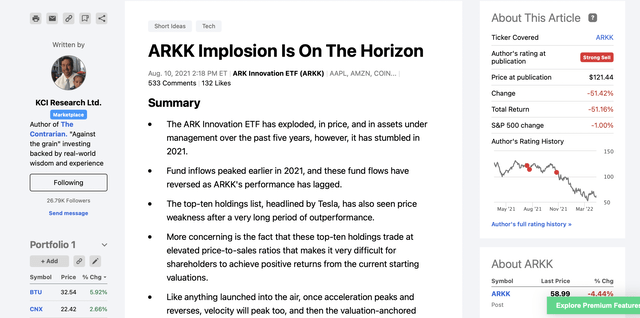

Progress shares, led by the momentum progress favorites that dominate ARKK, have been severely impaired, held again by their poor beginning valuations, one thing I wrote about intimately on August tenth, 2021, with the article titled, “ARKK Implosion Is On The Horizon.” Since that article was revealed, ARKK shares are down 51.2%, vs. a 1% decline within the S&P 500 Index (SP500), as illustrated within the picture beneath.

Creator’s August tenth, 2021 Article Snapshot (Creator, Searching for Alpha)

Clearly, progress shares are struggling, as rising rates of interest the yield curve, however notably on the longer finish of the yield curve, scale back the enchantment of the longest period belongings.

On the other aspect of the ledger, excessive free money stream yielding firms are being rewarded, and lots of of those free money stream standouts reside within the commodity fairness sector. Taken collectively, a historic capital rotation is underway. That is one thing I’ve chronicled regularly, documenting the stream of cash from the “Have’s” to the “Have Not’s.” These public articles beneath reference this historic capital rotation.

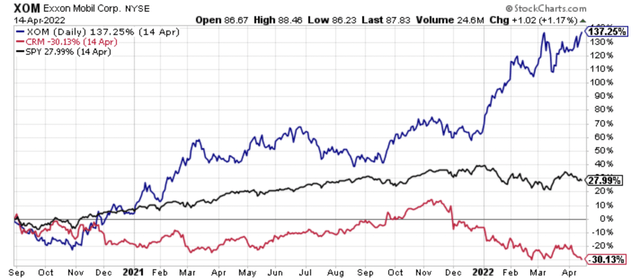

Including to the narrative, with this public article, I outlined how eradicating Exxon Mobil (XOM) from the Dow Jones Industrial Common (DIA) and changing the venerable, longest listed Dow Jones part with Salesforce.com (CRM) in August of 2020 would grow to be a excessive water marker for the present state of the monetary markets. The share value efficiency of Exxon and Salesforce.com shares since that elimination date says every thing that you have to know in regards to the monetary markets since August 2020.

XOM Versus CRM Efficiency Since XOM Was Changed By CRM In The DJIA (Creator, StockCharts)

Trying on the chart above, Exxon Mobil shares have strongly outperformed Salesforce.com shares since Exxon was faraway from the DJIA and Salesforce.com shares have been added. Let’s not overlook that the lively choice makers at S&P International (SPGI) eliminated Exxon and added Salesforce.com as a result of they thought that Salesforce.com was extra consultant of the way forward for the market. This occurred though the financial affect of Exxon Mobil was far better on the time of the swap, and that hole has elevated at the moment as Exxon’s revenues, internet revenue, and free money flows have surged with increased power costs.

With the good thing about hindsight, nearly all market contributors have been crowded on one aspect of the boat, overweighting know-how shares, and underweighting the left behind worth shares, notably the downtrodden commodity equities.

One of the best instance of this seismic shift within the funding panorama has been within the efficiency of pure gasoline equities, which have trounced their vaunted FAANG friends in efficiency phrases, throughout a variety of time frames relationship to January 1st, 2020, as I’ll illustrate beneath within the physique of this text, which is an up to date fourth version to my February third, 2021 article, “Off To The RACES: Pure Fuel Equities Lapping FAANG Shares, the Might twenty sixth, 2021 follow-up, after which the September tenth, 2021 third version.

