U.S. respondents solely

Noting that the industrial actual property trade has reached “an inflection level” and issues are lastly trying up, the City Land Institute and PwC have launched their Rising Tendencies for Actual Property 2025 forecast for the U.S. and Canada. As typical, the annual report additionally identifies the highest cities to observe.

The rising developments and rising metros are based mostly on 450 interviews and 1,600 survey outcomes from a broad swath of economic actual property professionals, who, the report cautioned, are nonetheless not “wildly optimistic.”

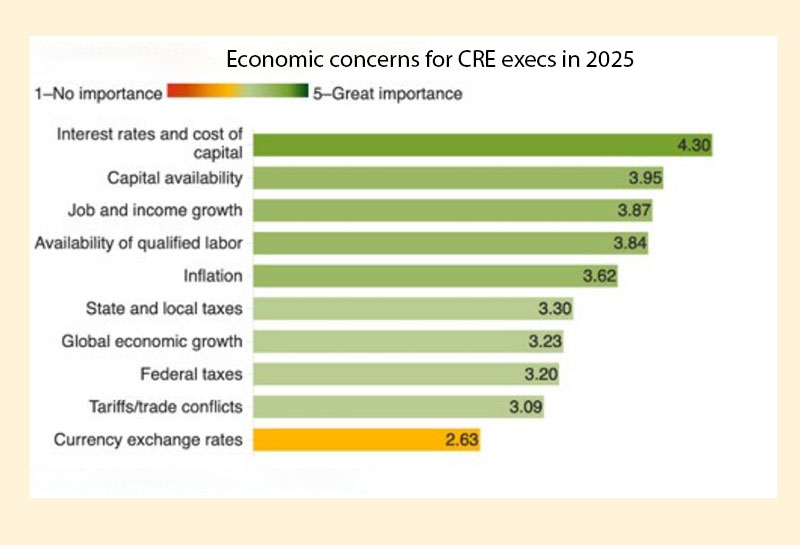

Rates of interest and value of capital are nonetheless the highest financial concern for interviewees and respondents, the majority of that are within the enterprise of shopping for and promoting actual property. Non-public property homeowners or industrial/multifamily builders symbolize 35.2 p.c of the executives ULI and PwC drew their conclusions from, and actual property advisory, asset administration or service firms comprise 20.1 p.c. The following two best financial issues had been capital availability and job and revenue progress.

READ ALSO: What Occurred to the Capital Markets

However capital prices fell barely in significance over final 12 months (down 40 foundation factors to 4.30 on a scale of 1 to five), reflecting the Fed’s August announcement that it was prepared to begin dropping charges. The precise 50-basis-point minimize got here after many of the survey members responded.

The three greatest social/political issues for the respondents and interviewees for 2025 are housing adopted by political extremism and immigration coverage—similar as final 12 months, though immigration beat out political extremism final 12 months.

The highest issues for builders in 2025 are building prices, labor availability and working prices.

Rising Tendencies for 2025

1. Be Cautious What You Want For

The Fed has begun making long-awaited rate of interest cuts and respondents count on elevated financial certainty to spice up transaction quantity and even some growth. However CRE executives are additionally cautious of how slower financial and job progress (i.e., the Fed’s delicate touchdown) may influence demand, NOI and worth appreciation. In sum, there may be “a combined outlook” for industrial actual property.

2. New Cycle Begins

“Therapeutic” within the capital markets is starting to allow the value discovery that has eluded the market for the reason that Fed started mountaineering rates of interest in March of 2022. There’s ample capital—at a barely extra affordable worth—for acquisitions and refinancing. As traders scale back their “publicity,” they are going to be extra prepared to tackle “new publicity.” On the fairness facet, there’s a rising consensus that costs have troughed.

