“Time is the scarcest resource leaders have. Where they allocate it matters – a lot.” That’s according to a Harvard Business Review study on how CEOs spend their time of which a great deal is spent working. CEOs put in 9.7 hours per weekday, on average, also conducting business on 79% of weekend days when they spend 3.9 hours daily, on average. Top that off with several hours a day on 70% of vacation days and you start to see just how grueling these top positions are. Then, when a CEO decides to cash in on some shares and spend the money on something nice, they’re berated by investors. Nobody said being a CEO was easy.

When a company’s CEO or other insiders start buying shares, their intentions are clear. They believe in their company, and they believe their company’s stock is at a bargain price. A study by Harvard and Yale students found that insider purchases tend to beat the market by 11.2% per year. But what about when insiders sell shares? Does that mean they’re losing faith in their company? Not always.

Reasons Insiders Sell Stock

There are multiple reasons why insiders may sell company stock, and it’s important to understand the reasons for these sales before letting them impact your own decisions. According to a study conducted by the University of Oulu in Finland, the most common reason an insider may sell shares is diversification. When an insider’s net worth becomes overly concentrated in company stock, it may be time to trim. The Oulu study also found that insiders with highly concentrated portfolios “have a higher propensity to sell their insider stocks” and “sell in larger trade sizes than insiders with less unbalanced portfolios.”

