Published on March 28th, 2023 by Nikolaos Sismanis

Monthly dividend stocks can be a fruitful investment option for individuals seeking stable income because they provide a predictable and consistent stream of cash flow. Unlike quarterly or annual dividends, monthly dividends allow investors to receive more frequent payments, which can help to cover living expenses or supplement other sources of income. Monthly dividend stocks can also be great for compounding returns, as investors can reinvest the dividends received to grow their wealth over time. Generally speaking, monthly dividend stocks can also help to offset market volatility and support their long-term financial goals.

There are just 86 companies that currently offer a monthly dividend payment. You can see all 86 monthly dividend paying names here.

You can download our full Excel spreadsheet of all monthly dividend stocks (along with metrics that matter, like dividend yield and payout ratio) by clicking on the link below:

However, not all monthly dividend stocks are created equal, and the safety of a dividend-paying stock is not solely determined by the frequency of its payouts. In fact, there are lots of examples of monthly dividend companies, which in their pursuit to attract investors through monthly payouts, have ended up overdistributing dividends. Consequently, several monthly dividend stocks have had to reduce their dividend payments when their profits take an unforeseen hit. Overall, despite the positive attributes attached to monthly dividend stocks, their risk profile can be elevated as they strive to maintain their frequent payouts.

That’s why, in this article, we have cherry-picked the ten monthly dividend stocks from our Sure Analysis Research Database, which we believe rank best in terms of dividend safety based on our Dividend Risk Score rating system. The stocks have been arranged in ascending order based on their Dividend Risk scores, and if there is a tie, their ranking is determined by their payout ratio, with the lowest payout ratio earning a higher place.

Table of Contents

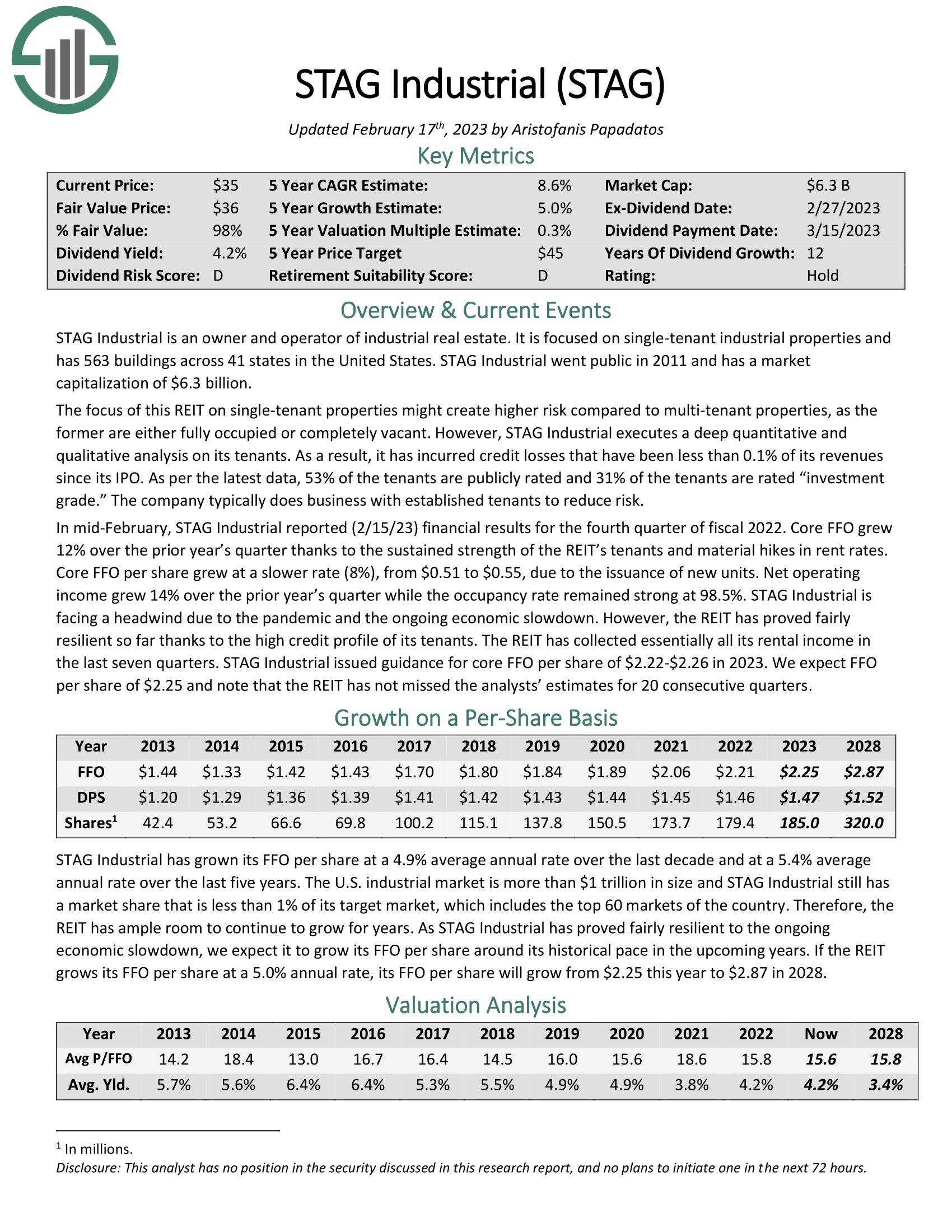

Monthly Dividend Stock #10: STAG Industrial, Inc. (STAG)

- Dividend Risk Score: D

- Dividend Yield: 4.5%

- Payout Ratio: 65%

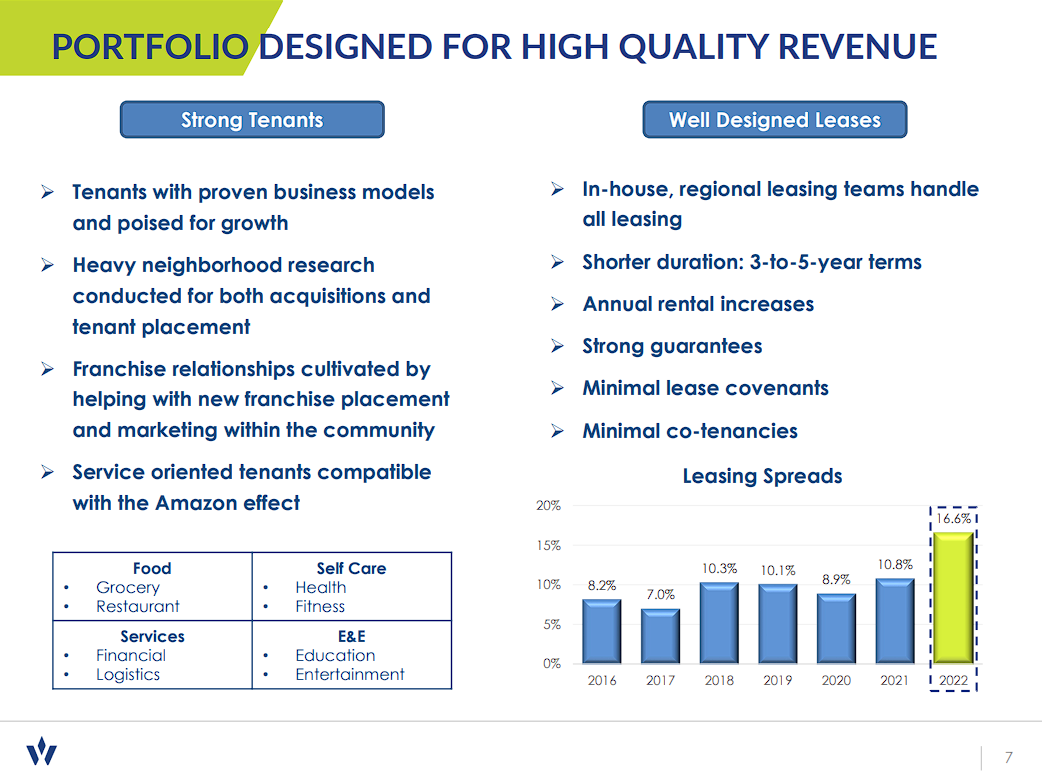

STAG Industrial is a Real Estate Investment Trust, or REIT. It is an owner and operator of industrial real estate. It is focused on single-tenant industrial properties and has 562 buildings across 40 states in the United States.

