Alexandros Michailidis

Dear readers/followers,

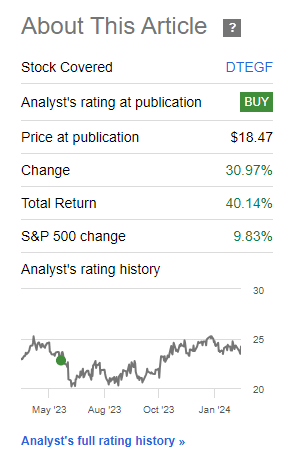

You may recall my work on Deutsche Telekom (OTCQX:DTEGY) which resulted in a sector-specific outperformance for this company (specific to the communications sector) over 30% RoR since my first article. In fact, if you go back to January of 2022, which is when I established my position in the company, the company has generated significant outperformance to the somewhat tepid S&P500. You can find my last article on the company here.

Seeking Alpha Deutsche Telekom (Seeking Alpha)

Obviously this has been a successful investment. That’s also why I took some profits (like I said in another article with regards to my rotation price), and maintain a position in the business today that is only half the size of what it once was. The rest of the capital has moved “onto greener pastures”, more undervalued companies and in most cases has seen growth behind that seen in Deutsche Telekom. You can find my last article on Deutsche Telekom here.

For this article, I am going to be updating my thesis on what I believe to be one of the better communications businesses in all of Europe. I own a wide variety of telcos – from Swedish Telia (OTCPK:TLSNF), Tele2 (OTCPK:TLTZF), and Norwegian Telenor (OTCQX:TELNY), but also French ones like Orange (ORAN), or American giants like Verizon (VZ). I no longer hold a stake in AT&T (T), but would get into this business at a lower valuation as well.

It’s all about that valuation for me.

And the valuation for Deutsche Telekom, while an attractive company, is not fantastic any longer.

Deutsche Telekom – An attractive upside made smaller by valuation improvements

Going into this article, I was actually fairly curious what the valuation outcome would be and how my targets would hold up in light of profit forecasts, and my own financial modelling. I am happy to say that despite some more uncertainties and having to discount higher owing to both what is available on the market in terms of “risk-free” rates and what I believe to be a smaller growth rate going forward, Deutsche Telekom remains a very conservative but qualitative business.

In terms of subscribers, Deutsche Telekom is by far the largest subscriber base company that I own. At over 300M+ subscribers including tens of millions in fixed network and broadband customers, Deutsche Telekom is one of the largest communications businesses on the planet. What was previously T-Mobile, T-home and other segments have been merged into this – and that’s even before considering the NA portion of the company, with T-Mobile US (TMUS).

What other upside and positives do the company have?

Well, BBB+ from all major rating agencies for one. Over €16B in free cash flow, a new buyback program, and T-Mobile US has launched a dividend, which is something I forecasted in my last couple of articles. The company has delved into AI with its German Chatbot, and the merger synergies with T-Mobile have exceeded expectations. (Source: Deutsche Telekom IR)

On the infrastructure side, Deutsche Telekom is a leading player in global 5G.

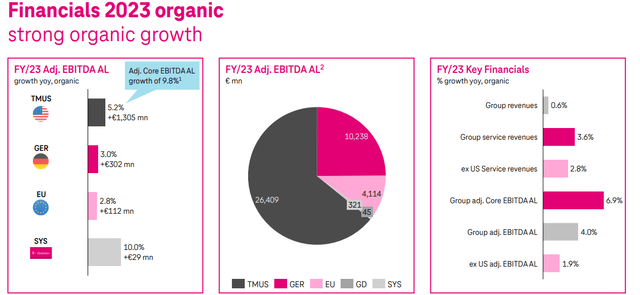

2023A was a good year for the company. Revenues were up 3.6% year-over-year, with group EBITDA AL up almost twice that, contributing to that significant €15B+ free cash flow for the year. DT has also managed to maintain its customer momentum, with guidance achieved not only in the NA side, but in EU as well.

