The Covid-19 pandemic triggered the most important financial contraction since WW2 and induced governments to enact unprecedented assist measures. Companies, specifically, benefitted from a wide selection of programmes, starting from transfers and fairness injections to publicly assured loans and debt moratoria. There may be proof that these financial measures helped stop a major spike in bankruptcies and agency closures – the variety of corporations that went bankrupt or exited the market after the pandemic is considerably smaller than in earlier years (Banerjee et al. 2021, Djankov et al. 2021, Orlando and Rodano 2022).1

A key concern is the extent to which these measures ended up additionally benefitting non-viable however nonetheless lively corporations (‘zombie corporations)’, thus altering the method of agency choice and useful resource reallocation (Leaven et al. 2020, Barnes et al. 2021, Demmou and Franco 2021). In a current paper (Pelosi et al. 2022), we assess this concern empirically, learning the take-up by zombie corporations of probably the most related assist measures enacted in Italy. As a result of the insurance policies are much like these adopted in different main superior nations, we argue our train has an inexpensive diploma of exterior validity.

In our evaluation, we deal with three fundamental measures adopted between March and Might 2020: ‘grants (i.e. transfers given to eligible corporations), debt moratoria, and public assure mortgage programmes. These measures are massive – as of March 2021 (the top of our pattern interval), corporations had acquired nearly €7 billion of transfers, about €150 billion of loans had been positioned underneath moratoria, and banks had issued about €150 billion of publicly assured loans.

Our research depends on granular administrative microdata on agency stability sheets and knowledge on their take-up of the assist measures from the Financial institution of Italy. These knowledge permit us to (1) establish zombie corporations primarily based on pre-crisis stability sheet knowledge and generally adopted standards, and (2) research the allocation of Covid-19 assist measures by agency standing, whereas accounting for the differential affect of the pandemic by agency measurement, industries and provinces.

The literature makes use of two fundamental definitions of zombie corporations. The primary leverages the curiosity protection ratio, which measures whether or not corporations’ working earnings can cowl curiosity bills (Adalet McGowan et al. 2018; Banerjee and Hoffman 2018, Andrews and Petroulakis 2019). The second leans on receiving subsidised credit score (Caballero et al. 2008, Acharya et al. 2019). We discover that the primary definition does a greater job at classifying as zombie corporations with decrease productiveness, low liquidity and capitalisation, and better default likelihood (Z-score) than the definition primarily based on subsidised credit score. Furthermore, the curiosity protection ratio-based definition has the fascinating property of figuring out debtors whose loans usually tend to be non-performing (NPL). Due to this fact, all through the evaluation, we depend on the definition of zombie corporations primarily based on corporations’ profitability.

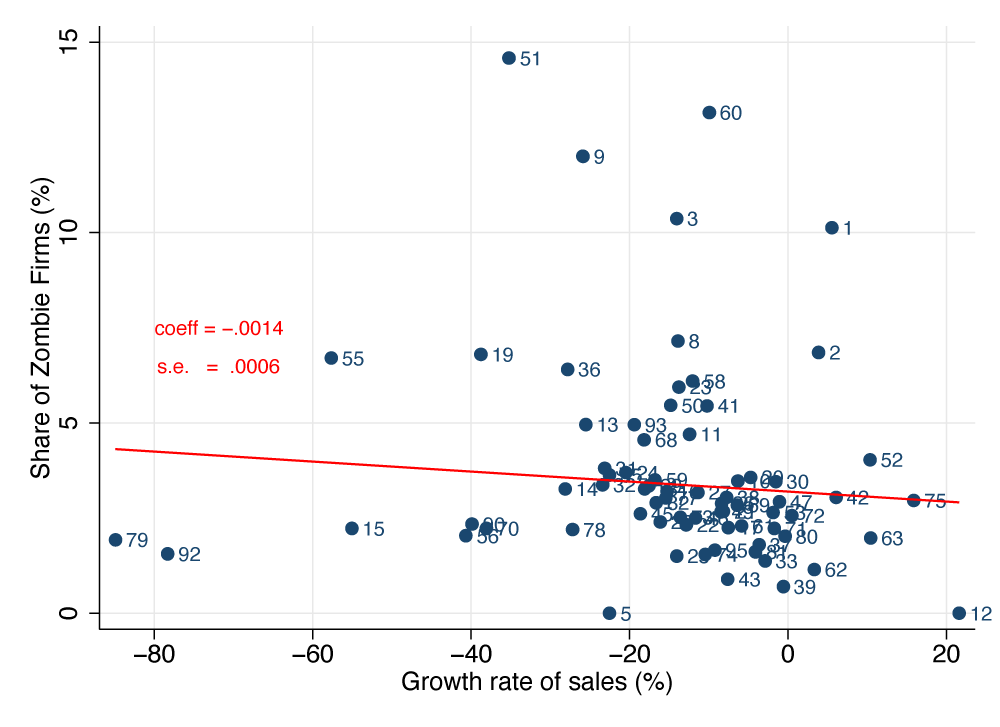

Utilizing this definition, we discover that on the finish of 2019, zombie corporations represented about 3% of all firms (11% as shares of belongings, 5.5% of worth added), and their incidence was greater in industries that skilled a bigger drop in revenues in 2020 (Determine 1). Apparently, these numbers are in the identical ballpark as these obtained by Favara et al. (2021) for the US.