The focus of this REIT on single-tenant properties might create higher risk compared to multi-tenant properties, as the former are either fully occupied or completely vacant. However, STAG Industrial executes a deep quantitative and qualitative analysis of its tenants. As a result, it has incurred credit losses that have been less than 0.1% of its revenues since its IPO. As per the latest data, 52% of the tenants are publicly rated, and 59% of the tenants generate over $1 billion in revenue.

Source: Investor Presentation

Another great quality of STAG Industrial is that the company generally has business ties with established tenants, which helps enhance its risk profile. Simultaneously, the company has limited exposure to any specific tenant. Amazon is the largest tenant, generating 3.0% of annual rent revenue, while the next largest tenant generates only 0.9% of annual rent revenue.

Income-oriented investors are likely to appreciate the stock’s 4.5% yield, especially considering the company has never cut its dividend throughout its short history. In fact, it has increased its dividend for 12 consecutive years. Moreover, while rising interest rates are likely to be a headwind to STAG Industrial, being a REIT, it’s worth noting that the company’s payout ratio has been on the decline for six consecutive years.

Click here to download our most recent Sure Analysis report on STAG (preview of page 1 of 3 shown below):

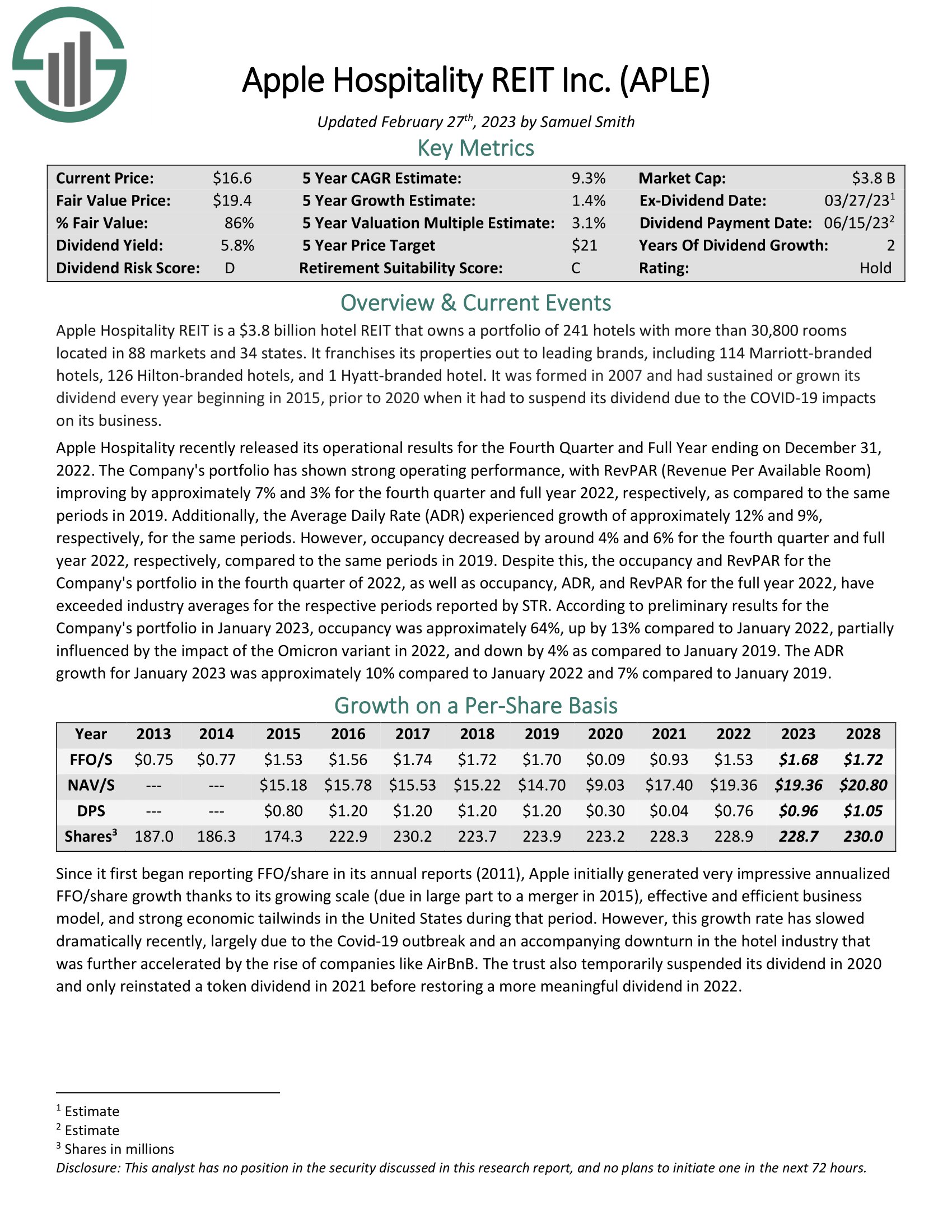

Monthly Dividend Stock #9: Apple Hospitality REIT, Inc. (APLE)

- Dividend Risk Score: D

- Dividend Yield: 6.7%

- Payout Ratio: 57%

Apple Hospitality REIT is a $3.3 billion hotel REIT that owns a portfolio of 220 hotels with an aggregate of 28,983 rooms located in urban, high-end suburban, and developing markets throughout 37 states. Concentrated on industry-leading brands, the company’s portfolio consists of 94 Marriott-branded hotels, 119 Hilton-branded hotels, four Hyatt-branded hotels, and two independent hotels.

Source: Investor Presentation

Apple Hospitality’s growth prospects will mostly come from an increase in rents. They were also selling less-profitable properties to acquire more beneficial properties. For example, in 2022, the company sold one hotel, a 55-room independent boutique hotel in Richmond, Virginia, for $8.5 million and acquired two hotels in Kentucky and Pennsylvania for $51 million, and $34 million, respectively.

The company does not have a long dividend history, as it became public in 2015. In 2016, the company did increase its annualized dividend substantially by 50%, from a $0.80 rate to a $1.20 rate. However, in the following years, the dividend stayed at that same rate until 2020, when the COVID-19 pandemic forced the company to cut its dividend and freeze it to a $0.20 rate for the year. In 2021, the company reinitiated the dividend by paying it every quarter instead of every month as it did before. Today, it pays a $0.08 monthly dividend.

Click here to download our most recent Sure Analysis report on APLE (preview of page 1 of 3 shown below):

