Market volatility is being blamed on varied Fedspeak – most just lately Lael Brainard, stating half-point will increase are going to be wanted to tamp down inflation.

Shade me skeptical.

I assume most explanations of market motion are a mixture of narrative fallacy and hindsight bias, with a smidgen of unintentional accuracy. The present explanations appear to suit into that

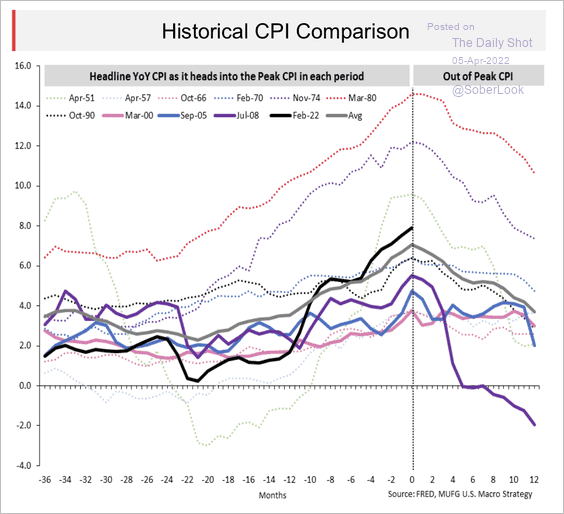

To evaluate the probability that these are something greater than Fed jawboning, and the rationality of the hindsight rationalization for volatility, think about the assorted elements that make up CPI inflation.

Vitality: Breakdown the rise in vitality costs into 2 phases: 1) The affect of return to workplace and reopening submit pandemic, with way more driving and air journey interval and a pair of) the current spike attributable to Russia’s invasion of Ukraine.

New and used autos: Bringing the complete world capability of producing semiconductors again on-line continues to be an achingly gradual course of. It’s a key think about rising car costs. (U.S. legal guidelines don’t enable cars to be offered minus chips which management security programs — ABS, airbags, and so forth.) The provision scarcity of latest automobiles (at similar demand) has led to cost will increase in new autos. Used automobile costs are tied to new car costs, however maybe much less apparent is that every one new automobiles develop into a part of the long run used automobile provide. Therefore, even after new automobile provide ramps up the scarcity of used (cheaper) autos is more likely to persist. Observe: Ukraine provides about half of the world’s neon, a key element in semiconductor manufacturing.

Meals (House): Russia and Ukraine provide roughly 28% of wheat merchandise to the world. An outbreak of Avian flu has led to a really timed mass slaughter and lack of chickens; a scarcity of beef is blamed on all the things from greater feedstock costs, industry-driven regulation, and elevated demand. Even weedkiller has risen in worth.

Different: A catchall class that features such numerous items and companies as tobacco, haircuts and funeral bills. Can we blame a Covid-created world scarcity of coffins for driving this part greater?

Eating places: Elevated meals costs to make certain, but in addition elevated wages (and well being care prices) are key drivers of restaurant worth will increase. And that’s earlier than we get to some extent the place landlords consider they’ve the flexibility to boost rents on new or renewed leases.

Shelter: The information right here is simple to misconstrue attributable to 1) Proprietor’s Equal Lease, which tends to understate inflation; and a pair of) The year-over-year collapse after which restoration, which tends to overstate lease enhance. Case Shiller at 20% means that costs have risen robustly.

Ask your self this straightforward query: Which of the above worth will increase are extremely conscious of Federal Reserve Curiosity Charge hikes?

None.

Ever since we started seeing 7% and eight% CPI prints, the Fed has had a number of alternatives to hike charges aggressively – at any of the 4 conferences since (November, December, January, and March) or any time between conferences.

That they selected to not and hiked solely 25 bps in March, suggests they perceive this fully.

They need to normalize charges with out inflicting a recession.

I believe Jerome Powell believes (hopes?) now we have already hit peak CPI, and that an natural fall-off is probably going within the close to future. It explains a lot of what now we have seen and heard.

Modifications in rates of interest function on an immense lag of 6 to 12 months. A smooth touchdown relies upon upon gauging what the affect of the modifications you made months in the past could have months sooner or later whereas ignoring the screaming headlines at present within the face of intense political stress.

The Fed Chair should relate to Hippocrates, who describes the doctor’s job as to “First, do no hurt.”

If solely pundits had comparable obligations…

~~~

Fed minutes are launched at present at 2:00 pm.

Beforehand:

Normalization vs Inflation (March 14, 2022)

Evaluating Stimulus: Financial vs Fiscal (GFC vs C19) (March 11, 2022)

Transitory Is Taking Longer than Anticipated (February 10, 2022)

Structural or Transitory? (November 23, 2021)

Deflation, Punctuated by Spasms of Inflation (June 11, 2021)

{kind=link}