Earlier this yr in January, the Reserve Financial institution of India’s versatile inflation concentrating on framework accomplished a decade as the first determinant of Indian financial coverage. Informally adopted in January 2014 and formally in 2016, the framework has been the topic of appreciable debate over the previous few years.

There actually are two branches to India’s inflation concentrating on debate: the numerical goal—4% in a band of 2-6%, and the measure of inflation itself, which is headline inflation as measured by the buyer value index (CPI). The Financial Survey for 2023-24 has waded into this dialogue, calling for a re-examination of the framework to see whether or not the goal could be spelt out by way of inflation excluding meals.

The Survey makes a reasonably compelling argument: meals costs can’t actually be countered by instruments on the disposal of the financial coverage authority. As an alternative, it’s the authorities that acts and helps cool these costs, which in flip “prevents farmers from benefiting from the rise by way of commerce of their favour”.

The Survey as a substitute means that RBI deal with controlling inflation excluding meals, leaving the federal government to maintain the hit to the pockets of the poor and low-income households from rising meals costs by direct profit transfers and even meals coupons.

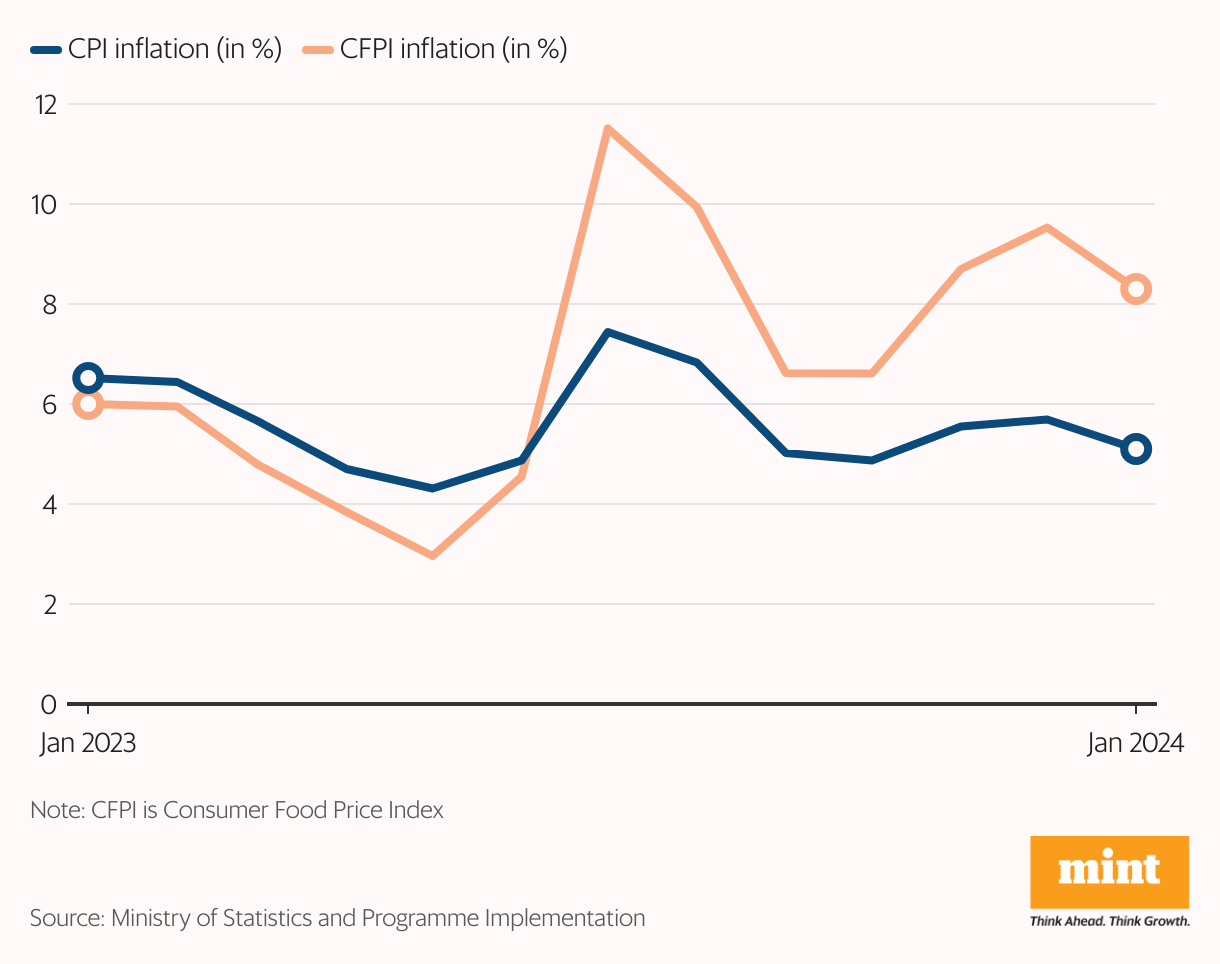

Given a selection, RBI would in all probability bounce on the alternative to not have to fret about meals costs. Take into account the final 10 months, which have seen CPI inflation common 5.1% and keep firmly inside RBI’s goal band of 2-6%.

On the similar time, Client Meals Value Inflation has averaged 8.4%, with the June print at a six-month excessive of 9.36%. No surprise RBI’s financial coverage committee (MPC) is targeted on meals costs and has left rates of interest unchanged for eight conferences in a row.