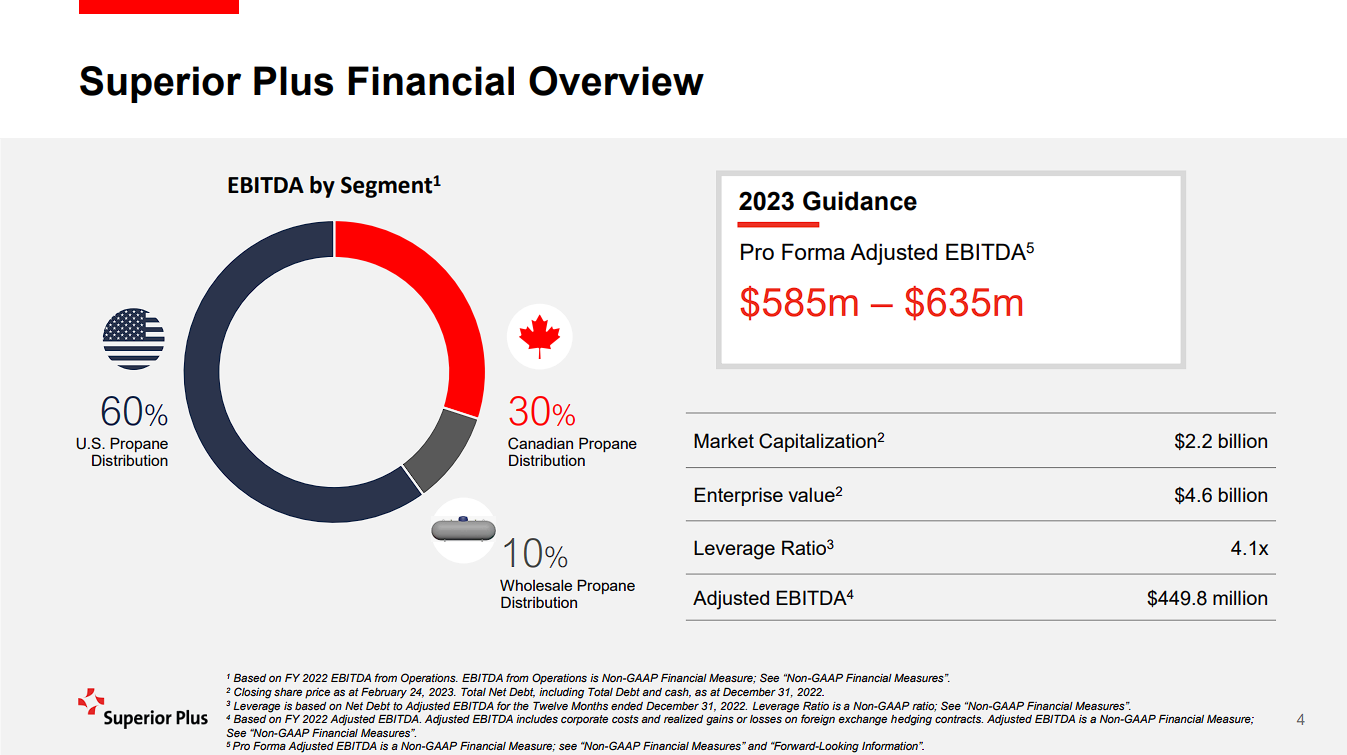

Monthly Dividend Stock #8: Superior Plus Corp. (SUUIF)

- Dividend Risk Score: D

- Dividend Yield: 6.7%

- Payout Ratio: 54%

Superior Plus Corporation is a relatively small industrial company but one of the larger propane distributors in North America. The company is the dominant distributor in Canada (30% of EBITDA), has significant operations in the U.S. (60% of EBITDA), and is also a propane wholesaler (10% of EBITDA). Superior Plus generates around $3.8 billion in annual revenues and is based in Toronto, Canada.

The company previously had a large Specialty Chemicals segment but sold this business in 2021 as part of a broader restructuring. Superior Plus is reorganizing its business to become a pure-play distribution company.

Source: Investor Presentation

Like many energy companies, Superior Plus was negatively impacted by the coronavirus pandemic and the resultant recession in the United States. As a result, the company incurred a 26% decrease in its earnings per share, from $1.63 in 2019 to $1.21 in 2020.

However, the company has stabilized its performance in recent quarters. In Q4 of 2022, the company generated an adjusted EBITDA of $135.7 million, a $30 million increase compared to the prior-year quarter.

The dividend yield will likely make up most of the returns of Superior Plus going forward, given the lack of share price growth over the last decade. Superior Plus currently distributes a monthly dividend of $0.06 per share in CAD, or C$0.72 per share annualized. In fact, the company has distributed the same dividend for several years in a row. U.S. investors need to keep in mind that the company pays its dividend in Canadian currency, which will have an impact on actual capital received based on the fluctuations in exchange rates. Based on an annualized dividend payout of $0.53 per share, Superior stock has a current dividend yield of 6.7%.

Click here to download our most recent Sure Analysis report on SUUIF (preview of page 1 of 3 shown below):

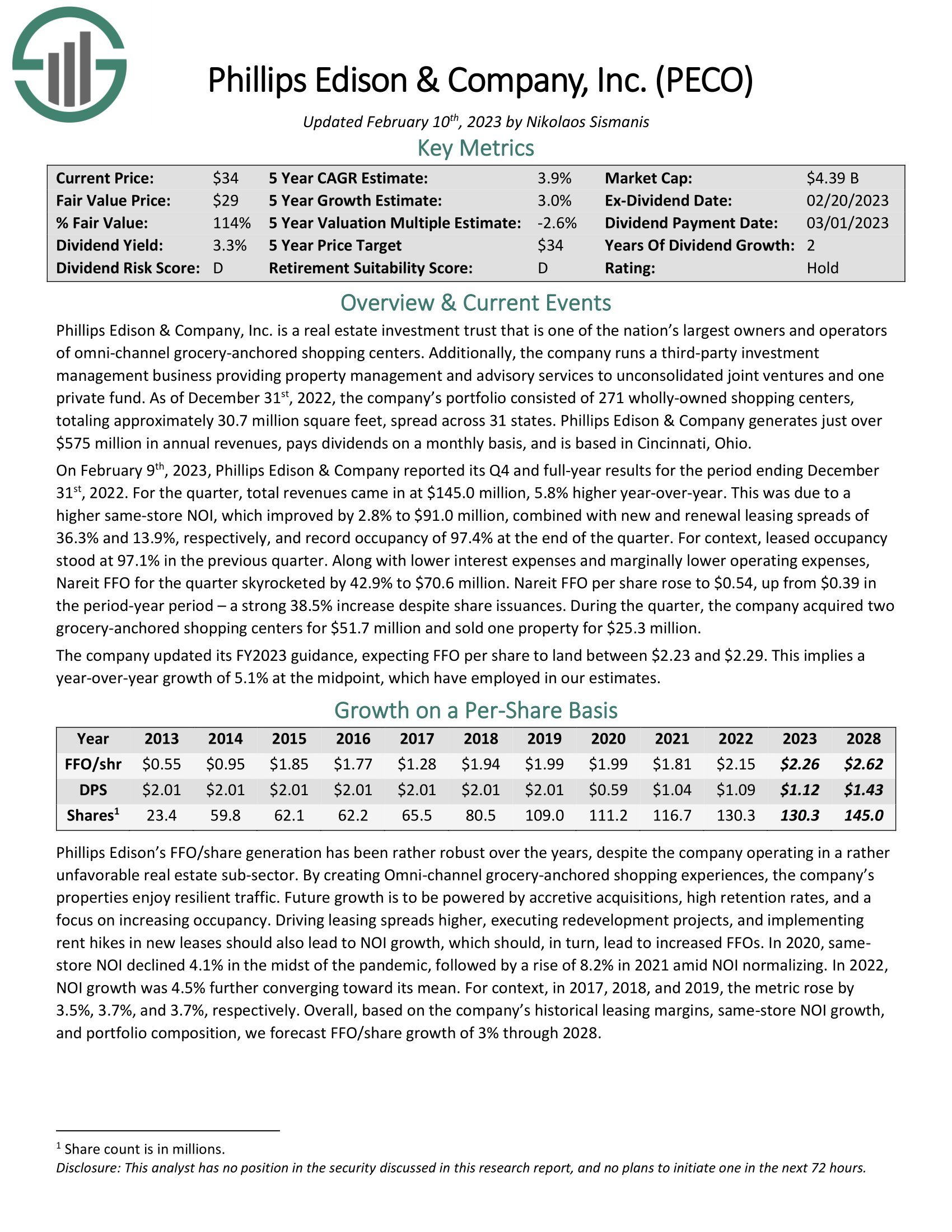

Monthly Dividend Stock #7: Phillips Edison & Company, Inc. (PECO)

- Dividend Risk Score: D

- Dividend Yield: 3.6%

- Payout Ratio: 50%

Phillips Edison & Company is an experienced owner and operator that is exclusively focused on grocery-anchored neighborhood shopping centers. It is a Real Estate Investment Trust (REIT) that operates a portfolio of 271 wholly-owned properties. The company has a 30-year history, but it began trading publicly only in the summer of 2021. Its management owns 7% of the company, and hence its interests are aligned with those of the shareholders.

Shopping centers are going through a secular decline due to the shift of consumers from brick-and-mortar shopping to online purchases. This shift has accelerated in the last two years due to the coronavirus crisis. However, Phillips Edison is well protected from this trend. It generates 71% of its rental income from retailers that provide necessity-based goods and services and has minimal exposure to distressed retailers.

Source: Investor Presentation

We believe Phillips Edison’s 3.6%-yielding monthly dividend be considered rather safe due to the company’s robust qualities, its low payout ratio, and solid balance sheet. Specifically, the trust has a payout ratio of 50% and an investment grade balance sheet, with a BBB- credit rating from S&P and a Baa3 rating from Moody’s. Moreover, it has well-laddered debt maturities and no material debt maturities for the next two years. Furthermore, 85% of its total debt has a fixed rate, which is paramount in the current environment of rising interest rates.

