Up to date March tenth, 2022 by Quinn Mohammed

Month-to-month dividend shares permit for dividend traders to compound their wealth month-to-month versus quarterly, which is the commonest dividend schedule on the planet of investing.

This frequent dividend fee permits for traders to reinvest their cash extra shortly if they’re within the asset accumulation part of their life, or to cowl dwelling bills for retirees.

You may obtain our full checklist of all 50 month-to-month dividend shares (together with necessary monetary metrics like dividend yields and payout ratios) by clicking on the hyperlink under:

Three years in the past, we appeared into Three Canadian Month-to-month Dividend Shares with Yields As much as 8%. Since then, two of these firms have been acquired. The third firm is included as soon as once more on this article.

Inter Pipeline Ltd. was absolutely acquired by Brookfield Infrastructure in late October 2021. Brookfield supplied shareholders $20.00 in money per share, or 1 / 4 of a Brookfield Infrastructure share, or any mixture of those. IPL.TO was then delisted from the TSX on November 1st, 2021.

Dream World REIT was acquired by The Blackstone Group Inc. in an all-cash transaction for $6.2 billion. Every unitholder of DRG.UN obtained $16.79 per unit.

Under are three Canadian firms buying and selling on the Toronto Inventory Alternate which have dividend yields of 5% to six% and have paid dividends each single month for a few years.

Two of the businesses under have dividend progress histories spanning over a decade, for earnings traders who rely on dividend progress along with yield.

Desk of Contents

Canadian Excessive-Yield Inventory #1: Pembina Pipeline Corp. (PBA)

Pembina Pipeline Company is a serious supplier of transportation and midstream companies. Pembina owns pipelines which transport hydrocarbon liquids and pure gasoline merchandise. Moreover, they personal gasoline gathering and processing amenities and an oil and pure gasoline liquids infrastructure and logistics enterprise. They function in Western Canada and have served their clients for greater than 65 years.

Although Pembina is a Canadian firm buying and selling below the ticker PPL on the TSX, it additionally trades on the NYSE below the ticker PBA.

The corporate owns and operates three completely different enterprise segments in western Canada. The three enterprise segments of Pembina include: Pipelines, Amenities and Advertising and marketing & New Ventures. For FY 2021, these segments made up 45%, 35%, and 20% of the corporate’s pre-tax revenue, respectively.

Supply: Investor Presentation

The corporate’s long-term technique is to accumulate and develop high-quality property that generate secure and predictable money stream, whereas delivering robust returns to shareholders.

Pembina already has a big and established backlog of progress initiatives. These initiatives lead administration to consider the company can develop adjusted money stream per share by 8%-10% per 12 months. Given Pembina’s risky earnings historical past, we anticipate they might develop adjusted money stream by about 5% per 12 months over the medium time period. Additionally, they anticipate elevating the dividend fee by 5% per 12 months going ahead.

Present Occasions

To additional gas progress, Pembina entered into an settlement with KKR to mix their western Canadian pure gasoline processing property into one single, three way partnership entity. Pembina will personal 60% of the brand new entity, and KKR’s world infrastructure fund will personal the opposite 40%. The brand new firm will even purchase Vitality Switch LP’s final 51% stake in Vitality Switch Canada (ETC). All in, the worth of those property add as much as $11.4 billion CAD.

On February twenty fourth 2022, Pembina reported their This autumn and FY 2021 outcomes. For This autumn, adjusted money stream from working actions per share rose 21% in comparison with 2020, from $1.10 CAD to $1.33. Adjusted EBITDA additionally grew 12% year-over-year to $970 million.

For the full-year 2021, the company grew adjusted money stream from working actions per share by 15%, to $4.80. Adjusted EBITDA was barely greater in comparison with 2020, a 5% improve to $3.4 billion.

With adjusted money stream per share of $4.80, and the FY 2021 dividend fee of $2.52, Pembina achieved a powerful payout ratio of 53%.