As we strategy the month of Might, which is racing season in Indianapolis, the favored pure gasoline equities, which I’ve coined with the time period RACES, which is the primary letter of every of the equities profiled extra in-depth beneath, are one of the best performing, most obscure nook of the market, that almost all traders have ignored, till lately. With the present slingshot increased in costs, many traders at the moment are acknowledging, appreciating, and shopping for into pure gasoline equities and associated equities as funding candidates, recognizing that their free money stream estimates are surging on the again of upper pure gasoline, and pure gasoline liquids costs.

Off To The RACES Shares Are Approach Forward Of FAANG Since The Begin Of 2020 And The Hole Is Widening

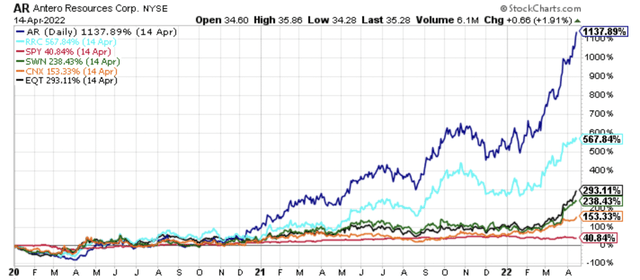

The next efficiency chart reveals the whole return of Vary Assets (RRC), Antero Assets (AR), CNX Assets (CNX), EQT Corp. (EQT), Southwestern Vitality (SWN), and the SPDR S&P 500 ETF (SPY) since January 1st, 2020 via Thursday, April 14th, 2022.

AR RRC EQT SWN CXN SPY Efficiency Since January 1st, 2020 via April 14th, 2022. (Creator, StockCharts)

Antero Assets shares lead the pack, increased by 1137.9% because the begin of 2020. For perspective, within the final article on this sequence revealed on September tenth, 2021, AR shares have been increased by 462.2% from January 1st, 2020 via Thursday, September ninth, 2021. Vary Assets is subsequent in line, with a complete return of 567.9%, adopted by EQT Corp., whose shares have gained 293.1%. Southwestern Vitality shares have gained a cumulative 238.4%, and CNX Assets shares have gained 153.3% because the begin of January 2020.

Notably, all of those pure gasoline equities have considerably outperformed the SPDR S&P 500 Index ETF, which has gained 40.8% over this timeframe, really down from the 43.0% within the final replace on this sequence, once more revealed on September tenth, 2021.

Collectively, the “Off To The RACES” shares have a mean return of 478.1% since January 1st of 2020. That is up considerably from the 190.4% common return from the final replace, and the 152.6% common return since January 1st of 2020 revealed within the Might twenty sixth, 2021 article.

Trying again to the primary article within the sequence, the typical return of 478.1% is up considerably from the typical return of 80.4% from January 1st, 2020 via February 2nd, 2021. This may shock many traders who’ve solid apart power equities to the dustbin of historical past, but these solid apart power equities are considerably outperforming.

What are the returns of the FAANG shares over this timeframe?

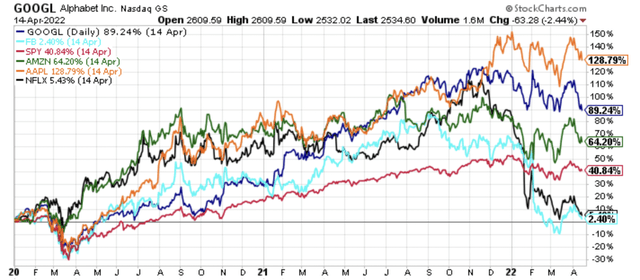

GOOGL FB SPY AMZN AAPL NFLX January 1st 2020 By April 14th, 2022. (Creator, StockCharts)

Like a rotating solid of characters, Apple (AAPL) shares have now jumped into the lead amongst the FAANG quintet, posting a 128.8% acquire from January 1st, 2020 via Thursday, April 14th, 2022. The acquire for Apple is reasonably above the 112.7% acquire in Apple shares posted throughout the September tenth, 2021 replace on this sequence. The issue, nonetheless, is that the remainder of the FAANG shares have struggled mightily over this timeframe.