As a side note, while Phillips Edison has an investment-grade balance sheet, its leverage ratio (Net Debt to EBITDA) currently stands at 5.3. This is above the upper limit of our comfort zone (5.0) and reveals the eagerness of management to invest in the aggressive expansion of the trust. Nevertheless, we believe that a lower leverage ratio is necessary in order to render the REIT more resilient to unexpected downturns.

Click here to download our most recent Sure Analysis report on PECO (preview of page 1 of 3 shown below):

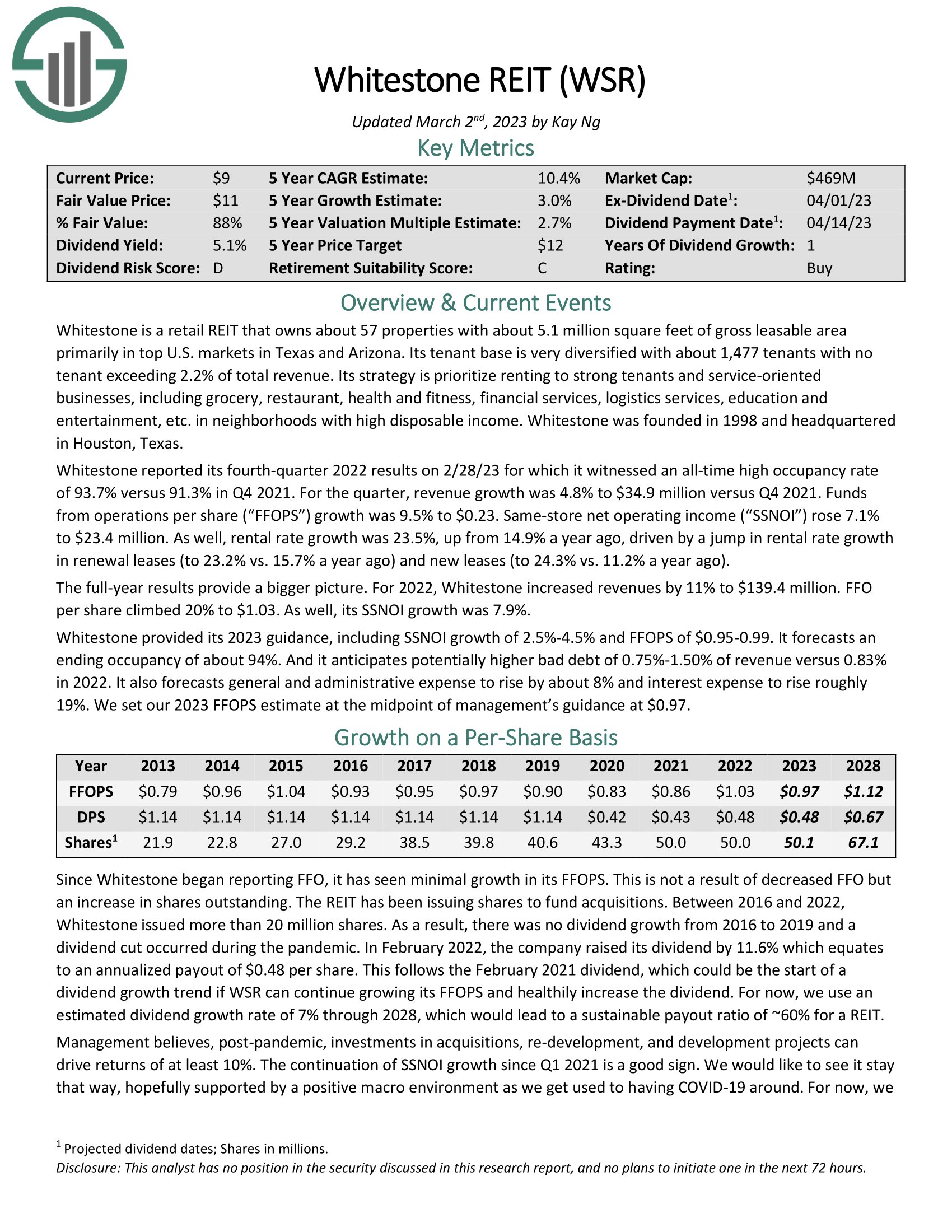

Monthly Dividend Stock #6: Whitestone REIT (WSR)

- Dividend Risk Score: D

- Dividend Yield: 5.4%

- Payout Ratio: 50%

Whitestone is a commercial REIT that acquires, owns, manages, develops, and redevelops properties it believes to be e-commerce resistant in metropolitan areas with high rates of population growth. The REIT currently owns 57 properties with about 5.1 million square feet of gross leasable area.

Its properties are located primarily in the southern United States, in areas with favorable demographics, such as income and economic growth. The trust’s properties are located primarily in Phoenix and Houston, with smaller allocations to other major cities in Texas.

Source: Investor Presentation

As a retail REIT, Whitestone was not spared from the coronavirus pandemic of 2020. As a result of the steep economic impact of the pandemic, Whitestone REIT reduced its monthly dividend by 63% in April 2020, from $0.095 to $0.035. The reduction was expected. Whitestone’s dividend-per-share was higher than its FFO-per-share every year between 2013 and 2019. A reduction during COVID-19 was both prudent and necessary. As the pandemic has subsided, Whitestone’s financial position has improved, which has allowed the company to raise its monthly dividend modestly to $0.04, where it currently stands.

Whitestone’s dividend seems secure going forward. We expect Whitestone to maintain a dividend payout ratio of 49% for 2023, based on our projected FFO-per-share of $0.97 for the full year. A dividend payout ratio below 50% is highly unusual for REITs and likely implies a high level of dividend safety. With such a low payout ratio, we believe the dividend is likely to increase from its current low base over the next several years. The stock currently has a 5.4% yield.

Click here to download our most recent Sure Analysis report on WSR (preview of page 1 of 3 shown below):

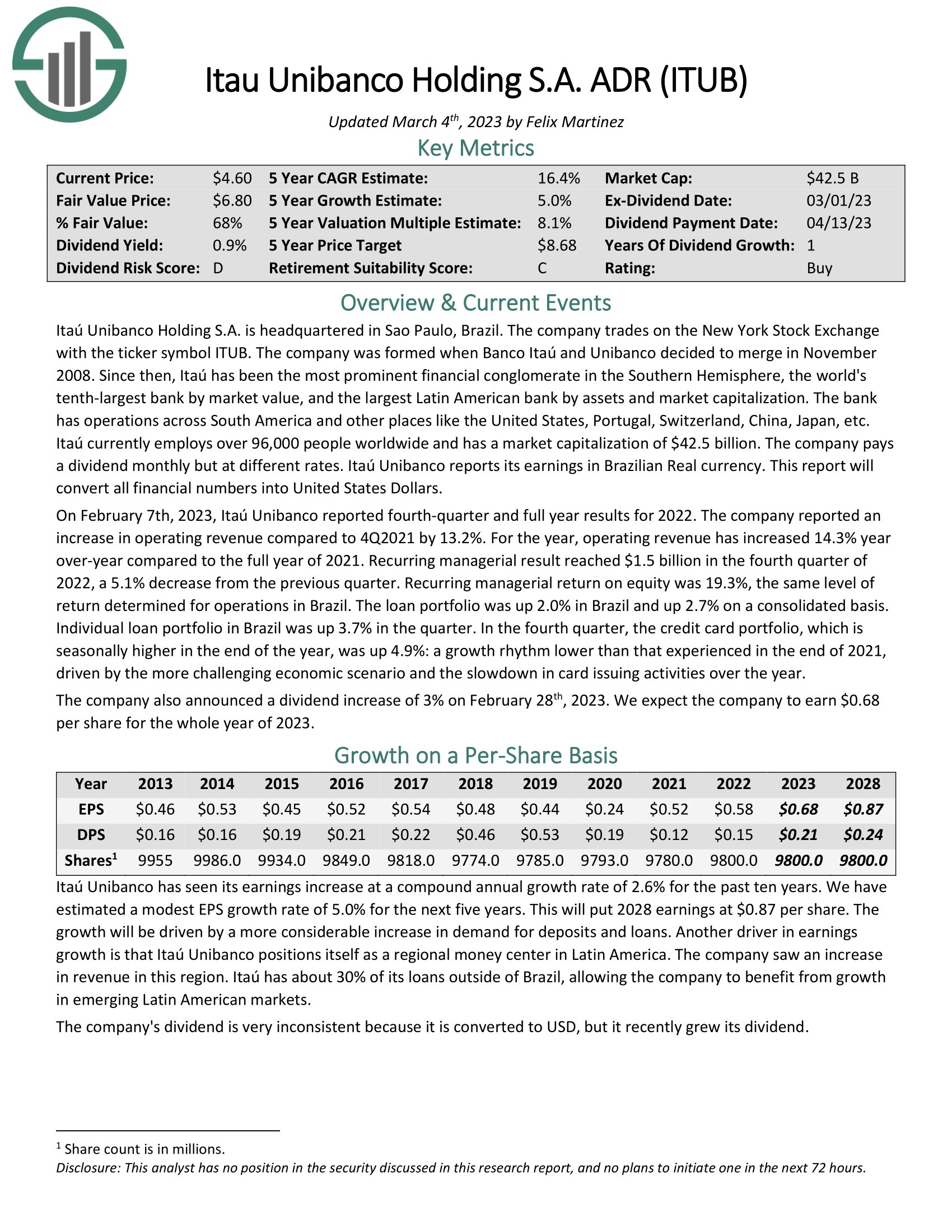

Monthly Dividend Stock #5: Itaú Unibanco (ITUB)

