Sundry Photography

Introduction

Uber (NYSE:UBER) remains one of our favorite stocks to trade, and research, as we continue to roll through a busy technology earnings season. Given the improving profitability of Uber, valuing the stock becomes easier, as we believe the stock has much more upside despite what has been a difficult IPO environment. The company generated lackluster returns since going public ($41 IPO price) as the stock currently trades at $34. Some of the weakness following IPO owed to an absence of profitability historically, negative news items relating to the company and how it manages its business, on-going headwinds in the form of foreign exchange.

We expect +80% upside based on our $62 price target. The company has grown a lot since it first went public in 2019, and yet it still trades at a discount to its IPO price of $42. We believe the stock trades at a steep discount to future growth given the overall uncertainty of achieving profitability, and difficult growth comparisons to other companies.

UBER has a lot of room for appreciation based on our upside estimate. We give UBER a buy recommendation to our readers, as we value the stock at 15x FY ‘25 earnings, which is extremely cheap (even in this environment), and even cheaper when compared to our research on Alphabet (GOOG) (GOOGL) and Advanced Micro Devices (AMD), which we value both at 18x forward FY ‘25 earnings.

Uber Q4 ’22 Earnings summary

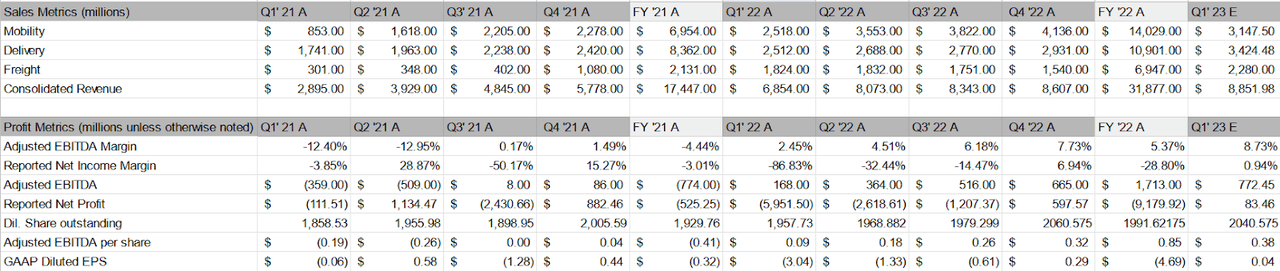

Uber surprised us this quarter with solid earnings, and execution. Uber reported diluted earnings per share of $0.29 versus $-0.18 loss (consensus), according to Refinitiv. Revenue also delivered above expectations, as Uber reported revenue of $8.6 billion vs. $8.49 billion (consensus). We also found the +90% y/y growth in FY ‘22 sales ($31.877 billion) versus FY ‘21 sales ($17.455 billion) reassuring on a constant currency basis. We don’t understand why some other analysts are forecasting such a steep drop-off on revenue growth aside from management outlook suggesting a lower growth range for bookings. We find ourselves modeling growth that’s more consistent with historical trends, as management didn’t offer a full-year revenue outlook range, but did offer Q1 ‘23 growth outlook in the mid-20% range for bookings, which was fairly underwhelming.

Arguably, Uber has one of the strongest growth narratives among tech stocks coming out of this week, though we feel like Lyft’s (LYFT) poor results and guidance stole the show with the stock tanking -30% in the afterhours on February 9th, Thursday afterhours session. LYFT then consequently opened Friday morning at $11 and is trading at $10.50 (dropping an additional -5%) at the time of writing as of February 10th, 2022.

Even with the impressive results UBER managed to deliver, we think investors are dodging the rideshare oligopoly as a whole. We like Uber as an investment much more given the bias towards being long the market when building a portfolio, and because the growth drivers to Uber via rideshare, delivery, and logistics have a multi-year growth runway that imply substantial upside assuming Uber trades at a more normalized valuation range.

Also, we anticipate more upside tied to advertising related revenue, which is high margin revenue that seems incremental to the delivery side, or Uber Eats app, which Dara Khosrowshahi anticipates will become a $1 billion business by 2024:

We committed to $1 billion in revenue by 2024, and we are progressing very, very well against that target. So you should expect to see more upside, both, by the way, in our Delivery business, but also in our Mobility business, we’ve seen some really encouraging signal as it relates to Journey Ads on Mobility, which you see on the app, put through rates over 3%, CPMs of $45, which is pretty amazing.