Alphabet (GOOGL), (GOOG), shares at the moment are up 89.2% from January 1st, 2020, which is a decline from the 114.3% acquire within the final replace. Amazon (AMZN) shares now sport a 64.2% acquire since January 1st, 2020, down from an 88.6% acquire within the final replace. Netflix (NFLX) shares have cratered, solely posting a 5.4% acquire since January 1st, 2020, down from 84.7% acquire within the September tenth, 2021 replace. Equally, Fb (FB) shares have cratered too, solely up 2.4% from January 1st, 2020 via April 14th, 2022, which was down from the 84.2% acquire within the final replace.

The up to date returns for the FAANG shares collectively, are a mean return of 58%, which is a significant decline from the typical return of 96.9% within the September tenth, 2021 replace on this sequence. With this decline, the benefit of the FAANG quintet over the SPDR S&P 500 ETF has shrunk considerably, with SPY up 40.8% from January 1st of 2020.

Offering perspective, the typical 58% acquire for FAANG shares not solely beneath the typical 96.9% acquire in FAANG shares from the September tenth, 2021 replace, it is also beneath the 68.5% return posted by the FAANG shares from the Might twenty sixth, 2021 replace, which lined January 1st, 2020 via September ninth, 2021 Might twenty fifth, 2021. That return was itself up reasonably from the primary article on this sequence, with FAANG shares increased by 62.2% on common since January 1st, 2020 via February 2nd, 2021. So, FAANG shares have successfully declined as a gaggle from their February 2nd, 2021 ranges, which is exceptional when you consider the narrative within the markets at the moment. On this word, as I wish to say, narrative follows value.

Backside line, the “Off To The RACES” shares have delivered an 478.1% common acquire because the begin of 2020, up from the 190.4% return on common from the final replace, considerably forward of the FAANG common inventory return of 58% since January 1st, of 2020. This FAANG 58% common acquire is down from the 96.9% common acquire from the September tenth, 2021 replace. The return hole is widening with every up to date article on this sequence, which isn’t a shock given the beginning valuation positions of every group of equities circa January 1st, 2020.

Vitality Costs Are Surging Led By Pure Fuel Costs

Including to the bullish narrative and relative value efficiency power is the truth that pure gasoline liquids costs and dry pure gasoline costs are each surging, led by an explosion increased in dry gasoline costs year-to-date in 2022.

Dry pure gasoline costs, which could be monitored with america Pure Fuel Fund (UNG), and america 12-Month Pure Fuel Fund (UNL), have lately damaged via the $7 stage (for perspective, that they had damaged the $5 stage within the final replace on this sequence).

Dry Pure Fuel Costs (Creator, StockCharts)

The breakout in dry gasoline costs has seen each UNG and UNL make new multi-year highs.

UNG Each day (Creator, StockCharts)

UNL Each day (Creator, StockCharts)

For perspective, within the September tenth, 2021 replace on this sequence, UNG was priced at $17.49, and at the moment it’s at $25.60. In the meantime, UNL was priced at $13.13 within the September tenth, 2021 replace (these are September ninth costs), and it’s at $23.21 as of the market’s shut on Thursday, April 14th, 2022.

Given the favorable provide/demand fundamentals, the restrained progress capital spending (partially as a consequence of pipeline takeaway capability restraints), ESG headwinds, and the continued avoidance by traders, as traders are nonetheless conditioned to plow funds within the broader market barometers and purchase the dip in know-how shares, which retains valuations low and compounding prospects strong, we could possibly be within the early innings of a secular bull market in power equities.

A Lengthy Time In Growth and The Begin Of A Longer-Time period Alternative

Researching, chronicling, and monitoring the chance in probably the most out-of-favor corners of the market has been a time-consuming initiative during the last couple of years, although it has proved worthwhile when it comes to relative and absolute alternative.

The next partial listing of public articles chronicles my thought course of on the focused pure gasoline equities, together with Antero Midstream (AM), and the broader creating alternative in commodity equities over the previous 12 months.