- Dividend Risk Score: D

- Dividend Yield: 4.6%

- Payout Ratio: 31%

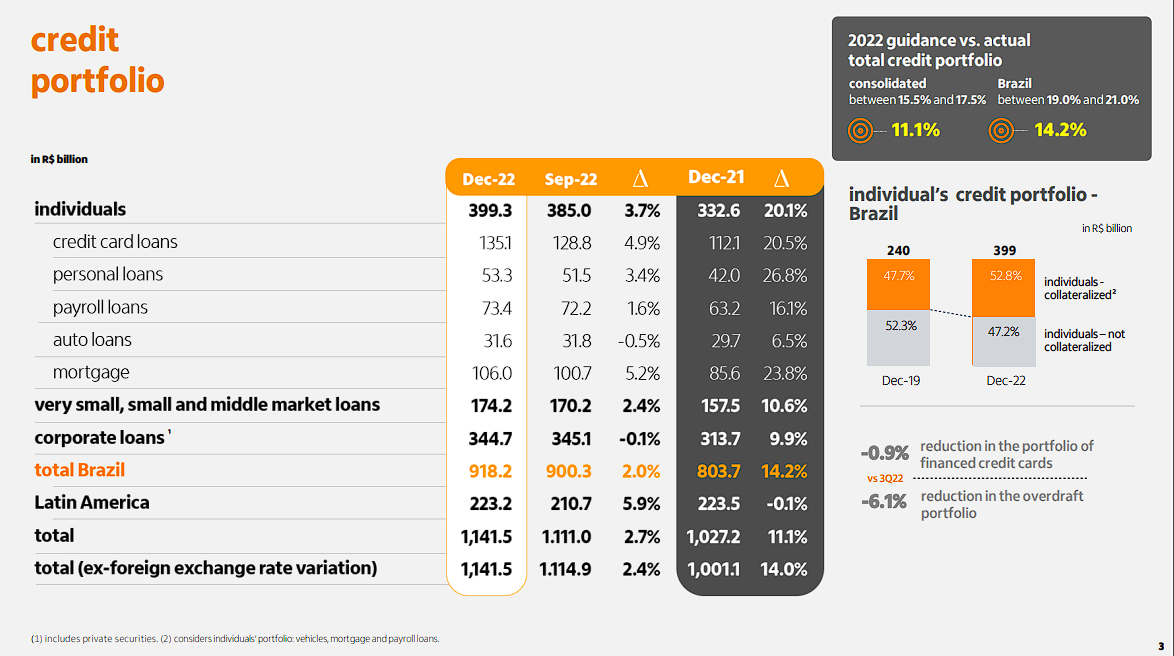

Itaú Unibanco is a very large bank that is headquartered in Brazil. ITUB is a large-cap stock with a market capitalization above $44 billion.

Itaú Unibanco conducts business in more than a dozen countries around the world, but the core of its business is in Brazil. It has significant operations in other Latin American countries and select businesses in Europe and the US.

Its scale is huge in relation to other Latin American banks. Itaú is the largest financial conglomerate in the Southern Hemisphere, the world’s 10th–largest bank by market value, and the largest Latin American bank by assets and market capitalization.

Source: Investor Presentation

It’s not uncommon for banks like Itaú Unibanco to try to cater to every type of consumer and business, just like major US banks have done by offering a range of services such as deposits, loans, insurance products, equity investing, and more, in order to attract customers. What sets Itaú Unibanco apart is its focus on emerging economies such as Brazil. However, emerging markets have struggled for many years. This is a cause for concern as economic growth is crucial for a bank’s expansion, and without it, Itaú Unibanco may face challenges in producing profit expansion.

Regarding its dividend, Itaú Unibanco has a conservative approach. The bank pays out dividends to shareholders based on its projected earnings and losses, with the goal being the ability to continue to pay the dividend under various economic conditions. Along with providing its recent quarterly results, the company also slightly increased its monthly dividend from $0.0033 per share to $0.0034 per share. Still, the yield is quite low at 0.83%. Thus, Itaú Unibanco isn’t a pure income stock by any means, as its yield is simply too small to be attractive to most income investors.

Click here to download our most recent Sure Analysis report on ITUB (preview of page 1 of 3 shown below):

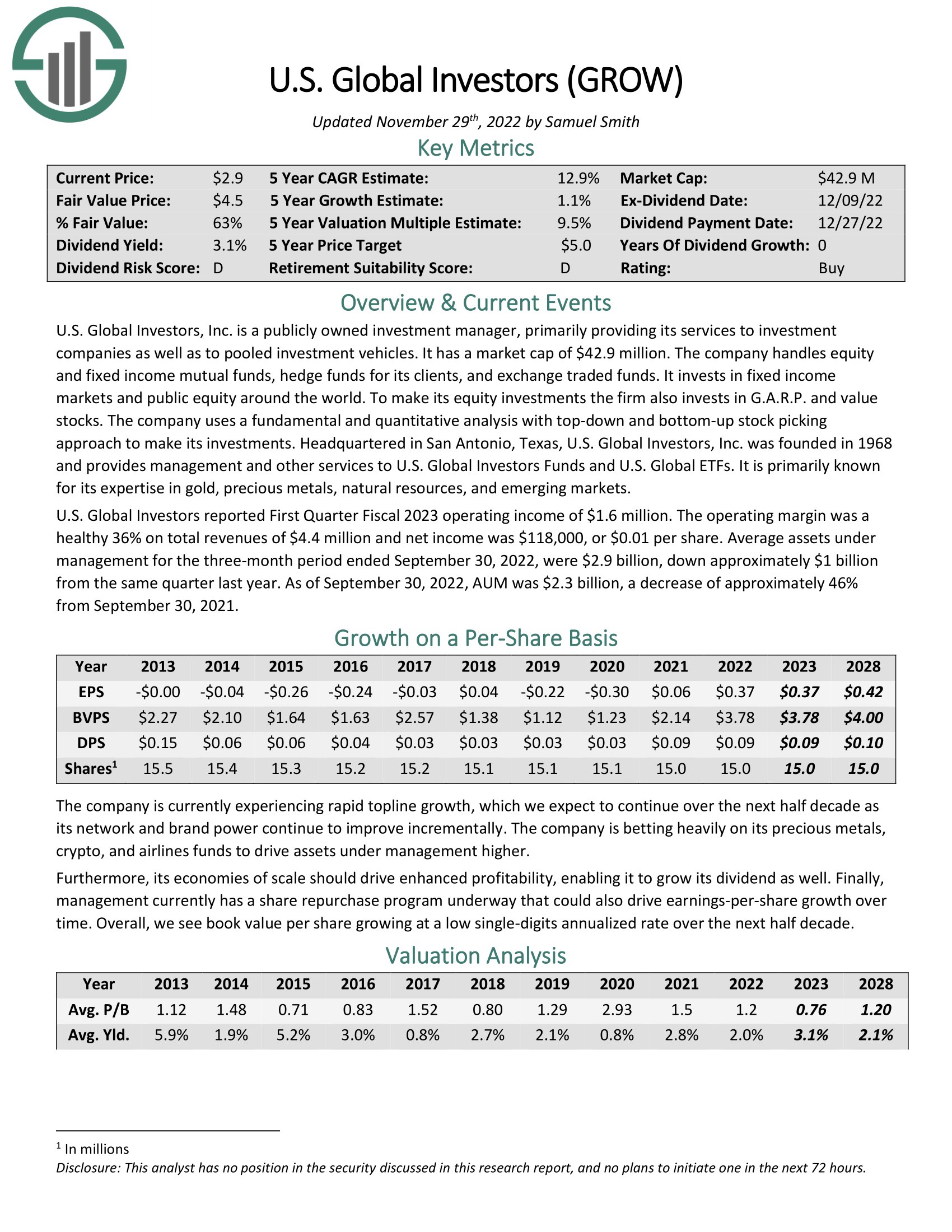

Monthly Dividend Stock #4: U.S. Global Investors, Inc. (GROW)

- Dividend Risk Score: D

- Dividend Yield: 3.5%

- Payout Ratio: 24%

U.S. Global Investors began more than 50 years ago as an investment club. Today, it is a publicly-traded registered investment advisor that looks to provide investment opportunities in niche markets around the world. The company provides sector-specific exchange-traded funds and mutual funds, as well as an interest in cryptocurrencies. U.S. Global Investors produced $24.7 million in annual revenue in 2022 and has a market capitalization of just $44 million.

