sorn340/iStock via Getty Images

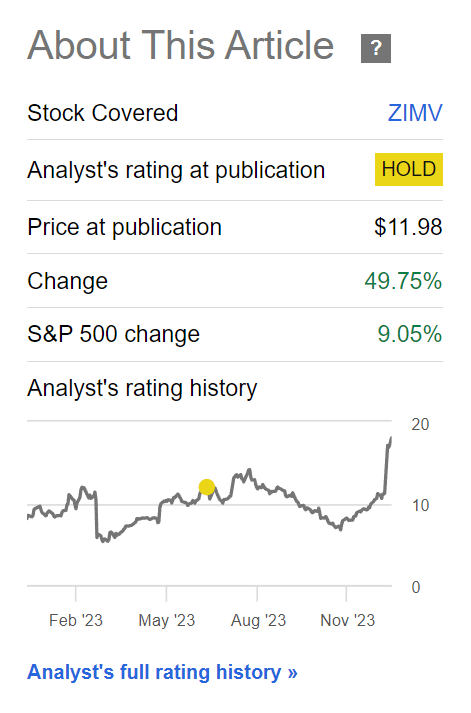

In June, I downgraded ZimVie Inc. (NASDAQ:ZIMV) to a hold, based on the company’s elevated valuation and deteriorating fundamentals. For a while, my cautious stance appeared to be the right call, as ZimVie struggled to return its businesses to growth, and the stock languished, falling to $7 a share or more than 40% below my June downgrade (Figure 1).

Figure 1 – ZIMV performance since last article (Seeking Alpha)

However, since reporting Q3 results on November 1st, ZimVie’s stock has been on a tear, more than doubling to almost $18 / share. What was the cause of this rally and what could be in store for ZimVie heading into 2024?

Brief Company Overview

First, for those not familiar, ZimVie was spun out of Zimmer Biomet (ZBH) in March 2022 and included the low-growth dental and spine medical device businesses of ZBH. Although the combined businesses generated close to $1 billion in sales, ZimVie was not a market leader in either segment and was thus deemed non-core for ZBH.

For more information on the spinoff, please refer to my initiation article.

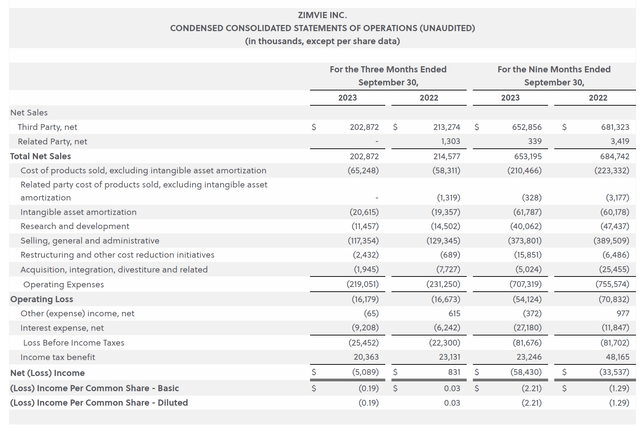

Q3 Was Better Than Feared

In early November, ZIMV reported Q3/23 earnings, with revenues declining by 5.5% YoY to $203 million. While revenues had declined YoY in every quarter in 2023, the rate of decline was better than expected, as analysts were looking for $196 million in revenues (Figure 2). For the 9 months to September 30, revenues declined by 4.6% YoY.

Figure 2 – ZIMV financial summary (ZIMV Q3/23 press release)

Despite better-than-expected revenues, ZIMV continued to show a GAAP net loss, with dil. EPS of -$0.19 / share in Q3/2023 and -$2.21 in the YTD period.

