Sean Gallup

As expected WeWork (OTC:WEWKQ) filed for Ch.11 bankruptcy in New Jersey on November 6 (case 23-19865). Included in the Declaration by CEO David Tolley (docket 21) is the restructuring support agreement – RSA (the RSA begins on page 47 of 180 pages and the RSA term sheet begins on page 95). Under the RSA current WeWork shareholders, except SoftBank Group (OTCPK:SFTBY), get no recovery and the shares will be cancelled on the plan effective date, which at this time is expected to be in early March. Debt will be reduced by $3 billion and so far about 61 current office leases are being rejected.

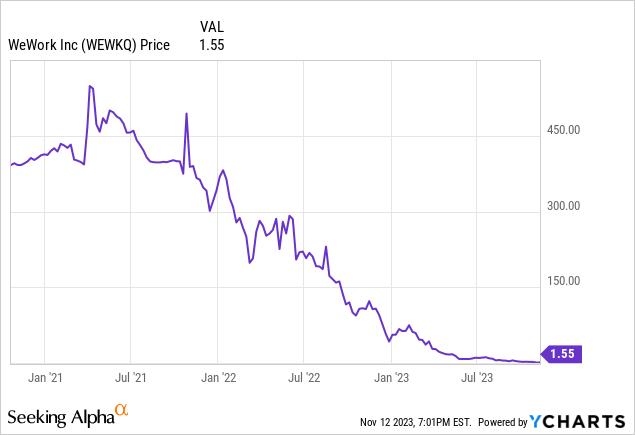

(Note: there was a 1 for 40 reverse stock split effective 9/1/2023)

Recoveries Under the RSA

Class 9 Parent Interests (current WeWork shareholders) Recovery:

Each Holder of Interests in the Reorganized Company, shall have such Interest cancelled, released, discharged, and extinguished and such Interests will be of no further force or effect, and Holders of such Interests shall not receive any distribution on account of such Interests (for the avoidance of doubt, other than any equity Interests held by the SoftBank Parties with respect to which a SoftBank Party contributes its Claims in exchange for the retention of its equity Interests)

The WeWork shares will be cancelled on the plan effective date for all shareholders except SoftBank. Some shareholders may assert that it is completely unfair that SoftBank does not get their shares cancelled and that this violates section

1123(a)(4) which states:

“provide the same treatment for each claim or interest of a particular class, unless the holder of a particular claim or interest agrees to a less favorable treatment of such particular claim or interest”.

These shareholders may further assert that they have not agreed to this treatment. (Actually, shareholders are not even being allowed to vote and have been deemed to reject.)

I expect this to be litigated. SoftBank, however, is NOT receiving a recovery specific to their Class 9 interest (WeWork shares). SoftBank is being allowed to keep their shares as recovery for their higher priority debt claims. That is a huge difference. New Jersey is in the Third Circuit and I could not find case law in that specific circuit, but other circuits have ruled on this issue and other somewhat similar issues, including the Peabody Energy (BTU) case, which many on Seeking Alpha followed a few years ago. I still, however, expect a nasty fight.

There is also the potential for different way to handle SoftBank’s priority claims. A plan could give SoftBank stock in the new WeWork for their debt claims and cancel their current WeWork stock along with the other current shareholders. There might be some potential tax issues, which are beyond the scope of this article, that would be more favorable for SoftBank to continue to own their current shares instead of getting new stock for their debt.

*3L notes (Class 6), unsecured notes (Class 7), and general unsecured creditors (Class 8) basically get what they would get under a liquidation of WeWork, which most likely will be nothing or at the most a token amount.

*LC facility claims and 1L notes (Class 4) and 2L notes (Class 5) get some of the new equity.

*DIP claims will get dollar for dollar of new LC facility or term loan.

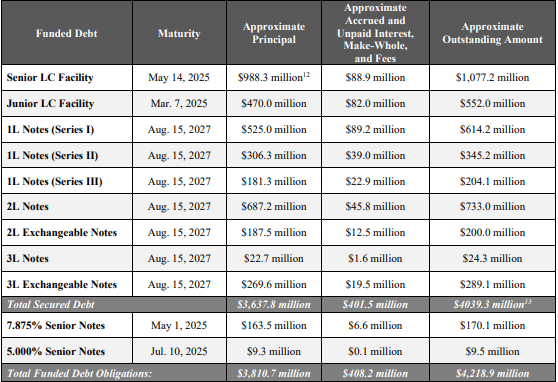

Pre-Petition Debt

docket 21 (dm.epiq11.com/case/wework/info)

Office Leases Rejected

WeWork is rejecting 61 leases under section 365(a) (docket 14 contains the list of rejected leases). New York City is the hardest hit with 35 rejected leases. I expect more leases to be rejected as the bankruptcy process continues. WeWork asserted in their Declaration that they already had negotiated lease payment reductions for 590 other leases, saving a total of $12 billion. I was shocked by this assertion given that their total future lease expense liability as of March 31, 2022 was $30.658 billion according to their 10-Q. That implies a rather dramatic percent drop in future lease payments. Some landlords seem to be willing to take a steep cut. This says a lot about the current state of affairs for office buildings in major cities – very weak.

There are many WeWork entities that are not included in the Ch.11 bankruptcy case. Many of these entities are parties to leased offices that I assume are not expected to be rejected, but that could change if they are added to the bankruptcy case. There are also many WeWork entities that are parties to leases that are included in the bankruptcy filing, but have not (yet) had their related leases rejected. (The lists can be found in docket 21 starting on page 40).

Investors in office REITs and bank stocks need to monitor this bankruptcy case because it could be the catalyst that eventually causes landlords to default on mortgages. Last month, 1440 Broadway landlord gave back the keys to the mortgage holders partially because WeWork was a major tenant.

SoftBank Will Control the New WeWork

SoftBank will control the new WeWork after it exits bankruptcy. They will own a majority of the shares, but I was unable to determine that exact amount based on the information contained in the RSA. The new board of directors will have a total of seven members – three from SoftBank, two from AHG noteholders, an independent director, and a CEO. They will have a very steep hill to climb to get WeWork operating with a positive cash flow (WeWork had a negative $646 million free cash flow for the first six months of 2023) and eventually some actual profits. I have my doubts. At least they will get rid of $3 billion debt. They are expecting to have a 4- year term loan up to $100 million.

Current Timetable

November 28 – next hearing date, February 4 – filing Ch.11 reorganization plan and disclosure statement, February 24 – motion to approve the adequacy of the disclosure statement, March 5 – order confirming the plan and effective date of the plan.

Conclusion

The reality is that current non-SoftBank WeWork shareholders are getting no recovery and their shares will be cancelled on the plan effective date, which is currently expected in March. This company was once valued at $47 billion – what a drop because their business model is not workable. There seems to be some traders who are confused and continue to buy this worthless stock. I rate WE/WEWKQ a strong sell.

Investors in office building REITs and bank stocks need to follow this bankruptcy case, especially if additional office leases are eventually rejected. The New York City office market could be really negatively impacted if there are significant additional lease rejections in the already weak Manhattan market.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

")

")

{kind=link}