The company is currently experiencing rapid topline growth, which we expect to continue over the next half-decade as its network and brand power continue to improve incrementally. The company is betting heavily on its precious metals, crypto, and airline funds to drive assets under management higher. Furthermore, its economies of scale should drive enhanced profitability, enabling it to grow its dividend as well. Finally, management currently has a share repurchase program underway that could also drive earnings-per-share growth over time.

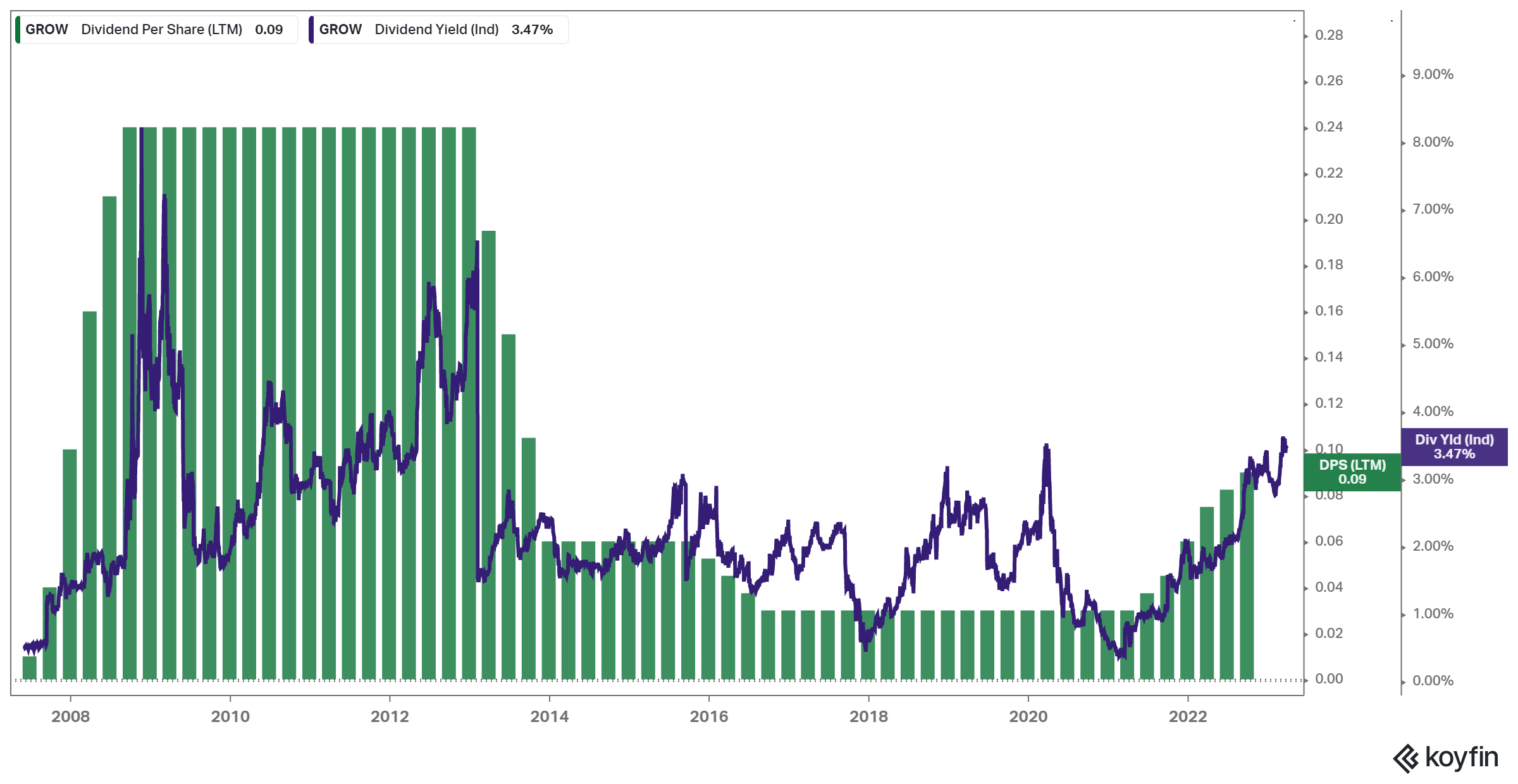

U.S. Global Investors has an impressive track record of paying monthly dividends for over 14 consecutive years, which is commendable. The current payout of $0.09 per share annually results in a yield of 3.1%, which, on a yield basis, may not be very attractive. However, it is noteworthy that the company has tripled its dividend since the onset of the pandemic.

It is important to mention that the company has a history of cutting its dividend. In the past decade, GROW has reduced its dividend, with the annual dividend per share being as high as $0.24 in 2012.

Source: Koyfin

Given the uncertain outlook for earnings growth, we anticipate that dividend growth may be challenging to achieve in the near future. Nonetheless, the company’s strong balance sheet suggests that it can continue paying dividends for a while, especially if it funds them with cash on hand rather than relying solely on earnings.

Click here to download our most recent Sure Analysis report on GROW (preview of page 1 of 3 shown below):

