champc

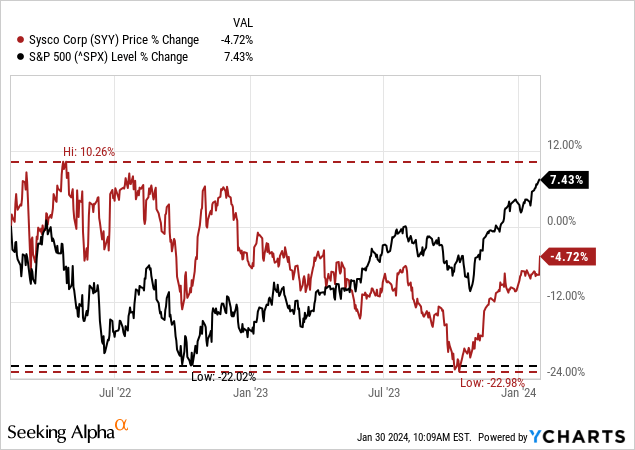

On Tuesday, Sysco Corporation (NYSE:SYY) reported second quarter results for fiscal 2024 and in the first hour of trading it seems like investors are quite pleased with the results and the stock is up almost 4%. My last article about Sysco was published almost 2 years ago – in February 2022 – and since then the stock hasn’t moved much. I rated the stock as a “Hold” and this was probably the right call as investors only collected dividends in the meantime.

And while the S&P 500 was also not a great investment during these two years, Sysco still underperformed the index. Let’s use the occasion of the quarterly results to provide an update on Sysco and ask the question if the stock is still a “Hold”.

Second Quarter Results

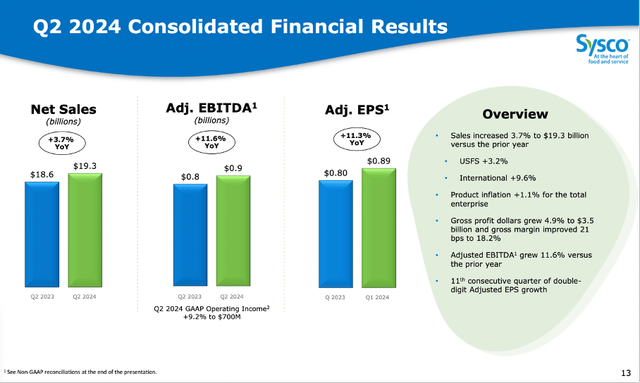

The results Sysco reported were more or less in line with expectations. While revenue missed slightly, the company could beat earnings per share expectations a little bit. But missing by $30 million on $19.3 billion in revenue is really not worth mentioning and we can see results in line with expectations.

Sysco Q2/24 Presentation

Sysco could grow its top line by 3.7% year-over-year and sales increased from $18,594 million in Q2/23 to $19,288 million in Q2/24. Operating income increased from $641 million in the same quarter last year to $700 million this quarter. And finally, diluted earnings per share almost tripled from $0.28 in Q2/23 to $0.82 this quarter. But the reason for the jump in earnings can be found in last year’s quarter, which included a charge of $315.4 million in other expenses related to pension settlement charges.

When looking at adjusted earnings per share we see an increase of 11.3% year-over-year to $0.89 and Sysco reported the 11th consecutive quarter of double-digit adjusted EPS growth.

Reaffirming Guidance

Aside from results being in line with analysts’ expectations, Sysco also reaffirmed its guidance for fiscal 2024. For the full year, management is expecting sales of $80 billion and adjusted earnings per share to be in a range of $4.20 to $4.40. This would result in mid-single digit growth for sales and mid-to-high single digit growth for earnings per share.