Determine 1 Zombie incidence

a) Share by indicator

b) Zombie incidence and gross sales progress

Supply: Authors’ computations on knowledge from CERVED and the Italian Ministry of Economic system and Finance.

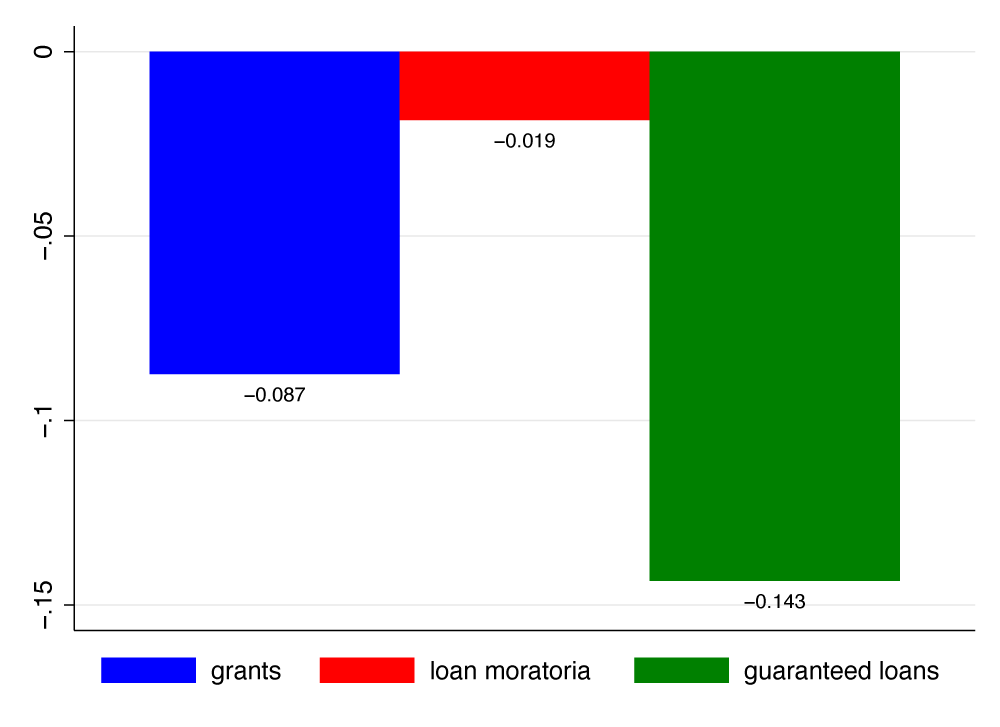

Our fundamental discovering is that zombie corporations are much less doubtless than wholesome corporations to entry public assist measures (Determine 2). Particularly, they had been 8.7% much less more likely to get hold of a grant and 1.8% much less more likely to put their debt right into a moratorium. Moreover, they had been 14% much less more likely to obtain loans assured by the federal government, and those who did acquired loans that had been on common 58% smaller than these granted to wholesome corporations. Lastly, upon accessing a assured mortgage, this was 12% extra more likely to be absolutely assured.2

Determine 2 Zombie take-up of assist measure

Supply: Our computations on knowledge from CERVED, Anacredit, Tesoreria telematica, Mediocredito centrale, and SACE.

So far as grants are involved, the decrease take-up by zombie corporations is determined by the measure’s design. Companies had been eligible for the grants if their revenues had fallen by at the least one-third between April 2019 and April 2020. Due to their structurally low stage of revenues, zombie corporations had been much less more likely to expertise a lack of such magnitude throughout the pandemic. In truth, controlling for the expansion in revenues between 2018 and 2019, we discover that the take-up of the grants is analogous for corporations that had excessive progress in revenues in 2019 however had been nonetheless zombies.

Understanding why zombie corporations had been much less more likely to entry debt moratoria and assured loans is much less simple. We present that zombie corporations’ decrease take-up of moratoria is determined by whether or not they obtained a assured mortgage. Zombie corporations that didn’t obtain a assured mortgage had been extra doubtless than wholesome corporations to make use of the moratoria. This discovering means that zombie corporations thought-about the 2 measures as substitutes.

