Olemedia/E+ by way of Getty Pictures

The GitLab Funding Thesis

GitLab Inc (NASDAQ:GTLB) is an organization with vital development potential as a result of its market place and a possible TAM of greater than $40 billion. On the time of my final article, nevertheless, the inventory had taken an enormous hit after steerage got here in worse than anticipated. Happily, the inventory was capable of bounce again from the weaker-than-expected steerage and even raised steerage above what was anticipated on the time.

The primary half of the fiscal 12 months was additionally very sturdy from a enterprise perspective, however that’s nonetheless not sufficient for me to boost my ranking, regardless that the corporate is extremely sturdy.

Temporary Overview Of The Enterprise And Aggressive Scenario

GitLab Investor Presentation

GitLab and GitHub, which is owned by Microsoft (MSFT), are the 2 dominant gamers within the Git market. Git principally signifies that a number of folks can work on the identical factor with out interfering with one another.

Atlassian (TEAM), with its Bitbucket software, can also be available on the market, however in my view, performs a reasonably minor function in comparison with GitLab and GitHub. GitLab’s differentiator is its deal with a single platform that goes past conventional code internet hosting and collaboration choices. As a result of it’s a single platform, licensing prices are decrease for purchasers as a result of they solely want GitLab and never a number of different functions. Plus, this additionally retains the combination prices low.

The issues that GitLab does, or that you are able to do with GitLab, are planning and collaboration, publishing and monitoring, and bug monitoring and fixing. Then there’s steady enchancment and steady supply, and final however not least, safety. Particularly, safety is a powerful differentiator proper now, and I feel GitLab is a step forward of the competitors on this space.

One other benefit over GitHub is that you’ve got extra management over your knowledge and repositories as a result of they are often hosted domestically. GitLab has a variety of options that GitHub requires you to make use of third-party instruments for. However on the whole, like Visa (V) and Mastercard (MA) in one other house, they’re each very sturdy gamers that dominate the market. GitHub additionally has its benefits in some areas. For instance, it’s usually mentioned that GitHub is meant to be quicker.

GitLab’s Q2 Outcomes

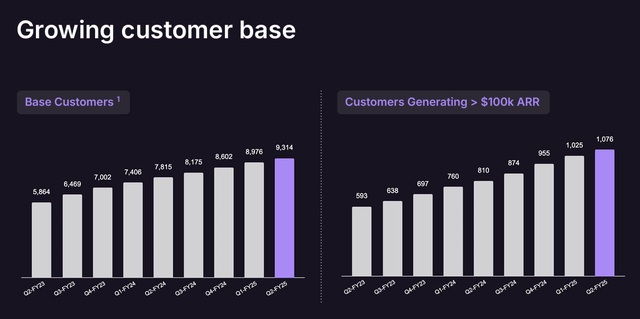

GitLab Investor Presentation

Purchasers with greater than $5,000 ARR elevated by 19% 12 months over 12 months, and purchasers with greater than $100,000 ARR noticed a implausible 33% year-over-year development to 1,076 purchasers. This, mixed with income development of 30.8% 12 months over 12 months, is a implausible consequence that many wouldn’t have anticipated given the downwardly revised steerage firstly of the 12 months.

GitLab Q2 Outcomes

Particularly, the steerage for FY25 has been very encouraging. At first of the 12 months, the steerage was weak, forecasting solely $0.22 per share, whereas analysts had been anticipating $0.37 per share. In Q2, the steerage was raised to $0.34 to $0.37 and is now at $0.45 to $0.47, properly above the initially anticipated $0.37.

The detrimental for me is that the steerage for shares excellent is 168 million. Since they’re at the moment at 158 million, we are able to anticipate the SBC to proceed to develop.

