John M Lund Pictures Inc

Funding Thesis

Fortinet’s (NASDAQ:FTNT) lately concluded Q2 quarter was an enlightening revelation.

On one hand, the billings slowdown endured simply as I famous in my earnings preview of Fortinet’s Q2 quarter, with Fortinet’s administration conserving full-year CY24 billings steerage unchanged from their earlier quarters.

Then, then again, administration shocked everyone with a high-octane growth of consolidated enterprise margins throughout the board pushed by elevated operational effectivity by way of its enterprise and the primary doable indicators of demand returning again to its merchandise, comparable to firewalls and safety home equipment.

These indicators had been additionally seen in stock ranges that confirmed sturdy enhancements for the primary time in years, pointing to indicators of demand weak spot for Fortinet’s {hardware} merchandise lastly stabilizing.

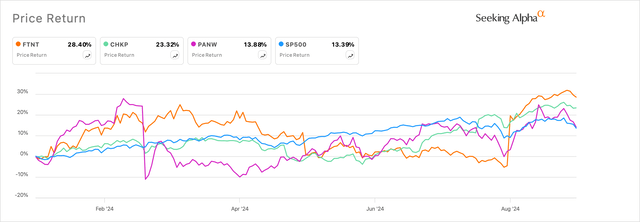

The strong shock that Fortinet delivered was ultimately seen within the firm’s inventory worth, which surged proper after its Q2 earnings report.

Exhibit A: Fortinet’s inventory worth is up 28% all thanks as a consequence of a sturdy Q2 earnings report. (Searching for Alpha)

For my part, the corporate’s Q2 report was an enormous enhance to the corporate’s outlook when it comes to its margins, on the very least aided by a doable backside within the contraction of Fortinet’s firewall and product enterprise.

I’m upgrading Fortinet to a Purchase.

Billings Slowdown Nonetheless Persists, However Slowdown in Product Income Normalizes

In my earlier protection, I did anticipate a tempered outlook in Fortinet’s prime line, primarily as a consequence of two elements:

First, the dearth of chest-thumping that administration normally does when parading its huge gross sales offers at any alternative they get. The delicate/reasonable tone of gross sales offers continued within the Q2 name, the place administration spoke about lumpiness and lengthy gross sales cycles paired with an enhancing gross sales effectivity outlook as Fortinet absorbed the gross sales groups from its latest Lacework and Subsequent DLP acquisitions. Nonetheless, administration did spotlight just a few 7-figure offers on the decision.

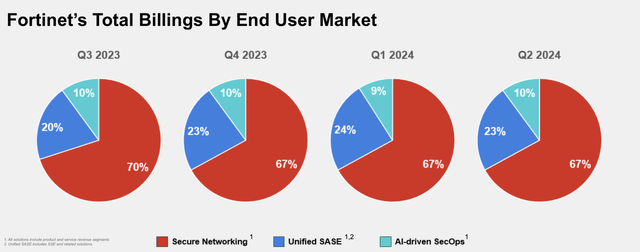

Second was the continued range-bound momentum of their Unified SASE and AI SecOps Billings, which flatlined after quickly rising final 12 months, as famous in Exhibit B beneath.

Exhibit B: Fortinet’s Billings By Finish Person Market Options (Investor Presentation, Fortinet)

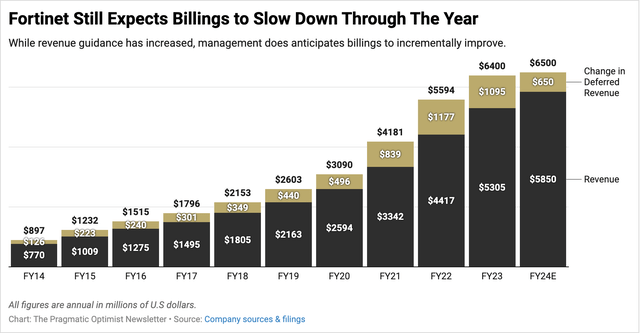

I did anticipate administration to revise their billings steerage greater, no less than after accounting for the inorganic carry that the Laceworks and Subsequent DLP acquisitions would give the corporate’s consolidated billings. Sadly, administration held the CY24 billings goal within the vary of $6.4-6.6 billion by mentioning that the inorganic carry in billings as a consequence of acquisitions was small, therefore no change in billings.