- “Southwestern Vitality: A Misunderstood Pure Fuel Producer” – Printed December thirteenth, 2019

- “Vary Assets Continues Capex Cuts, Validates Appalachia Benefit” – Printed January eighth, 2020

- “Antero Assets Is A Generational Purchase: Dispelling The Delusion Of Antero As Excessive-Price Producer” – Printed February nineteenth, 2020

- “Antero Midstream Shares Are Considerably Undervalued Too” – Printed February, twentieth, 2020

- “The Lengthy Oil, Brief Pure Fuel Commerce Is Formally Lifeless” – Printed March ninth, 2020

- “The USA Pure Fuel Fund Was Up On A Historic Down Day For Vitality” – Printed March tenth, 2020

- “EQT Corp. Surges As The Bearish Pure Fuel Thesis Is Lifeless” – Printed March seventeenth, 2020

- “EQT Main The Forthcoming Transfer Greater In Pure Fuel Costs” – Printed July twenty fourth, 2020

- “Antero Assets Is A Generational Purchase: Working By The Close to-Time period Debt Maturities” – Printed July nineteenth, 2020

- “Antero Midstream Has Outperformed All Different Midstream Companies Yr-To-Date” – Printed July twenty ninth, 2020

- “Antero Assets Is A Generational Purchase: Mapping Out The Free Money Move” – Printed October twenty eighth, 2020

- “Antero Assets Main The Approach In A Historic Vitality Fairness Rally” – Printed December eleventh, 2020

- “Not All Vitality Shares Are Created Equal” – Printed December twenty fourth, 2020

- “Antero Assets: Purchase The Forgivable Dip” – Printed August 2nd, 2021

- “EQT Corp.: Purchase The Forgivable Dip At A 20% Free Money Move Yield” – Printed August 4th, 2021

- “U.S. Metal: A Breakout Inventory For 2022” – Printed January twenty sixth, 2022

- “Peabody Vitality: A Breakout Inventory For 2022” – Printed January twenty eighth, 2022

If you happen to learn via the articles above that chronicle this journey, there was pessimism and skepticism within the commentary sections, particularly at first.

This skepticism and pessimism was evident publicly, and privately, the place many struggled to embrace such a poor performing group of shares. In my contrarian mindset, the continued pessimism and skepticism, which nonetheless exists at the moment to an extent, suppose Cathie Wooden of ARK Innovation ETF fame calling for a commodity crash within the second half of 2021, and subsequently doubling and tripling down on this name, confirms that we’re nonetheless within the early innings of this chance in pure gasoline equities, commodities, and commodity equities.

On that word, in the event you take a look at the relative efficiency chart of a broad based mostly index of commodities vs. the SPDR S&P 500 ETF, the scale and scale of the relative alternative rapidly grow to be obvious.

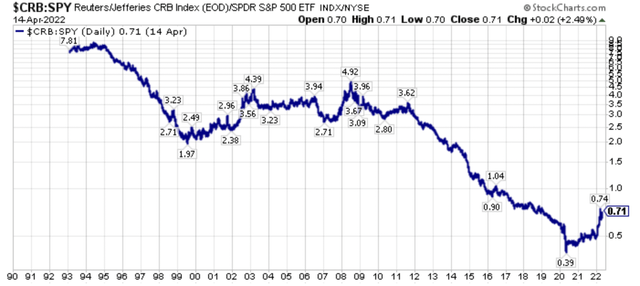

$CRB Versus SPY as of April 14th, 2022 (Creator, StockCharts)

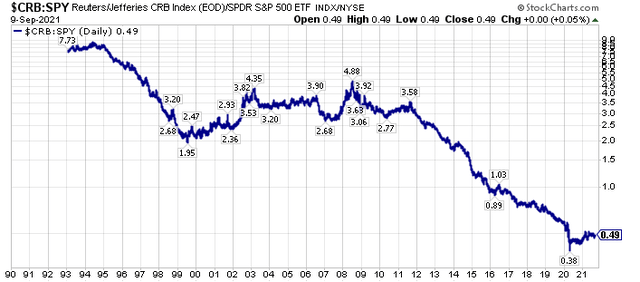

For reference, right here was the identical chart posted on September tenth, 2021 within the final replace on this sequence.