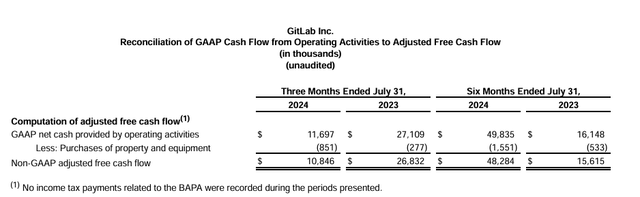

GitLab Q2 Outcomes

At first look, FCF seems to be good as a result of it’s considerably larger than final 12 months: $48 million this 12 months versus $15 million final 12 months. Sadly, SBCs are nonetheless so excessive that SBC-adjusted FCF continues to be detrimental.

- FCF $48m – $91m SBC = SBC adjusted = – $43m

- FCF $15m – $78m = SBC adjusted = -$63m

However regardless that SBC adjusted FCF continues to be detrimental, there’s a optimistic development, and it’s doable that FCF might be optimistic within the subsequent fiscal 12 months even after the adjustment.

GitLab Q2 Outcomes

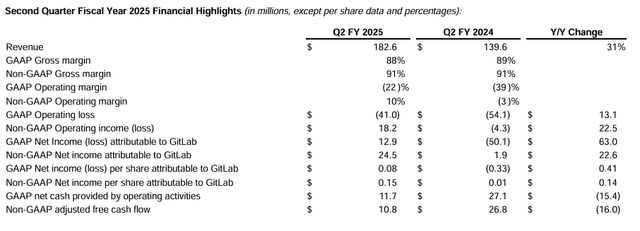

Total, there are optimistic developments. The GAAP working margin, whereas nonetheless detrimental, improved to -22% and the working loss decreased by $13 million to -$41 million. Though FCF in Q2 was decrease than a 12 months in the past, it was up sharply in H1, as proven above. Nevertheless, it is a quantity to look at in Q3 to see if FCF weakens once more in Q3.

GitLab Q2 Outcomes

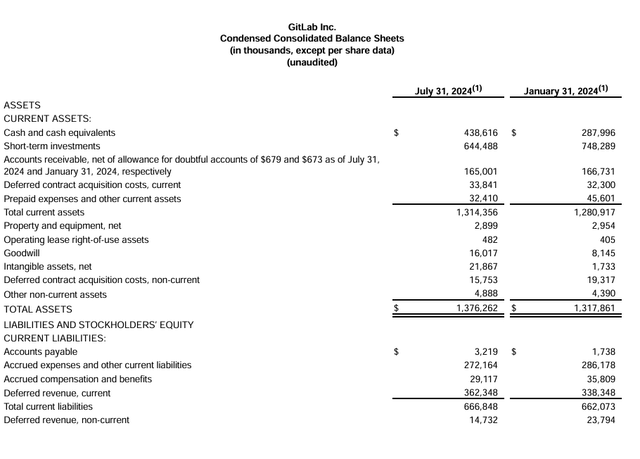

I do not suppose there are any huge surprises within the steadiness sheet. Money and money equivalents elevated from 1,036,285 to 1,083,104, which is a optimistic improvement, and debt stays at zero. Receivables are comparatively flat and payables are up, which, I feel, can also be an indication of improved capital effectivity.

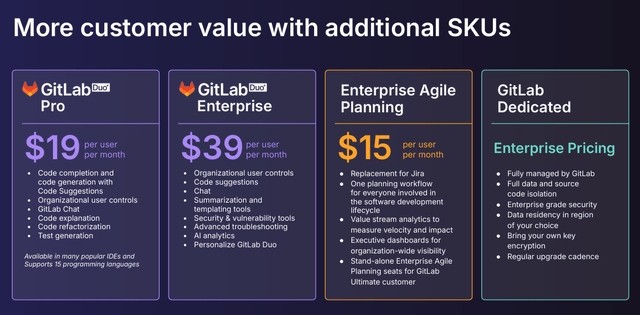

GitLab Investor Presentation

We are able to additionally see the pricing for GitLab Duo and what’s included in Duo and Devoted to have a present overview. At this level, it needs to be famous that GitLab stands out from the competitors by way of options, however that is additionally mirrored within the costs.