Whereas a secure and secure dividend is of utmost significance to dividend traders, firms dedicated to rising the dividend each single 12 months present much more profit. Pembina is one such firm because it has paid the next dividend for ten consecutive years, from $1.56 CAD in 2011 to $2.52 in 2021. Thus, Pembina has elevated the annual dividend by 4.9% per 12 months on common over the past decade.

Valuation & Whole Returns

Pembina Pipeline is an organization the place adjusted money stream (“ACF”) from operations are used to calculate the dividend payout ratio, and it’s one whose valuation might be based mostly on price-to-ACF. With adjusted money stream of $4.80 per share and Pembina’s present share value of $46.32 CAD, PPL.TO’s P/ACF is 9.7.

We see honest worth for Pembina at round 10.0 occasions adjusted money stream from operations. This improve in valuation might end in a 0.7% annual tailwind to complete returns.

With it’s present $2.52 CAD annual dividend, Pembina yields 5.4% (earlier than any dividend withholding taxes for non-Canadians) and pays its dividend month-to-month.

All in, we consider Pembina has the potential to generate annualized complete returns of 10.4% over the subsequent 5 years. These returns stem from a 5% progress fee, a 5.4% beginning dividend yield, and a possible valuation tailwind of 0.7% per 12 months.

Canadian Excessive-Yield Inventory #2: Alternate Revenue Company (EIFZF)

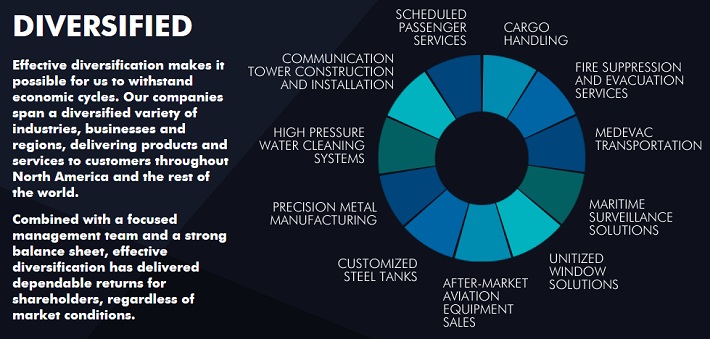

Alternate Revenue Company is a enterprise which makes investments and acquires firms within the aerospace and aviation companies and gear sector, in addition to the manufacturing sector.

The businesses acquired are in defensible area of interest markets – medevac transportation, manufacturing of aerospace and protection parts, manufacturing of a sophisticated unitized “window wall system” used primarily in high-rise multi residential developments; the checklist goes on to the tune of 15 particular person working subsidiaries.

The acquisition candidates should have a observe report of income and robust, continued money stream technology with their administration intact and a dedication to proceed constructing the enterprise.

The technique of the corporate is to develop their portfolio of diversified area of interest operations via acquisition and progress alternatives, and the results of that is to supply shareholders with a dependable and rising dividend.

Supply: Investor Relations

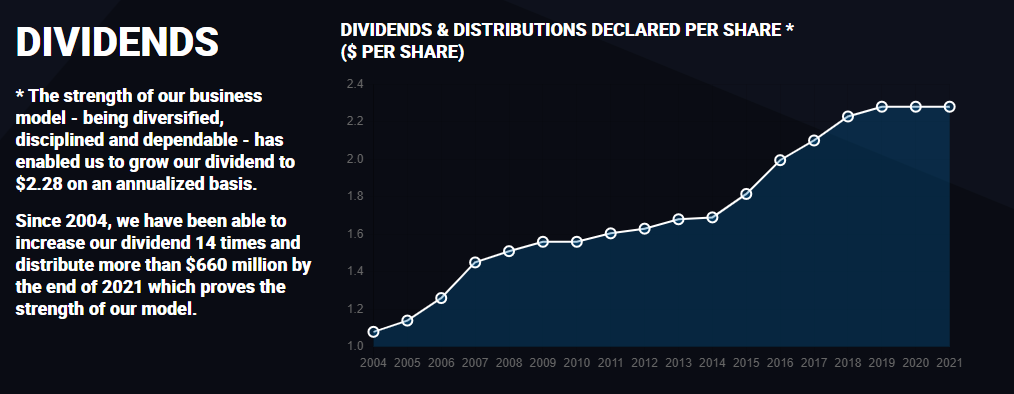

The company has elevated their dividend 14 occasions within the final 16 years (maintaining it secure via 12 months 2009 and 2021), at a 4.8% compound annual progress fee of the dividend. Whereas a close to 5% dividend progress fee is just not all that spectacular, 14 years of dividend progress bears extra weight on the TSX than it does on the NYSE. It’s because Canada has a a lot smaller checklist of dividend progress firms, or “aristocrats”.