$CRB Versus SPY As Of September ninth 2021 (Creator, StockCharts)

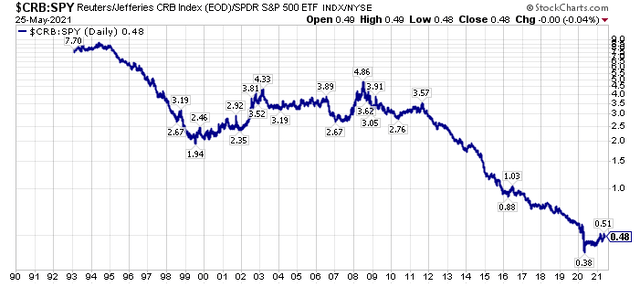

For additional reference, right here was the identical chart I revealed within the Might twenty sixth, 2021 replace. Look carefully, as even with the relative outperformance of commodities, there was solely reasonable motion on this reversion to the imply ratio. This could inform the market generalist that we’re nonetheless within the midst of a reversion-to-the-mean increased.

$CRB Versus SPY As Of Might twenty fifth, 2021 (Creator, StockCharts)

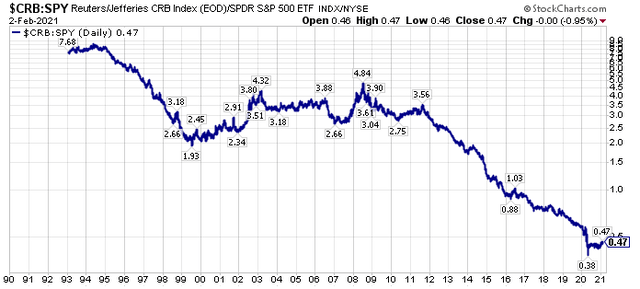

Going all the best way again, to the primary article on this sequence, right here was the identical chart from my aforementioned February third, 2021 article. The purpose is that this ratio principally stood nonetheless for the primary three updates on this article sequence, and it has moved upwards reasonably because the final replace, with vital commodity and commodity fairness outperformance.

$CRB Versus SPY As Of February 2nd, 2021 (Creator, StockCharts)

From an even bigger image perspective, commodities and commodity equities have actually had an explosive transfer from their 2020 depths. Nevertheless, within the larger image, that will have been the ultimate relative washout, and the reversion-to-the-mean commerce has the potential for lots extra room to run.

Closing Ideas: One thing Is Altering Below The Floor Of The Markets As Extra Traders Acknowledge The Commodity Bull Market

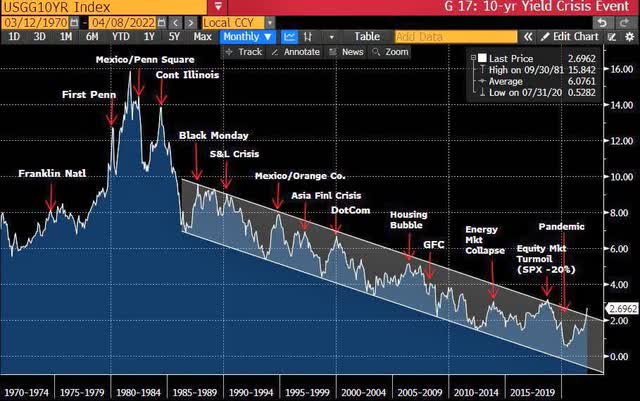

Totally different from the prior updates on this sequence, there may be positively an consciousness constructing as to the outperformance of commodities, and commodity equities collect steam. This historic capital rotation is sort of a storm constructing its power, and this storm could possibly be additional fed by a markedly totally different rate of interest surroundings than many traders have lived via for the final roughly 4 many years.