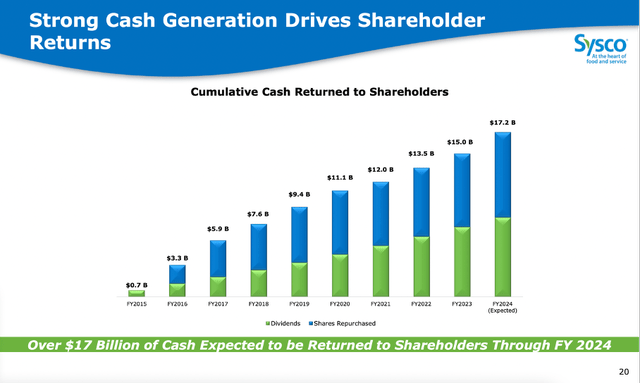

Increased Share Buyback Volume

Management also announced it will return approximately $2.25 billion back to shareholders in fiscal 2024. And with Sysco paying about $1 billion annually in dividends, this would lead to $1.25 billion spent on share buybacks. Previously expectations for share buybacks were only $750 million and considering a market capitalization of $38 billion right now, Sysco can repurchase about 3.3% of its outstanding shares in 2024.

And while Sysco has never been buying back shares with an aggressive pace, it constantly lowered the number of outstanding shares. In the last ten years, the number of outstanding shares declined from almost 600 million to 507 million right now and the cumulate cash returned to shareholders (dividend and share buybacks) increased every year.

Sysco Q2/24 Presentation

Growth Assumptions

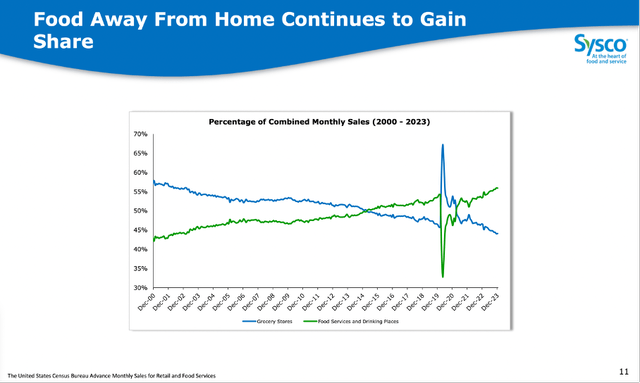

When looking at Sysco we can be quite optimistic about long-term growth as the company seems to be profiting from several long-term trends, which are tailwinds for the company. The COVID-19 pandemic and the resulting lockdowns were a shock for Sysco – one that is visible in the results as well as the stock price chart – but it seems like many trends are continuing on the “pre-COVID path”.

Sysco Q2/24 Presentation

Looking at the percentage of sales in grocery stores vs. the sales of food services and drinking places, we see a clear trend for the last 2.5 decades. While grocery stores are constantly losing market shares – aside from a few quarters during COVID-19 in which grocery sales skyrocketed – the food services and drinking places are gaining market shares and are now already at 55% market share.

Sysco Q2/24 Presentation

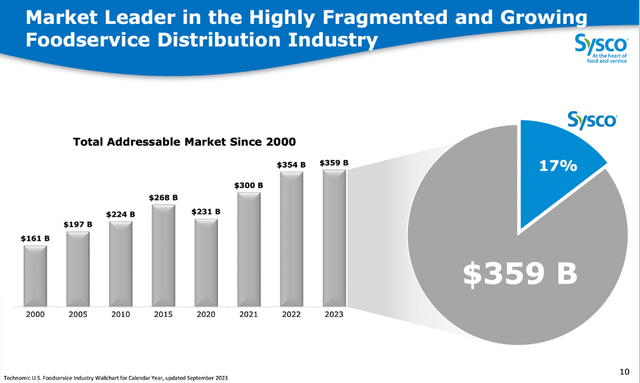

This is also resulting in a constantly growing total addressable market for Sysco over the last decades. Once again, we can clearly see the COVID-19 shock in 2020 but the total addressable market exceeds pre-COVID levels and is at $359 billion right now with Sysco having a market share of 17%.

And not only management seems to be optimistic about future growth – analysts are also expecting growth rates in the high single digits for the years to come. Between fiscal 2023 and fiscal 2028, analysts are expecting earnings per share to grow with a CAGR of 8.50%.