Exhibit C: Fortinet’s Billings greenback quantity by 12 months together with its 2024 goal vary (Firm sources)

One of many surprises within the prime line was the slower than anticipated decline in its product income, which dropped simply 4% to $452 million within the quarter, significantly better than I anticipated. This was as a consequence of better-than-anticipated gross sales of the corporate’s firewall merchandise and different safety home equipment and software program licenses. Service income, which incorporates merchandise within the SASE house, continues its sturdy double-digit progress, rising 20% to $982 million, however I used to be shocked by the large enchancment within the firm’s product income, which contracted at charges significantly better than I feared.

The reversal in product income contraction is nice information for Fortinet, which ought to now enhance total income progress for Fortinet, which was being pulled up by the double-digit progress charges seen in its service section.

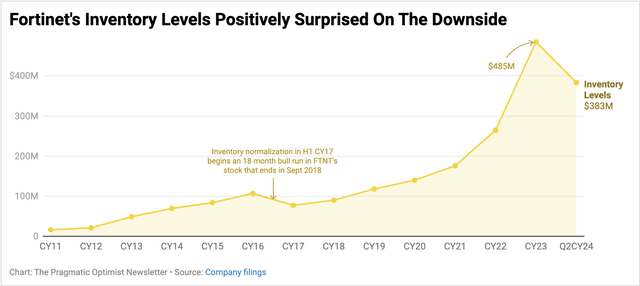

The smaller contraction development in Fortinet’s product income is also confirmed by Fortinet’s stock ranges, which for the primary time in lots of quarters dropped, pointing to indicators that there’s a reversal within the weak demand that was plaguing Fortinet’s income progress.

Exhibit D: Fortinet’s Stock ranges fall for the primary time in lots of quarters. (Firm filings)

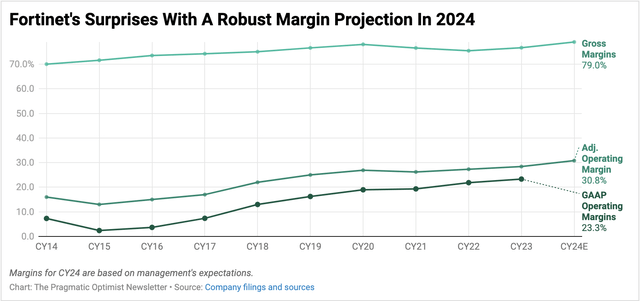

Margins On Steroids: The Huge Takeaway

What Fortinet’s enhancing stock ranges have really accomplished, aside from enhancing top-line progress, is boosted the general margin profile of the corporate because it ships extra product out to its prospects.

Exhibit E beneath attests to that remark, the place margins throughout the board bought a robust enhance as a consequence of falling stock ranges.

Exhibit E: Fortinet’s Margins On Steroids With Strong Enlargement (Firm sources)

On the earnings name, most analysts had been pleasantly shocked by the margin acceleration. Right here is administration’s response to the primary query of the earnings name that began with understanding the margin enhance:

I believe the gross margin is the most important driver of what you noticed within the working margin, significantly once you have a look at it on a quarter-over-quarter foundation and in that, we talked about or made reference to a extra normalized atmosphere for us when it comes to stock ranges, turns and what we’re seeing with channel stock but additionally commitments to our contract producers. So I believe that we have been working by way of that for in all probability the final 3 quarters, possibly 4 quarters. And with that, I might say, I believe we have returned to a extra regular state and so I might anticipate that to proceed on.

As famous in Exhibit E, Fortinet normally manages its enterprise nearer to the ~27% working margin degree. That is additionally what I had modeled in my earlier valuations, however with administration sounding extra optimistic about managing its enterprise shifting ahead on the new normalized vary of margins as demonstrated in Q2, I’ve raised my earnings outlook for Fortinet, which additionally boosts the valuation premium for the cybersecurity firm.

Add to this outlook the rising scope for margins as a result of elevated margin profile of Fortinet’s service income section, and I can simply see how margins have room to develop by no less than 22-25 bp over the following 10 calendar quarters.

Right here is a few extra forward-looking commentary from administration that’s pertinent to the idea of my valuation mannequin:

Additionally, we’ll profit from the service income which has a a lot greater margin in comparison with the product income. So as soon as the product begins rising, as a result of the product has a decrease gross margin, that in all probability will influence the margin however the product can be the main indicator of future service. In order that’s the place we sort of additionally had been completely happy to see the product additionally beginning rising now which I believe going ahead with the product has a better share, that in all probability additionally will influence the margin.