We think UBER is a cheap growth stock and operates a quality business model in the rideshare segment, and space. We anticipate efforts to further expand its business ecosystem, and the inclusion of more features tied to rideshare, and basic logistics inclusive of rental car services among many other announced products and services to add meaningfully to the stock and valuation.

We estimate that Uber will report Q1 ‘23 revenue of $8.85 billion, and diluted EPS of $0.05 per share, which compares to consensus estimates of $8.7 billion, and diluted EPS of -$.09. We think Uber sustains profitability, but based on management commentary we’re just not certain how the timing of non-cash charges, and cost-efficiency programs start to normalize into a quarterly trend of low profit margins to high single digit profit margins. Given the gradual improvement in adjusted EBITDA over the past year, we think profit transition is the main argument going in favor of Uber currently, especially when compared to Lyft.

Investment thesis overview

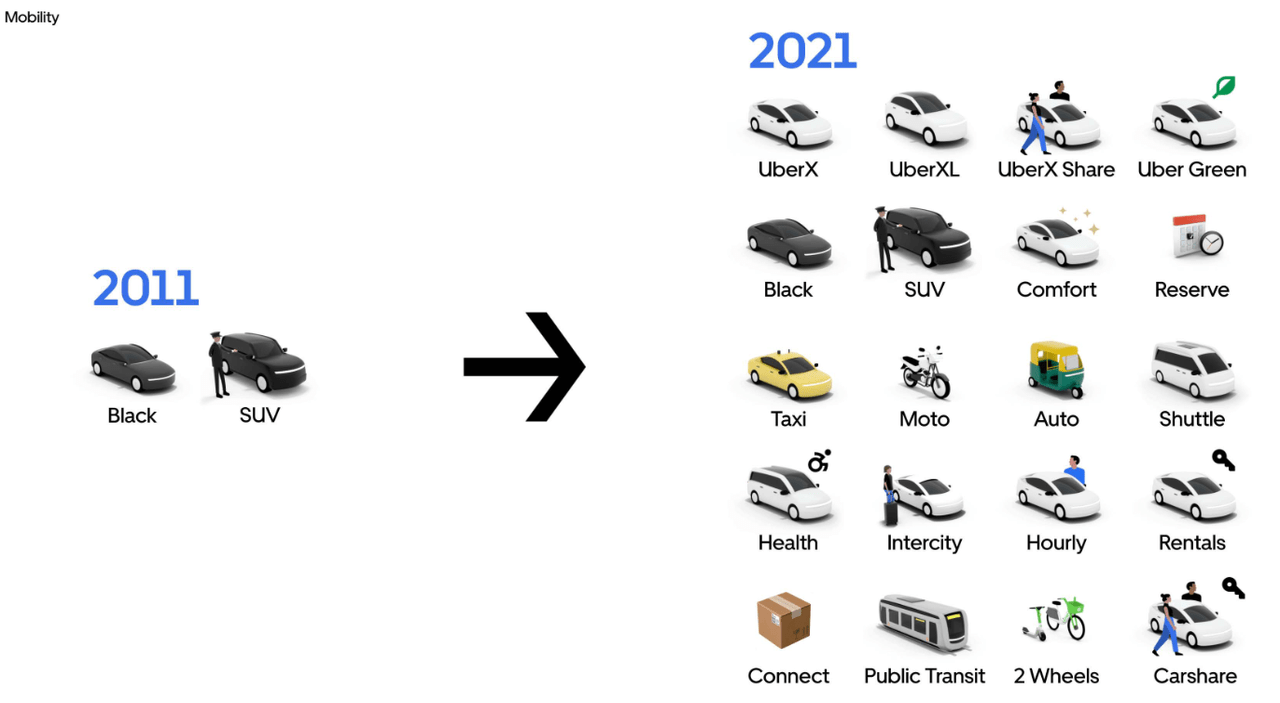

Figure 1. Uber continues to expand from 2011 to 2021

Uber Investor Day 2022 Presentation (Uber)