We count on the corporate can proceed to develop their dividend by about 2.0% over the medium time period. This is able to be supported by an anticipated adjusted EPS progress fee of about 3.0% per 12 months.

Supply: Investor Relations

Present Occasions

Based on their newest quarterly launch, payout ratio when calculated as a share of free money stream much less upkeep capital expenditures improved to 58% from 71% for the trailing twelve months. Payout ratio when calculated as a share of adjusted web earnings strengthened to 99% from 169% for the trailing twelve months. As well as, the annual dividend fee value the corporate 7% greater than in FY 2020. The adjusted web earnings payout ratio signifies the dividend may very well be in danger and must be monitored.

The corporate at present pays an annual dividend of $2.28 CAD, which equates to a 5.9% yield on the present share value of $38.85 CAD. Divided on its month-to-month fee schedule, that’s a 0.49% return on funding per 30 days earlier than taking any capital appreciation into consideration.

For full-year 2021, Alternate Revenue generated report excessive income of $1.4 billion, up 23% in comparison with 2020. Adjusted web earnings improved by 82%, to $86 million. Adjusted EPS was $2.31 per share for FY 2021, a 71% improve over $1.35 in 2020.

Throughout 2021, EIFZF closed on 5 acquisitions, a brand new report for variety of acquisitions in a calendar 12 months.

Valuation & Whole Returns

We estimate the company can generate about $2.56 CAD in adjusted EPS for 2022. Thus, Alternate Revenue is buying and selling at 15.2 occasions adjusted EPS.

We see honest worth for Alternate Revenue at round 15.0 occasions adjusted EPS. This minor valuation drop might end in a (0.2%) annual headwind to complete returns.

With it’s present $2.28 CAD annual dividend, EIF.TO yields 5.9%. Mixed with our estimated 3% annual EPS progress and marginal valuation headwind, Alternate Revenue is anticipated to generate annualized complete returns of seven.8% over the subsequent 5 years.

Canadian Excessive-Yield Inventory #3: TransAlta Renewables (TRSWF)

