Anna Moneymaker/Getty Images News

Taiwan Semiconductor Manufacturing Company Limited (NYSE:TSM) (“TSMC”) reported its Q4 and FY22 earnings release earlier today (January 12). But we believe investor attention has turned to its FY23 outlook and whether the company could continue to deliver its robust execution moving ahead.

The leading pure-play foundry reported Q4 revenue growth of 42.8% (Vs. consensus: 45.3%). However, its Q4 gross margin of 62.2% outperformed the Street’s projections of 60.4%. As such, it’s clear that TSMC’s technological and pricing leadership remains rock solid, even as it navigates a significant downturn in consumer electronics.

Despite that, there is some cause for concern for TSMC bulls. The company’s FY23 midpoint CapEx outlook of $34B is more than 6% below FY22’s metric. However, it shouldn’t be surprising, given the macro headwinds. Moreover, we believe a 6% revision is way better than the malaise in the memory industry.

With TSMC still positioning 2023 potentially as a “slight growth” year, we believe there are limited downside risks in the downgraded Wall Street estimates. Hence, as long as TSMC can continue executing well through the industry headwinds, it should be well-positioned to recover.

Notwithstanding, investors should expect a weak H1, with Q1’23 revenue growth potentially down by more than 14% QoQ. However, TSMC guided with confidence on meeting its long-term gross margins guidance of 53% and higher as it works on cost improvements.

Notably, the company is expected to see significant costs increase, with its Arizona fab total cost of ownership (TCO) more than five times its TCO in Taiwan. Therefore, it’s imperative that TSMC continues to maintain its technological superiority against Intel (INTC) and Samsung (OTCPK:SSNLF) to justify price increases.

Accordingly, the company’s 3nm or N3 ramp is still on track, leveraging the new data center processors and GPUs from Advanced Micro Devices (AMD) and Nvidia (NVDA). However, Apple’s ramp on TSMC’s N3E (enhanced version of its N3) should occur in H2, contributing to its recovery in H2.

However, management is reticent to comment on whether it will be a rapid recovery. Nevertheless, we think the prognosis is prudent, given worse macroeconomic headwinds.

The company is optimistic about outperforming the semi industry in 2023, as management forecasted it could see its ex-memory revenue decline by 4% YoY.

Hence, 2023 could still turn out to be a promising year for TSMC as it leverages tailwinds from hyperscaler/data center growth, while consumer electronics/PC could remain in the doldrums.

However, we believe investors should continue to monitor the company’s ramp efficiencies in Arizona and Japan. In addition, DIGITIMES highlighted previously that TSMC is expected to receive significant subsidies in Arizona, which could help lower its TCO.

TSMC has also been developing its supply chain ecosystem in the U.S. to improve its cost efficiencies.

Besides its U.S. and Japan expansion, TSMC also expects to invest in a specialty fab in Europe (possibly in Germany), leveraging the growth in automotive chips. Interestingly, the company is also expected to garner orders from Tesla (TSLA) recently, supplanting Samsung as Elon Musk’s main foundry partner, demonstrating its ability to continue gaining share against its arch-rivals.

Therefore, we encourage investors to continue monitoring TSMC’s progress in its overseas expansion and assess the impact on its gross margins.

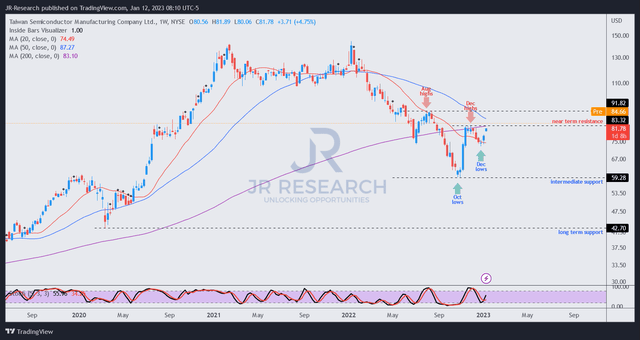

TSM price chart (weekly) (TradingView)

We note that investors likely anticipated a solid release, as TSMC has recovered remarkably from its December lows.

As such, it’s re-testing its previous December highs while also in line with its long-term moving averages.

At an NTM EBITDA of 7.4x, it’s no longer expensive and also in line with its peers’ median of 7.7x (according to S&P Cap IQ data).

However, we expect downward revisions, as the consensus estimates have overstated the company’s revenue estimates in H1’23, and thus are impacting its valuation multiples.

Also, we think the 200-week moving average (purple line) could continue to resist buyers’ upward momentum. Coupled with its more well-balanced valuation and potential cost overrun from its overseas expansion, we believe TSMC investors should remain patient and wait for a deeper pullback to improve reward/risk.

Rating: Hold (Reiterated).

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

")

performed in Q4 2023")

{kind=link}