UBER thesis: 1) Strength in core ridership metrics and growth in monthly active platform users from 118 million in FY ‘21 to 131 million FY ‘22, keeps us on board the ride share app. 2) Uber Eats continues to show strength (delivery bookings grew 14%-15% in the United States and globally) the business also turned profitable in Q4 ‘22 3) Uber’s growth in freight and logistics positions it in front of a massive transportation opportunity, which we anticipate will grow to $10 billion + or more sales by FY ‘24. 4) Transition towards GAAP profitability makes the business easier to understand and easier to value by end of 2023. 5) Transition towards profitability aided by an internal advertising business unit tied to Uber Eats, which gives restaurants and various private businesses an opportunity to drive traffic towards their business, while giving UBER an incremental $1 billion revenue source for FY ‘24.

We like Uber exiting Q4 ‘22 earnings, and we anticipate that the company will report earnings and revenue results that deliver above consensus expectations as we progress through the year. We also appreciate the commentary tied to cost reductions while Uber continues to sustain a high sales growth rate of 25%+ (maybe more) over the course of FY ‘23.

We think freight transportation is also a highly underrated opportunity, we expect greater revenue contribution tied to semi-trucks. Upon reviewing the technology demo, and the prospects for earning money by distributing cargo in the freight ecosystem, we expect more adoption from commercial truck drivers. We expect Uber Freight to contribute the most meaningfully to the growth thesis as core rideshare, and delivery starts to slow in growth by 2025.

Financial model overview

We expect mobility, and delivery revenue to grow at a fast rate, as we forecast revenue of $8.85 billion in Q1 ‘23, which is driven by annualized, and sequential growth trends in both businesses. We expect adjusted EBITDA metrics to rapidly improve in-line with historical trends of +100 bps growth per quarter since Q3 ‘21.

Management commentary from the Q4 ‘22 earnings call is supportive of continued adjusted EBITDA margin growth. Cost adjustments and charge offs tied to various acquisitions and minority interest: Joby (valued at $100 million), Aurora (valued at $400 million), Grab (valued at $1.7 billion), and Didi (valued at $1.8 billion). Other minority interests equate to $1.2 billion, which totals to about $5.2 billion in non-cash impact tied to just equity ownership (financial value moves on a mark to market basis). Meaning that about $5.2 billion in equity value moves the bottom line figure based on the perceived market value of those assets, and are non-financial charges, which is why we rely on the adjusted EBITDA figure to understand the core business profits.

Uber GAAP earnings per share figures gets affected by other non-cash charge offs like the recent $2.65 billion Post Mates M&A back in 2020 also having a negative impact due to amortization related charges being spread over a number of years. Post Mates no longer exists, and was mainly used to absorb customers into Uber’s existing Uber Eats app. We anticipate that the growth tied to the one-off M&A starts to moderate a little, which is why estimates on delivery might be a bit too high. We model a more conservative growth rate of +36% growth rate ahead of Q1 ’23 earnings. Though we believe UBER’s absolute market dominance in the segment translates to high revenue growth over the next three-year period regardless.

Figure 2. UBER Historical to Next Quarter Comparisons

Uber Historical Financials company data (Trade Theory)

We’re more optimistic than other analysts on revenue, but we think it’s justifiable given the improving growth narrative tied to delivery and freight. Profits also become more achievable, as the numbers tied to delivery start to factor favorably following adjustment charge-offs, and efforts to focus on core businesses translates to a much bigger business operating at much larger scale thus driving economies of scale, which is why we forecast revenue of $45 billion in FY ‘23 and $2 billion GAAP net profit on extremely low profit margins of 4.21%, which we think is achievable and below the 7% target mentioned by management assuming M&A related charge-offs are more limited going forward.