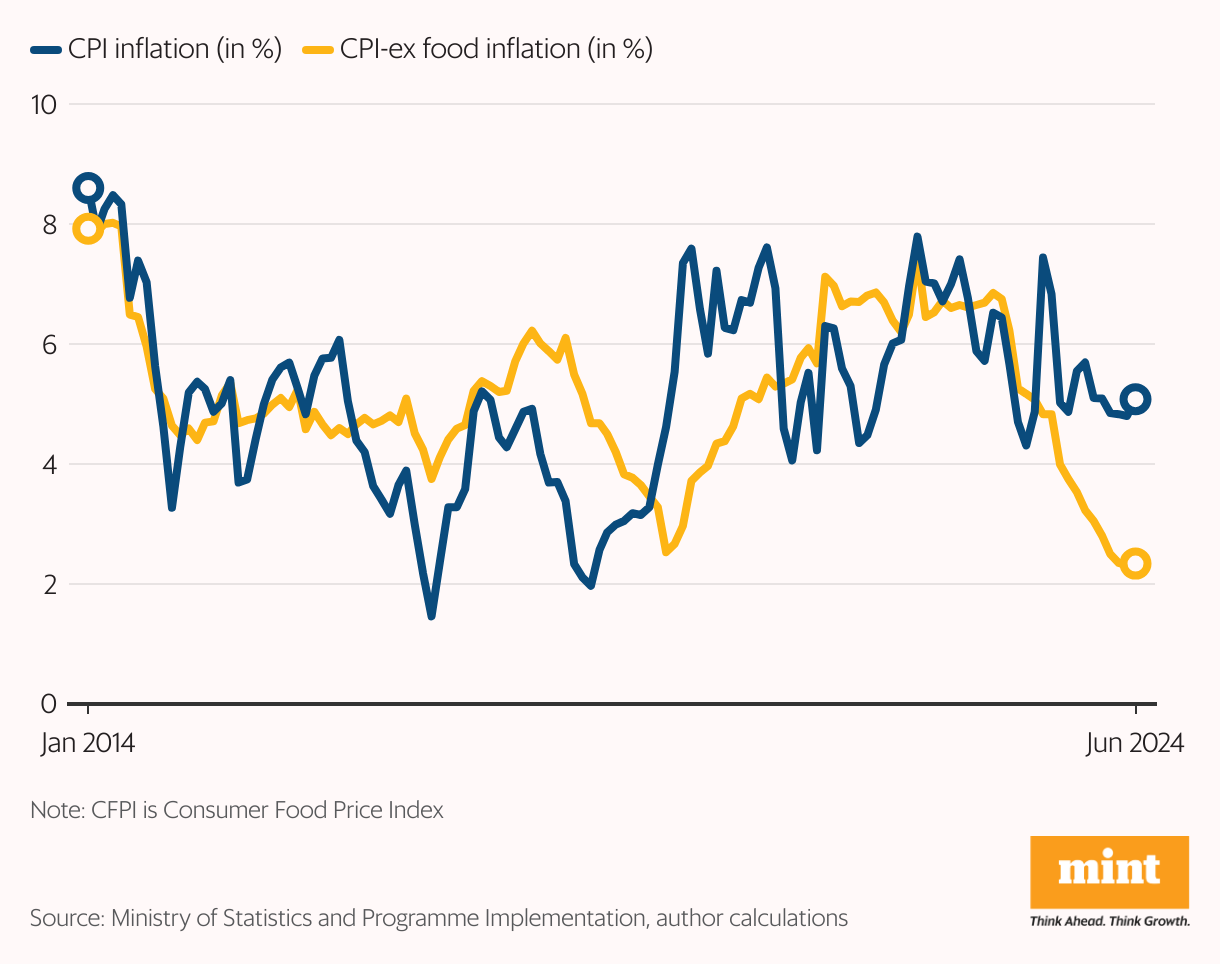

There’s, nonetheless, an issue in concentrating on non-food inflation. Had RBI been concentrating on this narrower measure of inflation, as recommended by the Financial Survey, its financial coverage actions would have seemed very completely different from what we’ve got seen.

As per the legislation, the central financial institution is deemed to have failed when common CPI inflation is outdoors the 2-6% band for 3 quarters in a row. This occurred in 2022, when headline retail inflation averaged 6.3% within the January-March interval, 7.3% in April-June, and seven.0% in July-September.

As soon as it began turning into clear that RBI was possible going to fail in its mandate, the MPC tightened the screws and commenced elevating the coverage repo charge beginning in Could 2022. The repo charge ended 2022-23 at 6.50%, 250 foundation factors greater than the pandemic-low of 4.00%.

If RBI was concentrating on non-food inflation, the central financial institution would have failed to fulfill its mandate in 2021 itself, with CPI inflation excluding meals averaging 6.6% in April-June 2021, 6.7% in July-September, and 6.8% in October-December.

The central financial institution would have been pressured to start out its charge hike cycle a yr sooner than it really did, and financial development could not have been as sturdy as it’s now. Low meals inflation of three.1% in 2021, down from 9.6% in 2020, helped drag down the headline charge to a stage that allowed India’s rate-setters to assist development amid the raging covid-19 pandemic.

To make sure, it is a hypothetical train. Additional, headline inflation could not essentially be one of the best goal, with Ashima Goyal, one of many three exterior members on the MPC, having talked up the usefulness of core inflation—or inflation excluding meals and gasoline—as a coverage anchor. Nonetheless, even Goyal thinks “fairness and shopper welfare issues assist concentrating on headline CPI”.

Nonetheless, the intervention by the Financial Survey comes at a quite opportune time. The present inflation goal of 4% in a band of 2-6% is legitimate till March 2026. Coincidentally, it’s anticipated that the ministry of statistics and programme implementation will launch the brand new CPI inflation collection, based mostly on the newest Family Consumption Expenditure Survey, in early 2026.

The brand new inflation collection ought to consequence within the weight of the ‘meals and drinks’ group of the CPI decreasing considerably from 45.86% at current; the identical ought to maintain true for the Client Meals Value Index, which accounts for 39.06% of the CPI at present. This in itself ought to weaken the affect meals costs exert over the headline inflation charge, making RBI’s job that a lot simpler.

{kind=link}