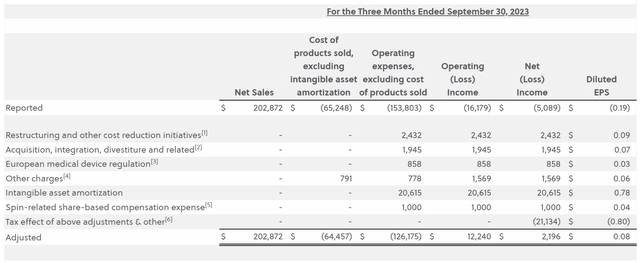

Furthermore, ZIMV continued to report heavily adjusted earnings, with quarterly adj. EPS of $0.08 compared to the -$0.19 GAAP loss. I remain critical of ZIMV’s adjusted earnings practice, as one would normally not expect so many ‘adjustments’ more than a year after the spin-off transaction (Figure 3).

Figure 3 – ZIMV reported an ‘adjusted’ net profit (ZIMV Q3/23 press release)

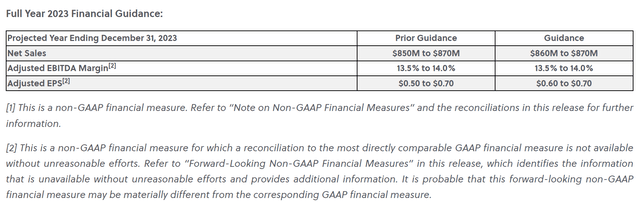

However, what likely got investors excited was the fact that management raised guidance for fiscal 2023, with slight improvements to both revenues and adj. EPS (Figure 4). The midpoint of management’s revenue guidance was raised by $5 million to $865 million while adj. EPS was raised by $0.05 to $0.65.

Figure 4 – Management raised guidance for 2023 (ZIMV Q3/23 press release)

Unfortunately, even if ZimVie hits the top end of management’s guidance and delivers $870 million in revenues and $0.70 in adj. EPS, those results would still be a YoY decline of 5% and 62% YoY respectively. Nonetheless, investors cheered the better-than-feared results and propelled the stock higher.

Divestiture Of Spine Business Lessens Debt Burden

Another key catalyst in the past few months was the announcement on December 18th that ZIMV would sell its spine business to HIG Capital for $375 million ($315 million in cash plus a $60 million promissory note that bears 10% interest).

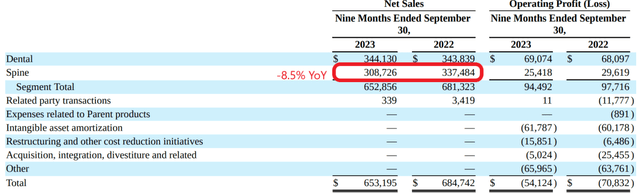

Given the spine business generated LTM revenues of $421 million and operating profits of $38.3 million (9.1% operating margin), the $375 million price tag looked like an attractive valuation for the business that was shrinking at a high-single digit (“HSD”) rate in terms of revenues so far in 2023 (Figure 5).

Figure 5 – Spine business was shrinking at HSD rate (ZIMV Q3/23 10Q report)

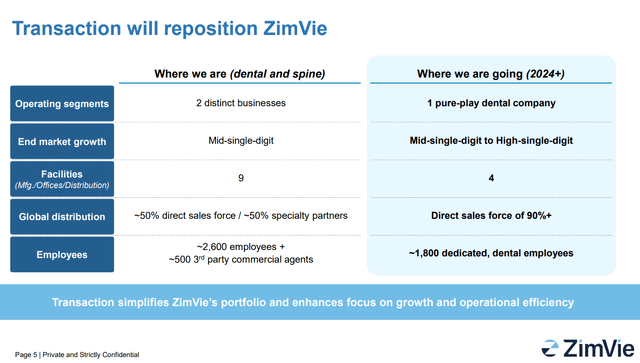

ZimVie commented that the deal proceeds would be used to pay down debt and that the deal will be accretive to revenue growth, EBITDA margin, and cash flow conversion as it allows the company to streamline operations and focus on being a pure-play dental company (Figure 6).