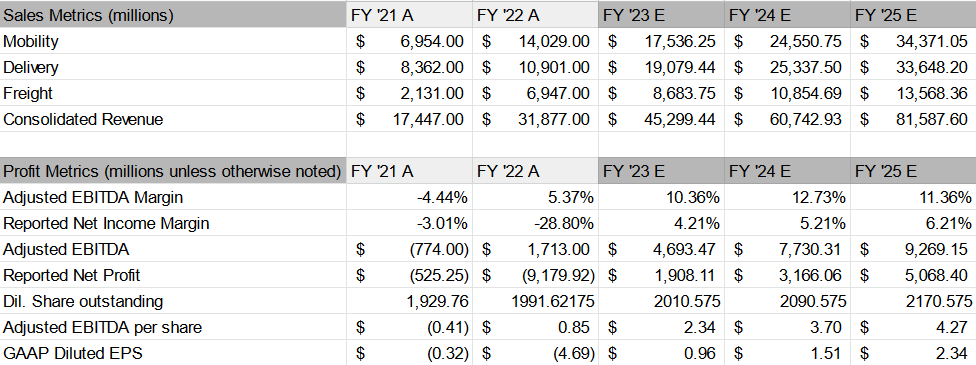

Figure 3. UBER Multi-Year Financial Model 2023-2025

Uber Multi-Year Financial Model (Trade Theory)

We expect revenue to more than double over the next three years as we expect FY ‘22 revenue of $31 billion to reach $81 billion by FY ‘25, which is quite astonishing given the already impressive scale of UBER. Given the broadness of growth, expansion of mobile product portfolio we find ourselves liking the stock on revenue/profit ramp.

We expect UBER to improve its profitability to 4.21% in FY ‘23 and then estimate profits grow to a 6%-7% level by FY ‘25, which seems very conservative and doable given the contribution of higher priced, higher margin contributing categories, and efficiencies driving up the overall profitability of UBER.

We think the mobility business slows in growth over time, but expect maturity in the business to also translate to e-commerce like profits, and so we value the business more conservatively, because its volume driven, gross market volume type model probably leads to an eBay (EBAY) like valuation of 16x earnings (historical range), which is already captured in our estimate. It’s also why we value the stock at a lower multiple than some technology conglomerates like AAPL and AMD at 18x earnings.

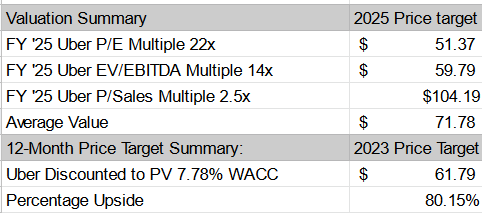

Figure 4. Valuation Model 12-month forecast

Uber Financial Model (Trade Theory)

Given the sensitivity to multiples and also low profit margins, we try our best to arrive at a fair value estimate, which by all definitions seems very conservative given our inputs. We value the business in FY ‘25 terms at 22x P/E, 14x EV/EBITDA, and 2.5x Sales. We then discount the average value of $72 by 7.78% or the firm’s WACC to arrive at our 12-month $62 price target on the stock, which implies +80% upside from where the stock is currently trading at $34 per share (at the time of writing).

Is Uber worth adding to the investor’s portfolio?

UBER had a phenomenal Q4 ‘22, the improving profit ramp, and the differentiated opportunities in mobility, delivery, and freight makes us more excited about the future of the company. We also think the stock and sector are heavily undervalued in general, but given the more immediacy of the quickly maturing, and better positioned UBER versus LYFT narrative, we have to recommend UBER as a stock to our readers given the ramping adjusted EBITDA margins to low 10%-11% range by FY ‘25, i.e. the underlying business is becoming more profitable even if cost adjustments tied to M&A and minority equity masks the impact on margins near-term.

We think the business narrative has improved to a point where we can anticipate profits on a sustainable basis, as opposed to a temporary or on an accounting basis due to gimmicky accounting adjustments. Furthermore, we think we can value the stock given the improving profit narrative, though investors might not be as responsive to this area given the overwhelming impact of M&A related charges. However, if we can look past the historical negatives tied to UBER, we can conservatively value the stock using very conservative inputs, and arrive at a discounted valuation of $62 using e-commerce-like multiples, which is extremely conservative and mirrors AMZN with a large and rapidly growing revenue base at low margins.

We acknowledge that there could be risks to our thesis, as Uber has historically performed poorly on profit metrics, and has gone on a business buying spree over the past three years. We’re hopeful those activities diminish, as the company orients towards organic growth, and meets a combination of revenue and profit expectations set by analysts on less corporate M&A activity.

We think the internal growth initiatives paired with the underlying growth in rideshare fundamentals keeps us long-term bulls in the name. We like the stock overall despite the gradual profit transition. We recommend UBER to our readers by offering our buy recommendation on the stock and expect +80% upside from where the stock is trading.

")

{kind=link}