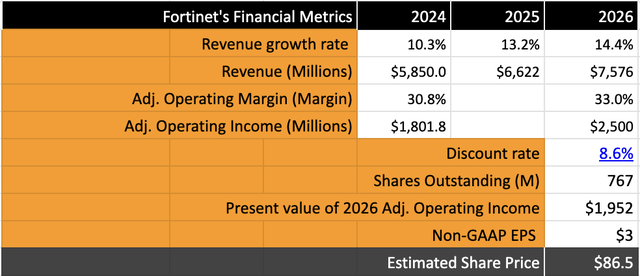

Fortinet’s Valuation Upgraded On Robust Working Leverage

With no change in billings but, I’m nonetheless leaving my income targets unchanged for CY25 and CY26, whereas I’m upgrading Fortinet’s CY24 targets to reflect administration’s steerage. This suggests 12-13% CAGR in top-line progress by way of CY26.

Fortinet’s mannequin now will get a lift as a result of working margin growth, the place I anticipate margins to develop by 220 bp by way of CY26 based mostly on my remark within the earlier part. This factors to an 18% progress in adjusted earnings, which means a ahead valuation a number of of ~34x.

Exhibit F: Fortinet’s valuation mannequin exhibits upside (Writer)

My mannequin assumes a reduction charge of 8.6% and a share dilution charge of half a % to 1%. Administration indicated that there was no share repurchase exercise in Q2.

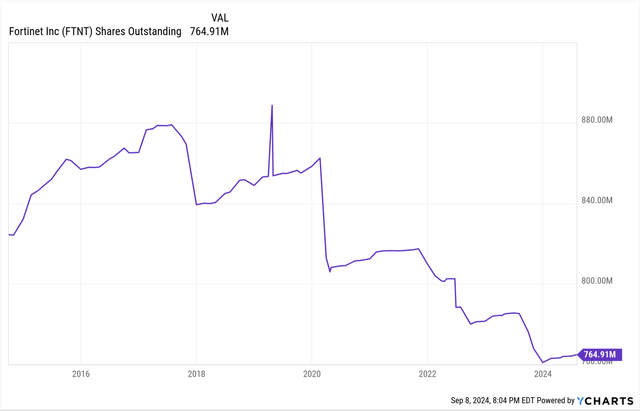

Nevertheless, their ahead steerage did point out that they’d exit 2024 with shares excellent within the vary of 767-777 million, which means their share base would contract by 1.4-2.6% y/y in 2024.

I believe administration may make the most of the remaining $1 billion of its buyback authorization to repurchase shares this 12 months itself. If administration does affirm that, anticipate one other enhance to the inventory worth.

Exhibit G: Fortinet’s shares excellent traits decrease. (YCharts)

I additionally anticipate administration to announce a brand new share buyback program within the subsequent two quarters after administration exhausts the remaining $1 billion of its earlier buyback program.

Dangers & Different Elements To Take into account

The important thing now might be to observe for Fortinet’s stock ranges, and any additional drop will affirm an inflection of their firewall product enterprise. Assuming their service enterprise continues to develop within the double digits, the inflection of its product enterprise might be an enormous enhance to the corporate’s outlook.

Fortinet is anticipated to host an Analyst Day in just a few months on November 18th, the place I anticipate administration to positively replace its midterm mannequin with revised estimates on progress charges and margins. A few of these hints had been strongly alluded to within the Q2 earnings name itself.

Fortinet’s administration will even be taking part in Goldman Sachs’ Communcopia Tech convention occasion tomorrow, which can additionally transfer the inventory.

Takeaway

To reiterate my key takeaway from Fortinet’s lately concluded Q2 quarter, there is no such thing as a higher approach to characterize the earnings report aside from saying that the cybersecurity’s margins look to be on steroids. The development in Fortinet’s product enterprise factors to an inflection and, coupled with the sturdy progress in its service enterprise, is including immense firepower to the corporate’s earnings outlook greater than its gross sales outlook.

I anticipate Fortinet to be a winner within the subsequent few months, and I’m upgrading this inventory to a Purchase.

Q3 2023 Earnings Call Transcript")

{kind=link}