Up to date on April twenty fourth, 2022 by Felix Martinez

Enterprise Improvement Corporations – or BDCs, for brief – generally is a nice supply of present yield for revenue traders.

Primary Road Capital Company (MAIN) is a superb instance of this. This BDC has a present dividend yield of 6.1%. Higher but, Primary Road Capital Company pays month-to-month dividends.

You may obtain our full Excel spreadsheet of all month-to-month dividend shares (together with metrics that matter like dividend yield and payout ratio) by clicking on the hyperlink beneath:

The inventory’s excessive dividend yield and month-to-month funds make it a stable selection for revenue traders. However what in regards to the energy of the underlying enterprise?

Luckily for traders, Primary Road Capital’s enterprise seems to be performing nicely. This text will focus on the funding prospects of Primary Road Capital Company intimately.

Enterprise Overview

Primary Road Capital Company is a Enterprise Improvement Firm, or BDC. You may see our full BDC checklist right here.

The corporate operates as a debt and fairness investor for decrease center market corporations (these with $10-$150 million of annual revenues) searching for to remodel their capital buildings. The BDC has the aptitude to spend money on each debt and fairness, which supplies it a major benefit over corporations who spend money on personal debt or personal fairness alone.

Primary Road Capital Company additionally invests within the personal debt of middle-market corporations (not decrease middle-market corporations) and has a budding asset administration advisory enterprise.

Supply: Investor Presentation

The BDC’s company construction is slightly easy. Primary Road Capital Company operates three funds:

- The Primary Road Mezzanine Fund

- The Primary Road Capital II Fund

- The Primary Road Capital III Fund

Since Primary Road Capital Company is the operator of its personal funding funds, administration charges are stored to a minimal, which supplies it a cost-based aggressive benefit over its opponents who outsource their fund administration.

Primary Road Capital Company’s holdings are extremely diversified by each transaction sort and geography. By transaction sort, the BDC acquires most of its offers through recapitalization and leveraged buyouts. Primary Road Capital Company additionally has a really excessive diploma of diversification by business.

Progress Prospects

Primary Road Capital Company’s progress prospects come from its distinctive technique of driving funding returns. Traders who personal the inventory are rewarded because the BDC sustains its excessive month-to-month dividend and grows it over time.

On the enterprise stage, Primary Road Capital Company’s progress shall be pushed by its experience within the decrease center market phase of the financial system.

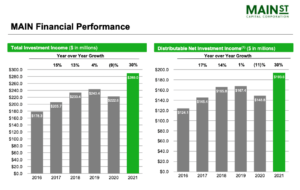

On February 24th, Primary Road Capital launched fourth-quarter and full-year outcomes for 2021. Internet funding revenue of $39.8 million was a 9% improve in comparison with $36.5 million a yr in the past. The company generated a web funding revenue of $182.7 million for 2021 a 32% improve in comparison with $137.9 million in 2020. The company generated a web funding revenue per share of $2.65, up 26% from final yr’s revenue of $2.10 per share. Distributable web funding revenue per share totaled $2.81, up 24% from $2.26 in 2020.

Primary Road’s web asset worth per share elevated in comparison with the top of 2020, from $22.35 to $25.29. The company declared month-to-month dividends of $0.215, representing an annual dividend of $2.58 per share. As of the top of the fourth quarter of 2021, the company had mixture liquidity of $567.6 million, consisting of $32.6 million in money and money equivalents, $535 million of unused capability beneath the revolving credit facility, which is able to preserve the help of its funding and working actions.

To conclude, Primary Road Capital Company has experience within the decrease center market of its business and has a budding asset administration enterprise that allows it to have robust operational leverage. These elements will drive the BDC’s progress for the foreseeable future.

Supply: Investor Presentation

Dividend Evaluation

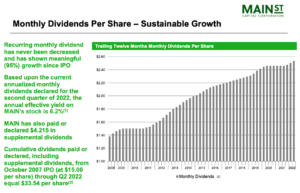

As talked about above, the corporate pays a month-to-month dividend. The corporate has been paying a month-to-month dividend because the finish of 2008. Since that point, the dividend has been rising. During the last 14 years, the corporate dividend has had a compound annual progress charge of 12.3%. We don’t count on this sort of dividend progress charge to proceed into the longer term, however we do count on the corporate to proceed to develop its dividend.

All through the years, the corporate has additionally paid supplemental dividends of $4.215. These are one-off particular dividends. We additionally count on the corporate to proceed this custom of particular dividends.

The dividend security is of concern. For instance, based mostly on earnings, the corporate had dividend payout ratios of over 100% for the final 9 years. Nevertheless, we count on the corporate to earn $2.75 per share in 2022, which is able to give us a dividend payout ratio of 94%. That is nonetheless excessive, however is sustainable.

To be able to keep away from company revenue tax as a BDC, Primary Road should distribute at the very least 90% of its taxable revenue, leaving little wiggle room to fund progress. Whereas this technique has labored extraordinarily nicely because the final recession, we do warning that this technique of funding turns into considerably much less engaging (and costlier) in lesser occasions.

Supply: Investor Presentation

Remaining Ideas

Though Primary Road Capital Company is off-the-radar for many dividend progress traders, this BDC has a powerful historical past of delivering substantial shareholder returns.

The agency’s robust observe document of superior funding administration and experience within the decrease center market phase offers it a powerful aggressive benefit within the personal fairness and debt business.

Additional, Primary Road Capital Company is shareholder-friendly with a excessive yield and month-to-month payouts. The inventory’s excessive yield and month-to-month dividend funds is perhaps appropriate for revenue traders, though the modest anticipated charge of return of seven.4% over the following 5 years coming largely from the excessive dividend yield of 6.2% retains the inventory as a maintain suggestion proper now.

Additional Studying: 5 No-Brainer BDCs Yielding Extra Than 5%

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

{kind=link}