3. Constructing Increase, Tenant Boon

Demand for many property sorts is stronger than pre-pandemic ranges, respondents reported. In workplace, nonetheless, there’s a “painful reckoning” of a seemingly extra everlasting nature. Oversupply in quite a few property sorts has created a real tenant’s market. Nevertheless, the report finds a widening bifurcation between newly constructed prime workplace and industrial areas and older areas with fewer facilities. Tenants’ benefit can be lessened as soon as the event pipeline slows down. In multifamily, oversupply has led to falling rents, notably within the Solar Belt. However demand is anticipated to soak up provide.

4. Now The place?

The report finds that Solar Belt migration has moderated because the area’s price benefit is evaporating in lots of areas and relocation prices (shifting bills and better rates of interest) improve. Local weather change can be an even bigger consider strikes in coming years, and will additionally contribute to a slowing of Solar Belt migration since most of the catastrophic climate occasions happen in that area.

5. Many Options, No Solutions

Whereas most new housing manufacturing tends to be market-rate or luxurious attributable to excessive building prices, there’s a sense that housing of any kind is welcome and that lower-income residents will be capable to occupy models vacated by the residents who transfer to newer buildings in a course of known as “filtering.” A federal answer to the housing disaster is required, and each presidential candidates are promising to deal with the issue throughout their potential administrations.

With CRE executives preparing for the following upcycle, the second set of developments is property-focused. Respondents rated the core property sorts on a scale of 1 to five, with industrial rating highest and workplace rating lowest for funding. Single-family housing ranked highest and workplace ranked lowest for growth.

Key developments for property sorts

1. Industrial Good Development

Industrial tenants can be fastidiously curating their logistics portfolios, specializing in provide chain effectivity, community diversification, know-how and sustainability. Savvy homeowners and builders can be tailoring their product to cater to tenants’ extra refined urge for food for house. Nearshoring and onshoring will drive manufacturing progress.

2. Information Facilities: Navigating Energy Constraints and Skyrocketing Demand

The info middle enterprise is exploding, and CRE traders are clamoring to fulfill demand. “Growth is extremely worthwhile in comparison with different types of actual property and lengthy leases with credit score tenants help excessive loan-to-value ratios,” the report authors wrote. Tenants’ intense energy necessities at present make growth difficult, however that’s stopping the market from getting oversupplied and holding rents excessive, the report discovered.

3. Senior Housing: Constructing New Muscle

As capital for brand spanking new senior housing turns into accessible, the report recommends rethinking the standard senior dwelling fashions to supply extra alternate options for getting older child boomers—now 20 p.c of the inhabitants and rising—and for “middle-market” seniors particularly.

4. Retail Resilience: Weathering the Storm

Demand for bodily retail has rebounded whereas there was little or no building over the previous few years, the report notes. Because of this, retail vacancies are down, and rents are up. Numerous retail bankruptcies and closures in 2024 appeared to threaten retail’s profitable streak, however landlords have been capable of backfill the house. Eating places, experiential retail and “quasi-medical” tenants are all increasing. Drug retailer closures are a priority, however additionally they current a redevelopment alternative.

5. Innovating the Suburbs: Is Life Sciences’ Development

Sustainable

Life science continues to develop, although perhaps not as quick as its actual property provide. In keeping with the report, the life science stock expanded by 20 p.c for the reason that begin of COVID-19, however absorption has not saved tempo in lots of markets. There are indications a brand new progress spurt for biotech is getting underway, igniting hope that new inventories will quickly be absorbed.

As soon as once more, the highest 10 rising markets for 2025 are largely within the Solar Belt area. This 12 months, they embody Dallas/Ft. Value; Miami; Houston; Tampa-St. Petersburg, Fla.; Nashville, Tenn.; Manhattan; Detroit; Columbus, Ohio; Charleston, S.C.; and New Orleans.

In 2024, the highest rising markets had been: Nashville; Phoenix; Dallas/Fort Value; Atlanta; Austin, Texas; San Diego; Boston; San Antonio; Raleigh/Durham, N.C.; Seattle; Houston; Denver and Charlotte, N.C.

{kind=link}