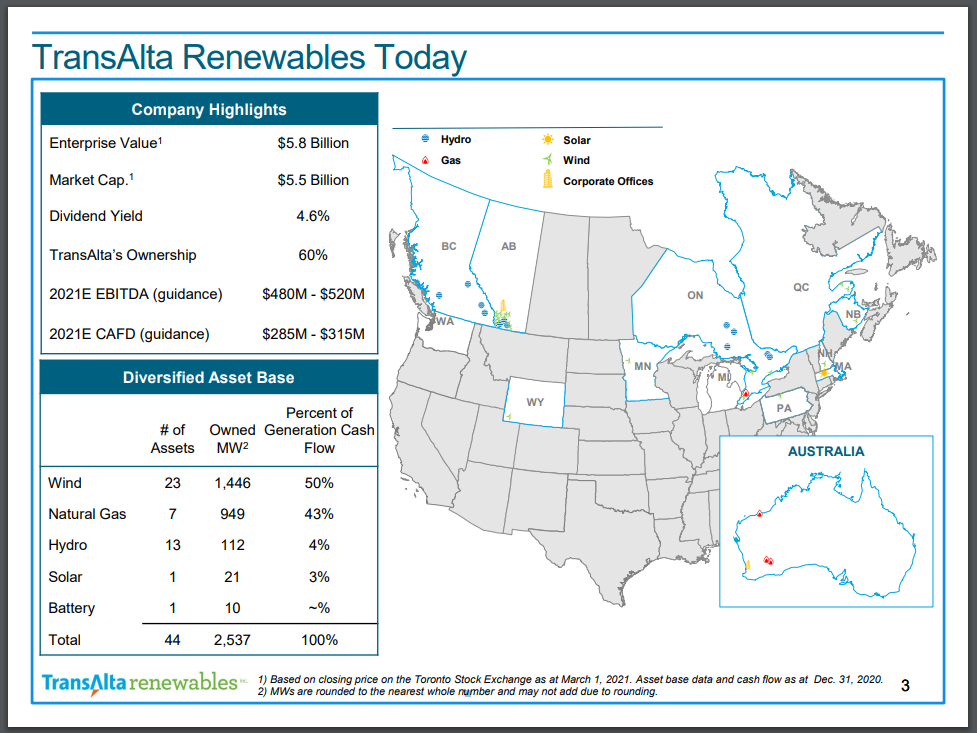

In 2013, TransAlta Renewables was spun off from TransAlta (TAC), which stays a serious shareholder within the different energy technology firm. The corporate’s historical past in renewable energy technology goes again greater than 100 years.

Its portfolio is made up of over 45 amenities powered by wind, pure gasoline, hydro, or photo voltaic, in 2022. The company generates nearly all of its money stream from its pure gasoline and wind property.

Supply: Investor Presentation

TransAlta’s portfolio is fortified by lengthy contracts, which is evidenced by its weighted common contract lifetime of greater than a decade. The corporate has remodeled $3.5 billion CAD of acquisitions since 2013 however the improve in share rely (to fund these acquisitions) has prevented its money stream per share from rising a lot, if in any respect, in sure durations.

For instance, TransAlta generated $1.34 CAD in FFO per share in 2013, and in 2021 they posted $1.34 in FCF per share, principally unchanged. From 2012 to 2021 although, its FCF per share elevated by about 1.2% per 12 months in USD.

Trying forward, we predict that progress will face a headwind from the Kent Hills 1 and a pair of wind amenities outage, as the prices of substitute and foregone income will have an effect. Presently, we estimate TransAlta Renewables can develop FCFPS by about 3% via 2027.

Present Occasions

Concerning the wind amenities outage, the corporate not too long ago suffered a tower collapse on the Kent Hills 2 wind website, and upon additional investigation, decided that each one 50 turbine foundations on the Kent Hills 1 and a pair of wind websites require a full basis substitute. This rehabilitation will take till the top of 2023 to be absolutely full. And the substitute is anticipated to value between $75 million and $100 million.

TransAlta Renewables reported fourth quarter and FY 2021 outcomes on February twenty fourth. The corporate generated barely much less renewable power manufacturing in 2021 at 4,332 GWh in comparison with 4,471 GWh in 2020. Nonetheless, revenues got here in greater by 8% over the prior 12 months, to $470 million CAD.

Yr-over-year, adjusted EBITDA was unchanged and FCF dropped 5% to $357 million CAD in comparison with $377 million. Money accessible for distribution (“CAFD”) per share, because of this, additionally decreased 10% to $1.03 CAD.

Valuation & Whole Returns

The corporate at present pays an annual dividend of $0.94 CAD (paid month-to-month at $0.07833), which equates to a 5.1% yield on the present share value of $18.57 CAD. TransAlta Renewables has maintained this dividend fee since 2017, after a sequence of dividend will increase.

We estimate the company can generate about $1.26 CAD in FCF for 2022. Thus, TransAlta Renewables is buying and selling at 14.7 occasions FCF.

We see honest worth for the company at round 13.0 occasions FCF. This potential headwind to the valuation might end in a (2.5%) annual loss to complete returns.

This valuation headwind, mixed with the 5.1% beginning dividend yield and three.0% annual progress in FCF might result in annualized complete returns of 5.1% over the subsequent 5 years.

Extra Assets

Along with these 3 high-yield Canadian shares, there are lots of different kinds of high-quality dividend shares to think about.

The next Positive Dividend databases include essentially the most dependable dividend growers in our funding universe:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

This fall 2024 Earnings Name Transcript")

{kind=link}