Figure 6 – Transaction repositions ZIMV to be a dental pure-play (ZIMV investor presentation)

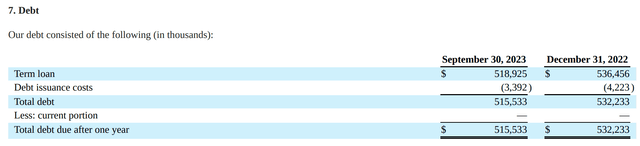

One of my biggest concerns regarding ZimVie has been the onerous debt load that Zimmer Biomet saddled the company with, with $516 million still outstanding as of September 30 (Figure 7).

Figure 7 – ZIMV had carried heavy debt load as a result of spinoff (ZIMV Q3/23 10Q report)

With the proceeds of the sale, ZimVie’s debt load is now projected to be less than $200 million going forward.

So ZimVie was able to solve one of the company’s biggest challenges by jettisoning the underperforming spine business for top dollar to a private equity group. Little wonder that ZIMV’s stock rallied more than 40% on the deal announcement. Kudos to ZIMV’s CEO for a fantastic transaction.

Standalone Dental Business Looks Attractively Valued

As a standalone business, ZimVie’s dental business generated $460 million in revenues in 2022 with $94 million in operating profit (Figure 8).

Figure 8 – 2022 segment revenue and operating profits (ZIMV 2022 10K report)

These operating metrics should be fairly consistent on a go-forward basis, as top-line growth rates have hovered around flat in 2023 for the dental segment (from Figure 5 above).

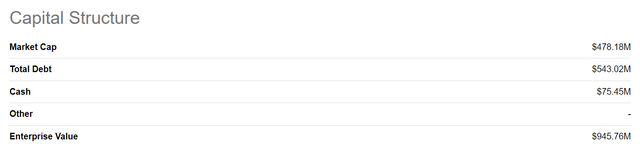

Therefore, assuming the full $375 million is applied against debt, ZIMV should have a pro-forma enterprise value (“EV”) of ~$570 million or, a valuation of 6x EV / operating profit (Figure 9).

Figure 9 – ZIMV enterprise value (Seeking Alpha)

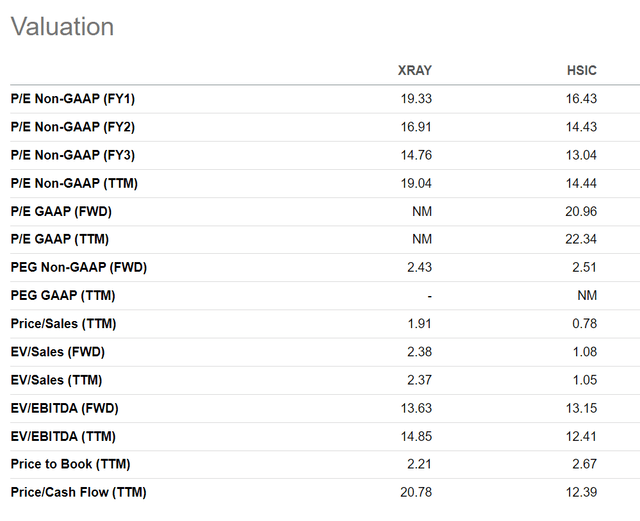

This compares well to dental market leaders DENTSPLY (XRAY) and Henry Schein (HSIC), which trade at the Fwd EV/EBITDA of 13.6x and 13.2x respectively (caveat being ZIMV’s definition of operating profits and EBITDA may not be the same).

Figure 10 – ZIMV attractively valued relative to dental market leaders (Seeking Alpha)

If management can now turn its focus on the dental business and return it to growth, then there should be significant valuation upside to ZIMV’s shares.

Conclusion

In conclusion, I believe the market’s positive reaction to ZIMV’s deal to sell its spine business is justified, as the company was able to jettison a shrinking spine business for top dollar while resolving the debt overhang that had been plaguing the company.

Looking forward, the standalone dental business now looks cheap compared to peers, trading at just ~6x EV / operating profits. If management can return the dental business to top and bottom-line growth, I believe there is significant upside in ZIMV’s shares, as dental market leaders are trading at >13x Fwd EV/EBITDA. I am raising my rating on ZIMV to a buy.

")

")

")

{kind=link}