On a optimistic be aware, Gardner’s AI efforts usually are not going unrecognized, as GitLab was acknowledged as a pacesetter in Gardner’s new discipline of AI code assistants.

GTLB Q2 Earnings Name

GitLab’s earnings calls are all the time fairly fascinating as you get to listen to lots in regards to the enterprise and, extra not too long ago, about AI and the advantages GitLab sees for its clients by way of quicker, extra environment friendly work or figuring out sources of errors.

GitLab predicts that there might be a shift in how AI is used, from reactive to proactive, and that autonomous brokers will play a bigger function sooner or later. And it seems to be like GitLab can compete very properly with Copilot. Additionally, SaaS is already at 28% of income as a result of they’ve a 46% development price. GitLab can also be doing very properly within the complicated safety house with their devoted providing.

The value will increase may even proceed to affect revenues within the coming months, as not all clients had been capable of renew their contracts on the identical time and revenues will due to this fact range relying on the timing of the renewal course of.

It was additionally talked about that traditionally Q1 is the weakest quarter and This autumn is the strongest quarter, so I feel the steerage for the total 12 months is conservative and will doubtlessly be exceeded.

Valuation

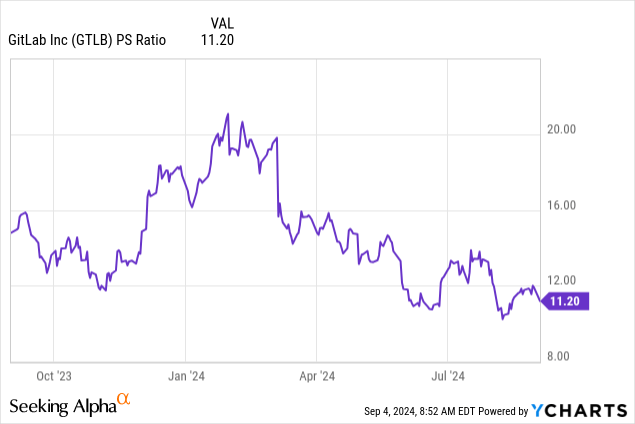

GitLab continues to be richly valued, however at the moment, the expansion charges justify the excessive valuation, and in contrast to earlier than, the valuation has already improved. The times of 20x+ PS multiples had been actually overdone.

Now, nevertheless, with a ~11x PS a number of for long-term traders, the valuation needs to be truthful when you’ve got a 5-10 12 months horizon. As a result of GitLab is so dominant in what they try this they are going to develop into the valuation.

Conclusion

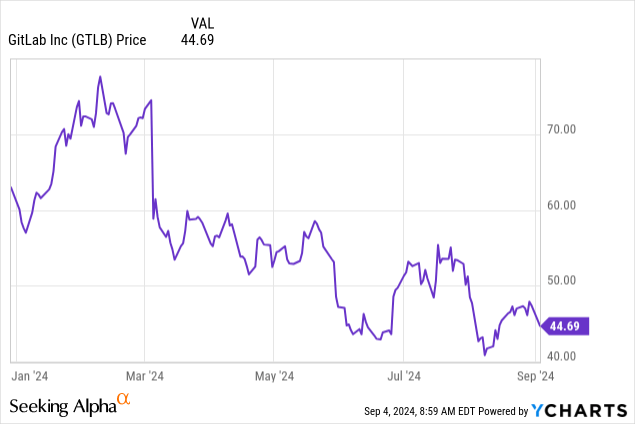

The instance of GitLab and its inventory value illustrates as soon as once more the necessity to separate inventory value from enterprise efficiency. Though the inventory’s YTD efficiency has not been nice, GitLab’s underlying enterprise has delivered implausible outcomes.

Due to this fact, I take into account the shares far more enticing as we speak than firstly of the 12 months. For an improve to Purchase, nevertheless, I nonetheless want a number of extra quarters to have the ability to higher assess FCF and the affect of AI.

")

")

{kind=link}