The company has sized up its TMUS stake as well. From the 40’s, the company now has an official majority position at 50.7%, and this is despite new share issuances. As such, DT now controls in full, TMUS. (Source: Deutsche Telekom IR)

The company’s new dividend, with the bump to €0.77/share, means that we’re now at a yield of around 3.5% at about €22/share, which is where the company currently trades. That’s one of the drawbacks at the company. If you’re in Europe, like me, you’re likely to be able to get at least 3.75-4% from a safe savings account, which makes the dividend if not negligible, but at least not that attractive – not when other large telcos pay at least twice that.

However, on the operational side, there aren’t many things that could be considered negative. In fact, not a single segment went negative for the year.

Deutsche Telekom IR (Deutsche Telekom IR)

In terms of specific segments, the company’s Network segment saw on-track development, expanding its 5G leadership across the world and across its various geographies.

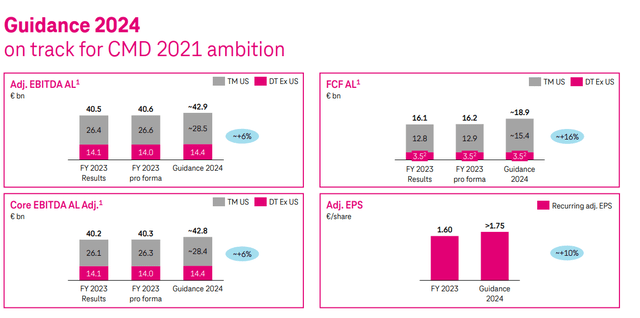

We also have a 2024 guidance to look at for the company, which comes to a mid single digit growth rate, of 6% for EBITDA growth and 16% in FCF.

Deutsche Telekom IR (Deutsche Telekom IR)

There is a consistency to the company’s growth as it is today. I mean that the company is growing in all categories, with postpaid phone, internet as well as FTTH. The company’s churn actually went up for the US segment – close to 1% as of the end of the year, which is probably the only real negative you can find in the results – and that negative is really related to seasonal churn, not in any way worrying trends or trends outside of the normal level.

Just how good are the company’s trends?

Look for example at Germany, one of the core markets. This latest quarter marks the 29th consecutive quarter of company EBITDA growth for this area. (Source: Deutsche Telekom IR)

Europe as a whole delivered the 24th consecutive quarter of growth. Unlike smaller and riskier positions, such as my play in Vodafone (VOD), Deutsche Telekom is a characteristically conservative “grower”. The company’s higher rate of growth has also been made possible by lower CapEx numbers, in particular in the US segment. (Source: Deutsche Telekom IR)

Net debt is now at a level of 2.3x excluding leases. With the reduction in net debt, what I would call Deutsche Telekom here is a reliable grower with consistent and conservative upside.

I see upside specifically both on the commercial and on the consumer side, with continued growth seeming almost a certainty, even if the overall rate is well below 10% per year.

Back when I first wrote on DT, the company worked with its 2021E CMD targets, all of which are currently well on track given these results.

Risks & Upside to Deutsche Telekom

Finding operational risks for Deutsche Telekom that are of significance is not an easy task – beyond that dividend and the upside that results in – but there are some.

Competition in Europe, especially in its home market (specifically Vodafone) is investing higher amounts of CapEx to catch up in broadband and cable. This could force a need for DT to step-up its CapEx to keep pace in order to not lose market share. Beyond that, I could speak of how the market for regional licensing for the 2.5 GHz spectrum in US is fragmented and, unlike Europe, is owned and in turn leased by educational institutions of all things. Because of decentralization of this market, this opens it up to being captured by new competitors easier than if, like in Europe, the spectrum is acquired from relatively few parties.

Beyond that, I must admit that I struggle to find real operational risks. The upsides to this company are many. I don’t think it an overstatement to call the Sprint/TMUS mobile merger an absolutely revolutionary one in the US market, with superb scale, synergies and spectrum. The returns from this should continue on for at least 3-5 years, possibly even more. In its home market, DT has what some consider to be a market position that is hard to approach given the company’s optimization.