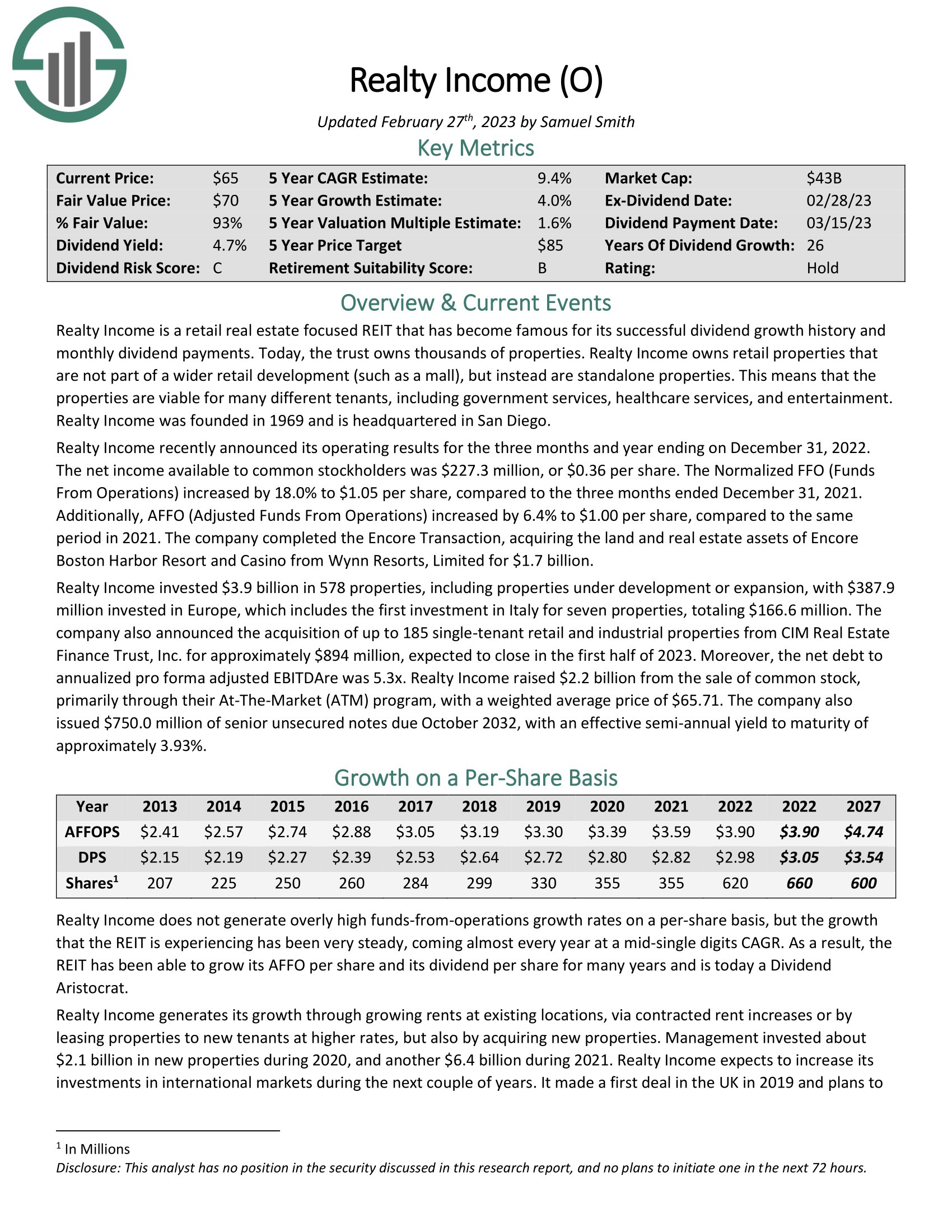

Monthly Dividend Stock #3: Realty Income Corporation (O)

- Dividend Risk Score: C

- Dividend Yield: 5.0%

- Payout Ratio: 79%

Realty Income owns more than 11,000 properties and has a market capitalization in excess of $40 billion. Realty Income focuses on standalone properties rather than ones connected to a mall, for instance. That increases the flexibility of the tenant base and helps the trust diversify its customer base.

The trust has earned a sterling reputation for its dividend growth history. Part of its appeal certainly is not only in its actual payout history but the fact that these payouts are made monthly instead of quarterly. Indeed, Realty Income has declared 633 consecutive monthly dividends, a track record that is unprecedented among monthly dividend stocks. Impressively, the company has increased its dividend more than 120 times since its initial public offering in 1994. Consequently, Realty Income is a member of the Dividend Aristocrats.

Source: Company’s IR

We believe the company’s dividend growth prospects remain robust, powered by the company’s proven recipe for driving accretive growth through its expansion strategy. The trust has a very long history of growing its asset base and its average rent, which have collectively driven its FFO-per-share growth. We don’t believe this has changed.

That said, Realty Income’s FFO-per-share and dividend growth may modestly slow down in the coming years due to the ongoing increase in interest rates, which affects all REITs. Still, we believe Realty Income’s balance is rather healthy, with its credit profile featuring a net-debt-to-EBITDA ratio of 5.3x and a weighted average term to maturity of more than six years.

Click here to download our most recent Sure Analysis report on O (preview of page 1 of 3 shown below):

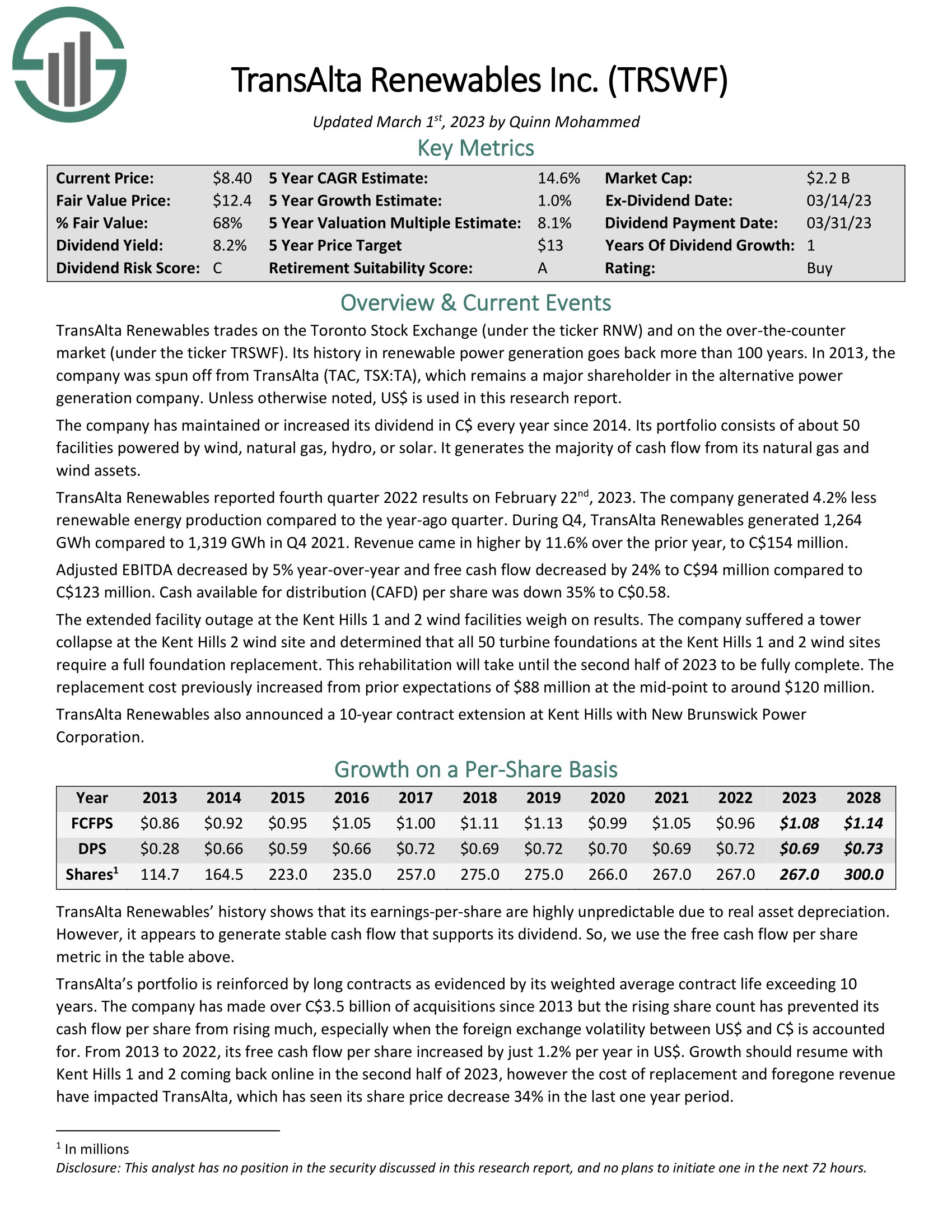

Monthly Dividend Stock #2: TransAlta Renewables Inc. (TRSWF)

- Dividend Risk Score: C

- Dividend Yield: 7.8%

- Payout Ratio: 68%

TransAlta Renewables, based in Calgary, Alberta, is a renewable energy infrastructure company that holds the title of Canada’s largest wind energy producer with a market capitalization of $3.2 billion. They have been involved in renewable power generation for over a century and were spun off from TransAlta in 2013. With a diversified portfolio, TransAlta Renewables has economic interests in several facilities, including wind, hydroelectric, natural gas, solar, natural gas pipelines, and battery storage projects, with an ownership interest of 2,965 megawatts of generating capacity.

Source: Annual Report

Investors are drawn to TransAlta Renewables because of their high dividend yield, which has been maintained or increased annually since 2014 at an average growth rate of 2.5%. However, rising interest rates may compress its CaFD, putting dividends at risk if the company doesn’t deleverage quickly enough. In 2018, the payout ratio was 71% based on earnings and 82% using distributable cash, but this ratio decreased to 66% in 2021 and 75% in 2022.

We expect a payout ratio of approximately 64% in 2023, assuming recent deleveraging efforts have a positive impact on the bottom line. Hence, despite this concern, we anticipate that the company will maintain its payouts in the near future.