But Also Being Cautious

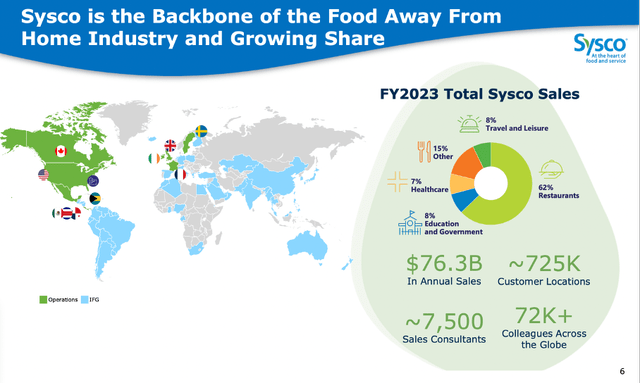

I have now mentioned in several articles (see here and here for example) that I would be rather cautious in the coming quarters. And in case of a recession, Sysco might also be one of the businesses that could be hit hard. The biggest part of sales is generated by distributing food to restaurants and usually people go less to restaurants when times are tough. On the other hand, sales for education and government as well as hospitals will most likely be stable even during recessions (but these two are only responsible for 15% of total sales). And when talking about restaurants we also must differentiate between expensive restaurants on the one hand or fast-food chains and canteens on the other hand. In case of a recession, people might eat less in more pricey restaurants but instead more frequent in canteens and therefore sales for Sysco might not suffer at all (but we should be cautious about high growth rates).

Sysco Q2/24 Presentation

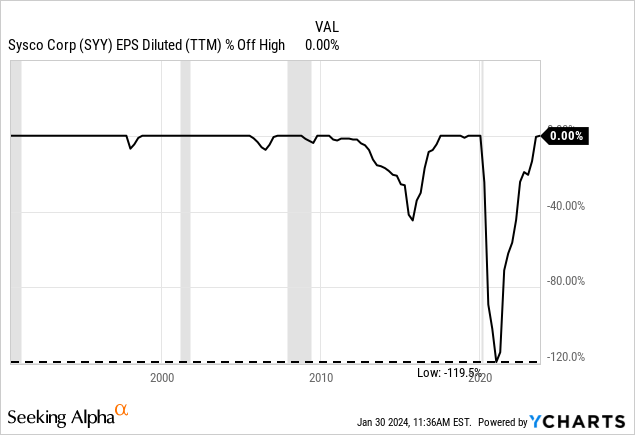

And when looking at the chart we can make the argument for a trend continuing and a breakout in the coming quarters. But it also seems possible that Sysco will not be able to break above the resistance level which is currently in the range of $85 and $90 and we might see lower stock prices once again.

Reasonably Valued

In the end we can make the argument that Sysco is fairly valued at this point. When determining an intrinsic value for Sysco by using a discount cash flow calculation we are calculating with a 10% discount rate – as always. As basis for our calculation, we take the free cash flow of the last four quarters, which was $1,999 million and when looking at the numbers in the last 10 years this seems like a reasonable assumption. Additionally, we calculate with 507 million outstanding shares and also assume 5% growth from now till perpetuity. When calculating with these assumptions, we get an intrinsic value of $78.86 for Sysco and the stock is fairly valued at this point.

We can also make the argument that 6% annual growth for the bottom line is reasonable. All other assumptions being the same, this would result in an intrinsic value of $98.57 for Sysco and the stock would be undervalued at this point.

As I already mentioned above, the valuation seems reasonable at this point, but these growth assumptions are not taking into account the risk of a recession in the years to come. And although Sysco performed quite well during past recessions – 2020 was an outlier and not a “normal” recession – we should be rather cautious for the next few years as 5% or 6% annual growth might be too optimistic.

Bottom Line

I would continue to see Sysco as a “Hold” and a more or less fairly valued stock at this point. I see slight upside potential but considering the resistance level in the chart and the risk of a recession, I don’t think I would invest in Sysco at this point – like I won’t invest in many other stocks and rather trim positions.

")

{kind=link}