Unlike many other telcos and their search for RoR, DT’s management has shown exceptional capital allocation ability, combining discipline and patience. Just look at the several times it refused to buy Sprint until the company was at the price they wanted.

Also, unlike the rush that some operators have shown, DT is in absolutely no hurry to sell or monetize its tower arm.

With that, I’m ready to show you my upside.

Deutsche Telekom – Upside in the longer term

In my last article, I gave the company a conservative price target of around €24/share. This was at a different interest rate outlook, but it was also before the company beat my own estimates and expectations for the full year.

The company currently trades at a €21.8/share. This is neither what I would consider excessively cheap at today’s results, nor is it prohibitively expensive. At today’s price, and given my €24/share price target, (Here are some of my previous articles where I go through these targets more in detail – Link 1, Link 2)

DT trades at over 13x P/E. That is high for a Telco, with many European telcos trading under the 10x mark. The company’s yield is also on the low side, but you will not find many telcos with this level of operational excellence, and proven excellence.

However, forecasting it at its current P/E, even with a forecasted EPS growth in the higher single digits, this fails to produce the desired (and targeted by me) 15% annualized, in no small part due to that lower dividend.

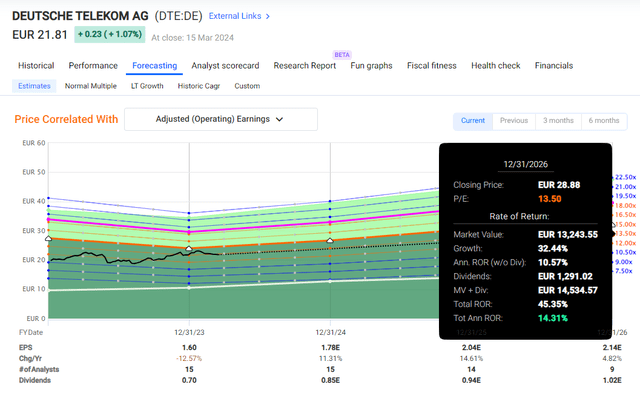

F.A.S.T Graphs DT Upside (F.A.S.T graphs)

And 13x P/E can be considered an accurate or likely level for this company to track going forward because it is in fact the 6-year average trading level for Deutsche Telekom. Only if you estimate the company higher, would it in fact deliver outperformance here. (Source: FactSet).

Other analysts following Deutsche Telekom consider the company somewhat undervalued – much like me. Morningstar gives the company a FV of €25/share (Source: Morningstar). 21 analysts follow this company, and all but 4 of those consider this company a “BUY” or “Outperform” rating, with a low-end rating of €20 and a high-end rating of €31, and an average for those analysts of close to €26.8 (Source: S&P Global).

Between beating my expectations, and a higher risk-free rate, I’m not changing my price target here and instead continue to view Deutsche Telekom at a PT of €24/share – as you can see, below where most analysts have it. This is explained by a higher discount rate – I can literally get a better interest rate than DT from a savings account.

I have been hoping to see a sub-€20/share price for some time, at which point I would call the company “cheap”.

For now, closing on 2023A, the company is attractive, but not cheap, and I still see it possible to make a double-digit annualized RoR here. For that reason, I remain at “BUY” with the following thesis

Thesis

- Deutsche Telekom is one of the more qualitative and price/mix-appealing telco businesses on earth. While it does have somewhat higher leverage and lower credit rating and yield than some of its peers, it makes up for this with a potential longer-term upside and growth that is outside the 1-2% norm found in the sector.

- I believe Deutsche Telekom can be bought with ease and as a “STRONG BUY” at anything involving a €1X native share price, which we currently do not have.

- When the native share price reaches above €21/share, things look somewhat different. It’s still a “BUY”, and I put the PT around €24/share long-term, but at over €21/share, your returns are looking likely to include single-digit RoR, or low-double, sub-15% annualized RoR.

- I’m still at a “BUY” for the company.

Remember, I’m all about:

1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Deutsche Telekom is no longer cheap – but it’s decent enough with a good upside, and I maintain my “BUY” here.

This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

")

")

{kind=link}