Change In Curiosity Fee Backdrop (Bloomberg, AzizSapphire)

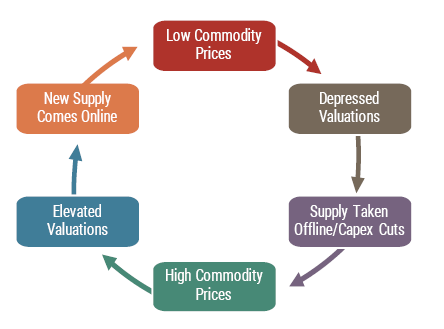

The untold story with the rise in power equities, and extra particularly pure gasoline equities, is that this can be a provide aspect story. Going additional, the capital cycle is enjoying out in actual time in pure gasoline costs, pure gasoline liquids costs, and pure gasoline equities, with pure gasoline equities considerably outperforming their FAANG friends in 2020, in 2021, and year-to-date in 2022.

Capital Cycle (GMO)

This outperformance of probably the most out-of-favor power equities, a sector I’ve been identified to beforehand name the red-headed stepchild of the already out-of-favor power sector, at the very least earlier than the latest value run-up, has actually accelerated in 2022.

With the broader fairness market nonetheless uncovered to the potential of a powerful drawdown, or maybe seven years of working in place, due to traditionally poor beginning valuations, there is a want for traders to contemplate various asset courses. Importantly, an additional drawdown within the broader markets, which could possibly be fueled by rising long-term rates of interest rising due to provide aspect commodity inflationary pressures mixed with constructing wage pressures, may speed up fund flows into commodity equities.

Why?

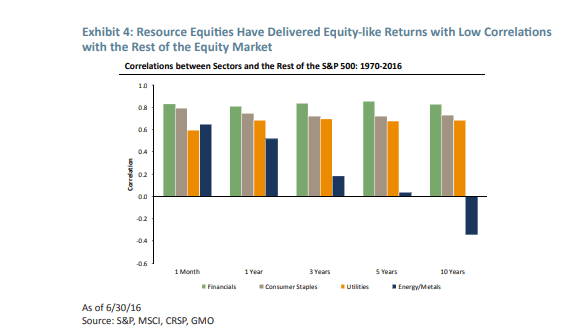

Merely put, traders shall be on the lookout for non-correlated sectors and non-correlated shares, particularly if the drawdown in each shares and bonds continues. Notably, this twin decline in shares and bonds is impairing the historically standard 60/40 portfolio in addition to the earlier very in-favor threat parity methods. On this word, commodity shares, particularly the as soon as loathed, and nonetheless typically unloved power fairness sector, actually suits the invoice as a portfolio diversifier, and enhancer, which we’ve seen play out in spades in 2022.

Useful resource Equities Provide Diversified Returns (S&P, MSCI, CRSP, GMO)

Wrapping up, quietly at first, and now extra quickly because the capital rotation has broadened in scope, we’ve seen a passing of the baton of market management. Will there be ebbs and flows to this course of? Unequivocally sure, which means anticipate relative pullbacks as traders reposition, and traders of all stripes attempt to reorientate across the inflection level that’s occurring actual time.

At this juncture, most traders are merely simply turning into conscious of this management transition that has been happening because the broader fairness markets bottomed in March of 2020, although relative and absolute value motion this 12 months in 2022 has actually opened extra eyes. Recognizing this altering backdrop after years of examine, together with being too early, I’ve been pounding the desk on the extraordinarily out-of-favor commodity equities for a number of years now, and I nonetheless suppose we’re within the early innings of what is going to be a longer-term secular bull market, albeit with vital volatility. Personally, I feel we’ll supersede the capital rotation that befell from growth-to-value throughout 2000-2007, which additionally coincided with the final secular commodity bull market which ran from 2000-2008.

Traders skittish of commodity equities ought to analysis solid apart financials as additionally they will profit from rising inflationary expectations and rising long-term rates of interest. Understanding the larger image, then having an understanding of the bottoms-up fundamentals has been the important thing to outperformance, and this can be a path that has not been simple with these taking part confirming this actuality. Nevertheless, the street much less taken is usually the higher one, and I firmly imagine that at the moment, as conventional shares, bonds, and actual property proceed to supply very poor beginning valuations and really poor projected future actual returns from at the moment’s value ranges. Extra particularly, the out-of-favor belongings and asset courses, together with commodities and commodity equities and out-of-favor particular securities, are the place the historic alternative has been, and that is the place it nonetheless stands, from my perspective.

{kind=link}