Lastly, zombie corporations acquired fewer assured loans than wholesome corporations. Nevertheless, conditional on accessing a mortgage, zombies usually tend to obtain a full assure. Whereas zombies might have a decrease demand for credit score, their incentives to entry low cost loans to substitute current ones are plausibly excessive. On the financial institution facet, there are contrasting incentives. On the one hand, banks might desire to interchange their current loans to zombies with assured loans and switch the credit score danger onto the federal government. Then again, banks earn decrease curiosity revenue on assured loans, and substitution of current loans with assured credit score would scale back unit margins. As a result of the rate of interest differential is probably going greater for riskier than for safer corporations, this channel would incentivise banks to grant fewer assured loans to zombie corporations.3 As well as, banks may nonetheless be answerable for ‘reckless lending’ in case of default of a borrower that seemed too weak at origination. This could doubtless induce banks to lend comparatively much less to zombie corporations than to wholesome ones.

We have to acknowledge two caveats when studying our outcomes. The primary is that different measures, comparable to labour furlough schemes or freezes in chapter procedures, additionally contributed to maintaining corporations alive. Second, corporations that had been categorized as zombies earlier than the pandemic is probably not so within the post-Covid world and vice versa. Nevertheless, it’s affordable to suppose that corporations characterised by decrease productiveness and profitability and the next likelihood of default earlier than the Covid-shock – i.e. those who we establish as zombies – are more likely to even be non-viable after the shock.

Total, our proof means that zombie corporations had been much less doubtless than wholesome corporations to take up grants, mortgage moratoria, and public ensures on loans, thus suggesting that these measures didn’t contribute to a zombification of the economic system. These findings are in keeping with these accessible for France (Cros et al. 2021).

References

Acharya, V V, T Eisert, C Eufinger, and C Hirsch (2019), “No matter it takes: The actual results of unconventional financial coverage”, The Overview of Monetary Research 32(9): 3366–3411.

Andrews, D and F Petroulakis (2019), “Zombie corporations, weak banks, and depressed restructuring in Europe”, VoxEu.org, 4 April.

Adalet McGowan, M, D Andrews, and V Millot (2018), “The Strolling Lifeless? Zombie Companies and Productiveness Efficiency in OECD International locations”, Financial Coverage 33(96): 685–736.

Banerjee, R N and B Hofmann (2018), “The rise of zombie corporations: causes and penalties”, BIS Quarterly Overview, September.

Banerjee, R N, J Noss and J M V Pastor (2021), “Liquidity to solvency: transition cancelled or postponed?”, BIS Bulletin no. 40.

Barnes, S, R Hillman, G Wharf and D MacDonald (2021), “How companies are surviving Covid-19: The resilience of corporations and the position of presidency assist”, VoxEU.org, 16 July.

Bénassy-Quéré, A, B Hadjibeyli and G Roulleau (2021), “French corporations via the COVID storm: Proof from firm-level knowledge”, VoxEU.org, 27 April.

Caballero, R, T Hoshi, and A Okay Kashyap (2008), “Zombie lending and depressed restructuring in Japan”, American Financial Overview 98(5): 1943–77.

Cascarino, G, R Gallo, F Palazzo, E Sette et al. (2022), Public ensures and credit score additionality throughout the covid-19 pandemic, Technical Report, Cash and Finance Analysis group, Universita Politecnica delle Marche.

Cœuré, B (2021), “What 3.5 million French corporations can inform us concerning the effectivity of Covid-19 assist measures”, VoxEU.org, 8 September.

Cros, M, A Epaulard and P Martin (2021), “Will Schumpeter catch COVID-19? Proof from France”, VoxEU.org, 4 March.

Demmou, L and G Franco (2021), “From hibernation to reallocation: Mortgage ensures and their implications for post-Covid-19 productiveness”, VoxEU.org, 14 November

Djankov, S and E Zhang (2021), “As COVID rages, chapter circumstances fall”, VoxEU.org, 4 February.

Favara, G, C Minoiu and A Perez (2021), US zombie corporations what number of and the way consequential?, Technical Teport, Board of Governors of the Federal Reserve System.

Leaven, L, G Schepens, and I Schnabel (2020), “Zombification in Europe in occasions of pandemic”, VoxEu.org, 11 October.

Orlando, T and G Rodano (2022), “The affect of covid-19 on bankruptcies and market exits of Italian corporations”, Financial institution of Italy Covid Papers.

Pelosi, M, G Rodano, and E Sette (2022), “Zombie corporations and the take-up of assist measures throughout Covid-19”, Financial institution of Italy Occasional Paper 650.

Endnotes

1 A part of the discount in chapter procedures is because of a freeze in new filings lively till July 2020. Nevertheless, new chapter procedures are under pre-pandemic ranges even within the second half of 2020 and in 2021 (Orlando and Rodano 2022).

2 Loans smaller than €30,000 had been eligible for a 100% assure.

3 See Cascarino et al. (2022) for proof in step with this speculation.

{kind=link}