Shares of Southwest Airways (NYSE: LUV) had been down on Friday, a day after the corporate delivered better-than-expected outcomes for the second quarter of 2022. Income and earnings surpassed expectations and whereas demand tendencies have stayed sturdy, rising prices stay a ache level. Right here’s a take a look at the airline’s expectations for the remainder of the 12 months:

Income and profitability

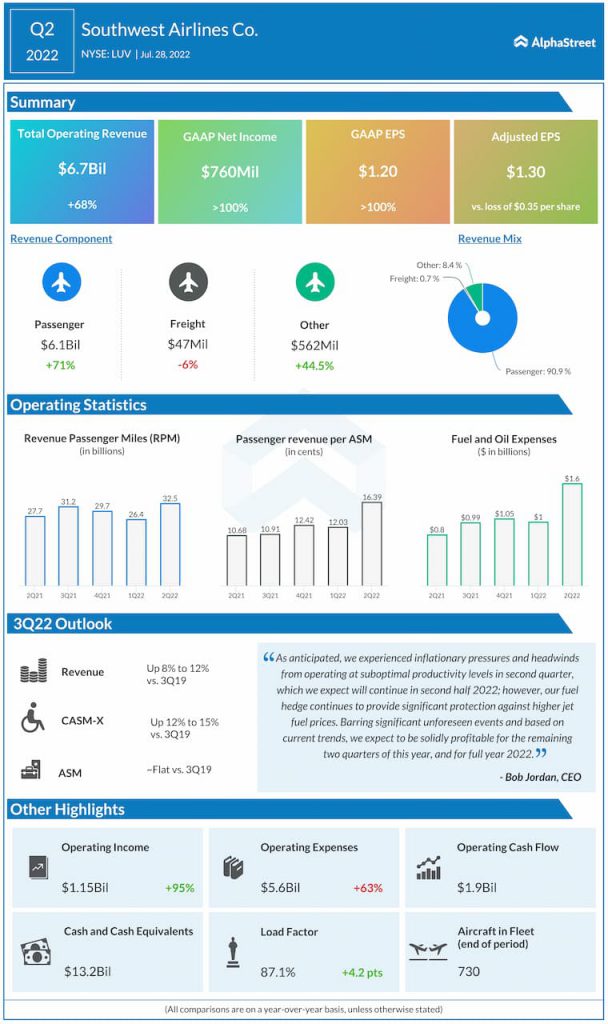

Southwest generated revenues of $6.7 billion for the second quarter of 2022, which was up 68% year-over-year and 14% versus Q2 2019. Revenues improved sequentially by way of every month of the second quarter resulting in the corporate’s strongest month-to-month income efficiency in June.

The highest line progress was fueled by sturdy demand tendencies as leisure demand remained strong whereas enterprise demand witnessed a significant enchancment. Managed enterprise demand was down 19% in June in comparison with down 36% in March. This enchancment is anticipated to proceed within the third quarter of 2022. Southwest expects working revenues in Q3 2022 to extend 8-12% versus Q3 2019.

Southwest reported adjusted EPS of $1.30 for the second quarter. This compares to a lack of $0.35 per share within the year-ago interval. On its quarterly convention name, the corporate mentioned this was essentially the most secure income surroundings it has had in over two years and that it stays well-protected with its gasoline hedge. Primarily based on these components, the airline expects to be worthwhile for the third and fourth quarters in addition to the complete 12 months of 2022.

Demand and capability

Southwest witnessed journey demand acquire traction in March. Each leisure and enterprise journey noticed vital momentum by way of the second quarter. Wanting on the third quarter, demand tendencies stay sturdy with energy in passenger bookings yields and cargo components. Demand for each leisure and enterprise journey are trending effectively.

Capability in Q2 was up practically 12% year-over-year however down 7% in comparison with the identical interval in 2019. For the third quarter of 2022, capability is anticipated to be roughly flat in comparison with Q3 2019. For the fourth quarter, capability is estimated to be down 1-2% in comparison with the identical quarter in 2019. The corporate is at the moment projecting capability for the primary quarter of 2023 to extend 10% from the primary quarter of 2022.

Prices

Southwest continues to expertise inflationary pressures. Within the second quarter of 2022, working bills per obtainable seat mile, excluding gasoline and oil expense, particular objects, and profitsharing (CASM-X) elevated 13.1% from the identical interval in 2019.

For the third quarter of 2022, CASM-X is anticipated to be up 12-15% versus the 2019 ranges. Greater than half of this improve is anticipated to be pushed by larger charges for labor and advantages and the rest is attributable to headwinds brought on by working at suboptimal productiveness ranges.

Click on right here to learn the complete transcript of Southwest Airways’ Q2 2022 earnings convention name

From Natural Disasters")

{kind=link}