Click here to download our most recent Sure Analysis report on TRSWF (preview of page 1 of 3 shown below):

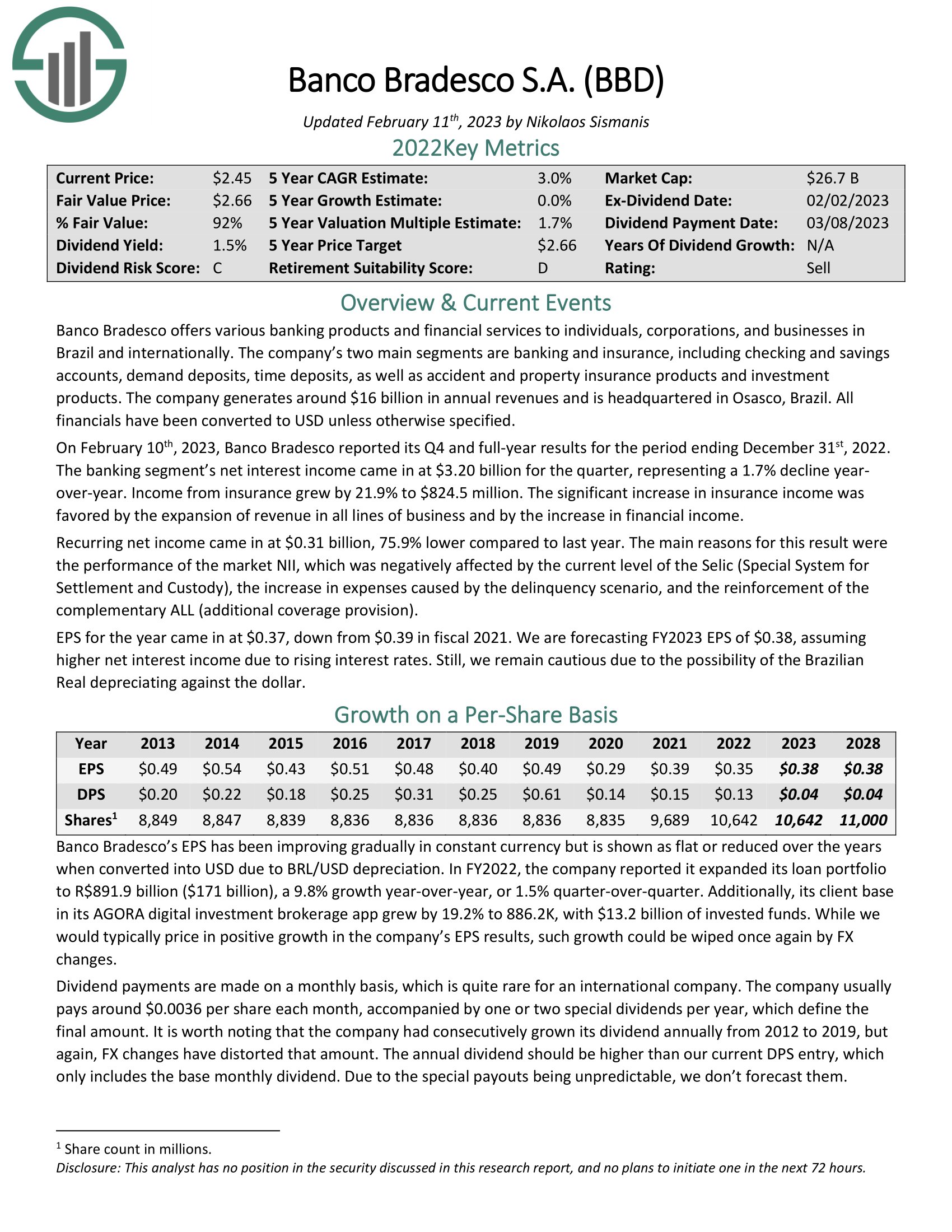

Monthly Dividend Stock #1: Banco Bradesco S.A. (BBD)

- Dividend Risk Score: C

- Dividend Yield: 1.6%

- Payout Ratio: 11%

Banco Bradesco is a financial services company based in Brazil. It offers various banking products and financial services to individuals, corporations, and businesses in Brazil and internationally. The company’s two main segments are banking and insurance, including checking and savings accounts, demand deposits, and time deposits, as well as accident and property insurance products and investment products.

The 2020 COVID-19 pandemic year was very difficult for Banco Bradesco, as the global economy was negatively impacted by the coronavirus pandemic. Fortunately, the company has recovered notably during the past two years.

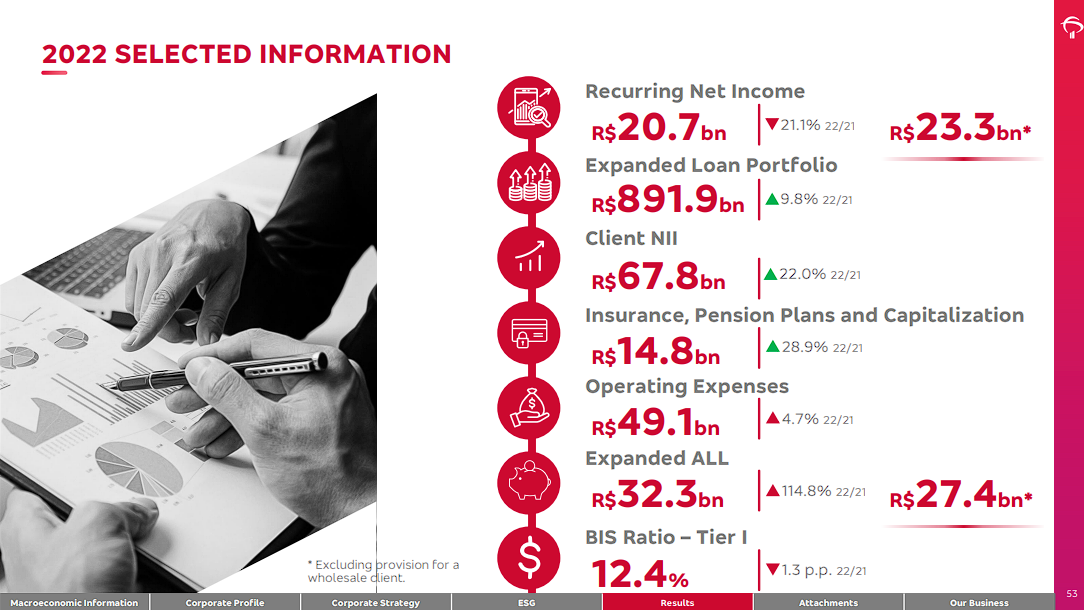

In FY2022, the company reported it expanded its loan portfolio to R$891.9 billion ($171 billion), a 9.8% growth year-over-year, or 1.5% quarter-over-quarter. Additionally, its client base in its AGORA digital investment brokerage app grew by 19.2% to 886.2K, with $13.2 billion of invested funds.

While we would typically price in positive growth in the company’s EPS results based on its continuous product expansion, such growth could be wiped once again by FX changes. This has been a consistent theme for the company. Its EPS has been improving gradually in constant currency, but it is shown as flat or reduced over the years when converted into USD due to the BRL’s depreciation against the USD.

Source: Investor Presentation

The company usually pays around $0.0036 per share each month, accompanied by one or two special dividends per year, which define the final amount. It is worth noting that the company had consecutively grown its dividend annually from 2012 to 2019, but again, FX changes have distorted that amount. The annual dividend should be higher than Banco Bradesco’s $0.04 annualized monthly dividend, as it only includes the base payouts. The company has a history of paying special dividends as well. Still, it’s almost impossible to forecast their value, especially given the FX factors involved.

Click here to download our most recent Sure Analysis report on BBD (preview of page 1 of 3 shown below):

Final Thoughts

In conclusion, monthly dividend stocks can be an attractive option for investors seeking a steady source of income, whether that’s for covering one’s everyday expenses or for regular compounding. While no investment comes without risk, some monthly dividend stocks have demonstrated a history of financial stability, consistent earnings, and reliable dividend payments.

Our list of the ten safest monthly dividend stocks presented in this article includes companies from a variety of industries that rank high based on our Dividend Risk scoring system.

Nevertheless, there are numerous other monthly dividend stocks available, each with its unique features and benefits. We recommend exploring these options to find the ones that align with your requirements and preferences. However, it is essential to keep in mind that every investment carries its own inherent risks, so be sure to conduct thorough research before making any decisions.

If you are interested in finding more high-quality dividend growth stocks suitable for long-term investment, the following Sure Dividend databases will be useful:

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly:

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

{kind=link}