Water cannot leave our planet and it does not arrive from space. The amount of water available on earth always stays the same, it’s the availability of water that changes. In Bangladesh, small villages use packs of pills distributed by NGOs to purify pond water and make it drinkable. In Pacific Island countries, expensive desalination plants transform sea water into fresh water. Ultimately, we can imagine a future where water can be extracted from anywhere in an economical fashion. Until then, investing in water infrastructure seems like a compelling growth thesis.

Desalination is an attractive investment thesis, but there aren’t many pure-play desalination stocks out there. In fact, there aren’t many good ways to invest in water, period. That’s why Xylem (XYL) stood out when we last covered them in a piece titled Investing in Smart Water Technology with Xylem.

Revisiting Xylem Stock

Xylem has been spending big bucks over the years to solidify its place in smart water technology while offering retail investors some interesting exposure to water scarcity and the Internet of Things (IoT). That’s the conclusion we reached three years ago, and today we’re able to buy shares at around a 12% premium to what they were priced at the time we wrote our last piece in October 2019. In the meantime, Xylem’s revenues haven’t changed much which means we’re paying around the same valuation – a simple valuation ratio of three compared to our catalog average of eight. This brings up questions around whether Xylem is priced for growth.

Our interest in equities surrounds two different strategies:

- Disruptive growth stocks capturing market share to maintain leadership in their niche

- Dividend growth stocks – growth or value

Disruptive growth isn’t about companies that are planning to plan or offering a “build it and they will come” value proposition. Disruptive tech stocks are different even from growth stocks, something that demands we define what a growth stock is in the first place.

Growth Investing vs Value Investing

Two of the oldest stock classifications in finance – growth and value – are not mutually exclusive categories. The terms are somewhat self-explanatory but defined differently by everyone. What we can all probably agree on is that generally speaking, growth stocks outperform in bull markets while value stocks outperform in bear markets. However, we need a more objective way to quantify these classifications because everyone defines them differently.

Leading global index provider MSCI (MSCI) provides an objective way to classify stocks according to value or growth exposure.

Note that these two categories are not mutually exclusive. When MSCI builds value and growth indices, they merely weigh a stock according to its exposure. For example, a firm might have 40% exposure in the value index and 60% in the growth index (the total exposure always sums to 100%).

It’s intuitive that technology stocks are typically growth stocks. That’s because technology is often what enables disruption to happen, and companies that disrupt generate lots of revenue growth. In fact, revenue growth is the most important metric we watch for in disruptive tech stocks alongside their ability to survive in today’s bear market.

That brings us to Xylem, a stock that may fit the traditional definition of growth, but may not clear the bar when it comes to the disruptive revenue growth we’re looking for.

Xylem Stock: Value vs. Growth

Thinking about an investment in Xylem demands we take a step back and recall what we’re looking for in a stock that might belong in our disruptive tech stock portfolio. There needs to be an element of disruption, that is, technology being used to create a new blue ocean opportunity or displace existing market share. Proof that said technology has traction can be seen in the form of revenue growth. A disruptive technology company without revenue growth is pointless. That’s why one of the only two reasons we’ll sell a disruptive tech stock is if revenue growth stalls or our thesis changes.

Xylem doesn’t offer the revenue growth we’re looking for.

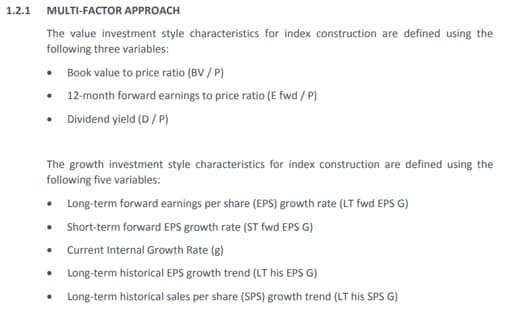

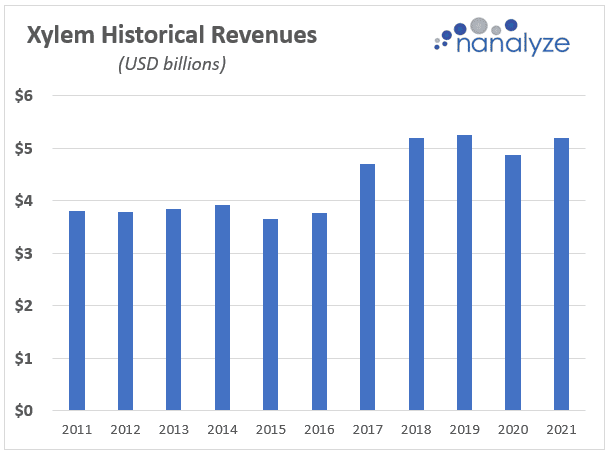

Over the past decade, they’ve grown revenues at a compound annual growth rate of 3.2% – about what global inflation averaged during 2020. Like a utility company, Xylem is growing slowly and making sure to reward investors along the way with dividends and share buybacks. Around 38% of Xylem’s capital deployment over the last three years has been value returned to shareholders in the form of dividends or share repurchases.

It’s traditionally frowned upon for growth companies to pay dividends because that money can see a much better return by reinvesting it in the company instead of giving it back to investors. Sometimes, we’ll see foreign growth companies pay dividends which may relate to cultural expectations from investors, but we largely expect to see growth companies using the cash they generate to keep growing. Xylem’s messaging doesn’t lead us to believe they’ll be transforming into a growth machine anytime soon.

What Xylem Says

Traditional growth factors look at earnings growth. Looking back at the MSCI objective criteria, four out of five relate to earnings per share. Therefore, Xylem’s ability to be perceived as a traditional growth company relies on their ability to grow earnings, something that can only happen two ways – by growing revenues or expanding margins. Messaging from the company surrounds margin expansion and an increase in digital offerings which also helps expand margins. Milestones out to 2025 include organic compound annual revenue growth of 5-6% (from 2021 to 2025) which is historically the sort of growth numbers we’ve seen from the company over the past 12 years.

What we don’t see is messaging around how strong revenue growth will be realized as they look to disrupt aging global water infrastructure. It may be a great way to invest in water scarcity, but it doesn’t clear the bar when it comes to the sort of disruptive growth we want to see in our own tech stock portfolio.

Conclusion

Water represents a compelling investment thesis. Aging water infrastructure lends itself to technological improvements brought about by IoT technology solutions such as those being offered by Xylem. Unfortunately, they’re a mature company that’s moving forward with a prudent plan to expand margins and revenues to a lesser extent. A company with a track record of low single-digit revenue growth isn’t a bad investment, it’s just not something that belongs in our disruptive tech stock portfolio.

Tech investing is extremely risky. Minimize your risk with our stock research, investment tools, and portfolios, and find out which tech stocks you should avoid. Become a Nanalyze Premium member and find out today!

{kind=link}