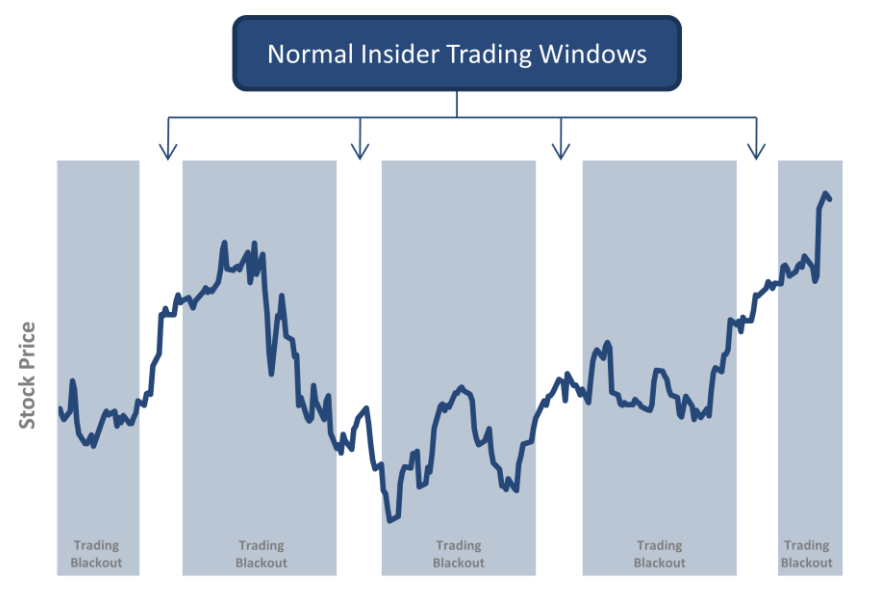

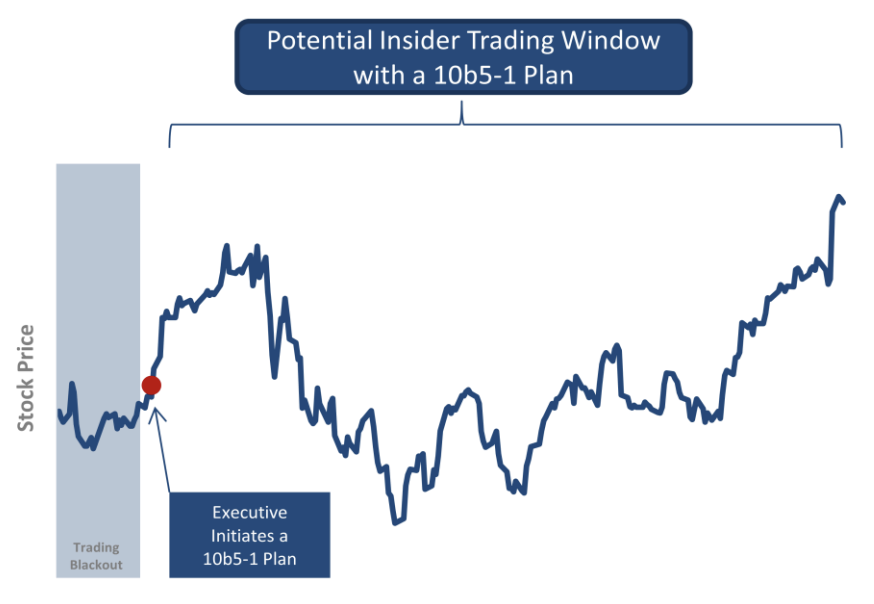

Other reasons for selling stock may include tax planning or personal financial reasons. Even executives and directors need to send their kids to college or take a distracted vacation. Our friends at the Securities and Exchange Commission (SEC) have a nice system to improve transparency for insider sales. If insiders need to sell for one of the above reasons, they can set up pre-planned sales through a 10b5-1 plan. (The SEC sure do love their catchy names, don’t they?) This plan gives an insider the ability to set up a schedule to sell shares regardless of price, at a predetermined time, so as not to cause alarm to shareholders.

A director of XYZ Corporation, for example, may choose to sell 5,000 shares of stock on the second Wednesday of every month. To avoid conflict, Rule 10b5-1 plans must be established when the individual is unaware of any [material non-public information].

–Investopedia

Since the trades are predetermined, insiders can also use a 10b5-1 plan to sell during a normal trading blackout.

So what does this all mean? Speculating about why executives sell shares without knowing their personal circumstances or total net worth seems pointless.

Lockup Periods

There are times, such as after a recent initial public offering (IPO), that insiders are prohibited from selling (or buying) company stock. These are known as “lockup” periods. A lockup period can last any amount of time, but is usually between 90-180 days as detailed in the company’s S-1 filing. After the lockup period ends, insiders can begin selling stock without restrictions. This type of selling is very common, and not usually a cause for concern. A study conducted at the University of Florida found that after a lockup period, company shares typically underperform the market. Those of you who have followed us for a while know that we avoid new IPOs until the dust settles. This helps us avoid new IPO noise, but it also conveniently saves us from any post-lock-up drops. Before worrying about a new influx of insider sales, check to see if there was a lockup period that recently expired.

Interpreting Insider Sales

There are few things to look for when evaluating a particular insider sale. What is the title of, and total number of shares held by the insider? For example, a sale by the CEO carries more weight than a sale by a director since CEOs typically hold a much larger position of company stock than a director. (As of last year, the average company ownership by a CEO in the tech industry is around 20%.) To help eliminate noise, focus on activity from key roles – the CEO, CFO, and Chairman. Pay attention to “cluster trading,” where multiple key roles execute similar trades.

Not all sales are created equal. Another consideration when reviewing an insider sale would be the amount of shares held versus the amount of shares sold. Look at the sale in terms of a percentage. An insider selling 1,000 shares hardly matters if he holds 100,000, for example, since it’s only 1% of his total holdings. However, the same 1,000 share sale could be significant if an insider only owns 10,000 shares, because this is a 10% reduction in shares held.

There are several forms that can be reviewed to determine what type of insider sale has taken place. The forms are as follows:

- Form DEF 14A (Definitive Proxy Statement) is the place to find out how many shares each director and officer owns, as well as anyone who owns more than 5% of a company’s stock.

- Form 3 (Initial Statement of Beneficial Ownership of Securities) is filed by anyone who becomes an insider of a company, and must be filed within 10 days of the insider’s start date.

- Form 4 (Statement of Changes in Beneficial Ownership) details the amount of shares sold, and at what price, by insiders who own more than 10% of a company’s stock.

- Form 5 (Annual Statement of Changes in Beneficial Ownership) is an annual form which details all holdings of an insider.

All of these forms can be found using the SEC’s EDGAR tool, which provides free public access to company information. If you wanted to get all of the details on a particular insider sale, you might, for example, look at the Form 4 to find the total number of shares sold, then compare it to the Form DEF 14A to see what percentage the sale makes up of the insider’s total holdings. From there, you can decide if it’s significant or not. Most of the time, a one-off insider sale is nothing to worry about. However, when multiple insiders begin selling large positions (such as what we saw recently with Xometry), it may be worth taking a closer look.

Above you can see key individuals cluster selling where the amounts being sold represent significant chunks of their overall holdings.

Stock-Based Compensation

You may be wondering why insiders have so much company stock to begin with. Oftentimes, companies will reward executives with stock-based compensation (SBC) as a way of encouraging continued performance, since this kind of compensation is directly tied to the price of the company’s stock. There are 3 main forms of stock-based compensation:

- Stock options. Not unlike the options contracts that Redditors gamble their $1,000 life savings on, these contracts give an employee the right to purchase company stock at a predetermined price during a specific window of time.

- Restricted stock units (RSUs). These are an agreement by the employer to provide company stock to an employee using a vesting schedule, encouraging employee retention.

- Shares. Plain and simple – you work hard, you earn ownership in the company.

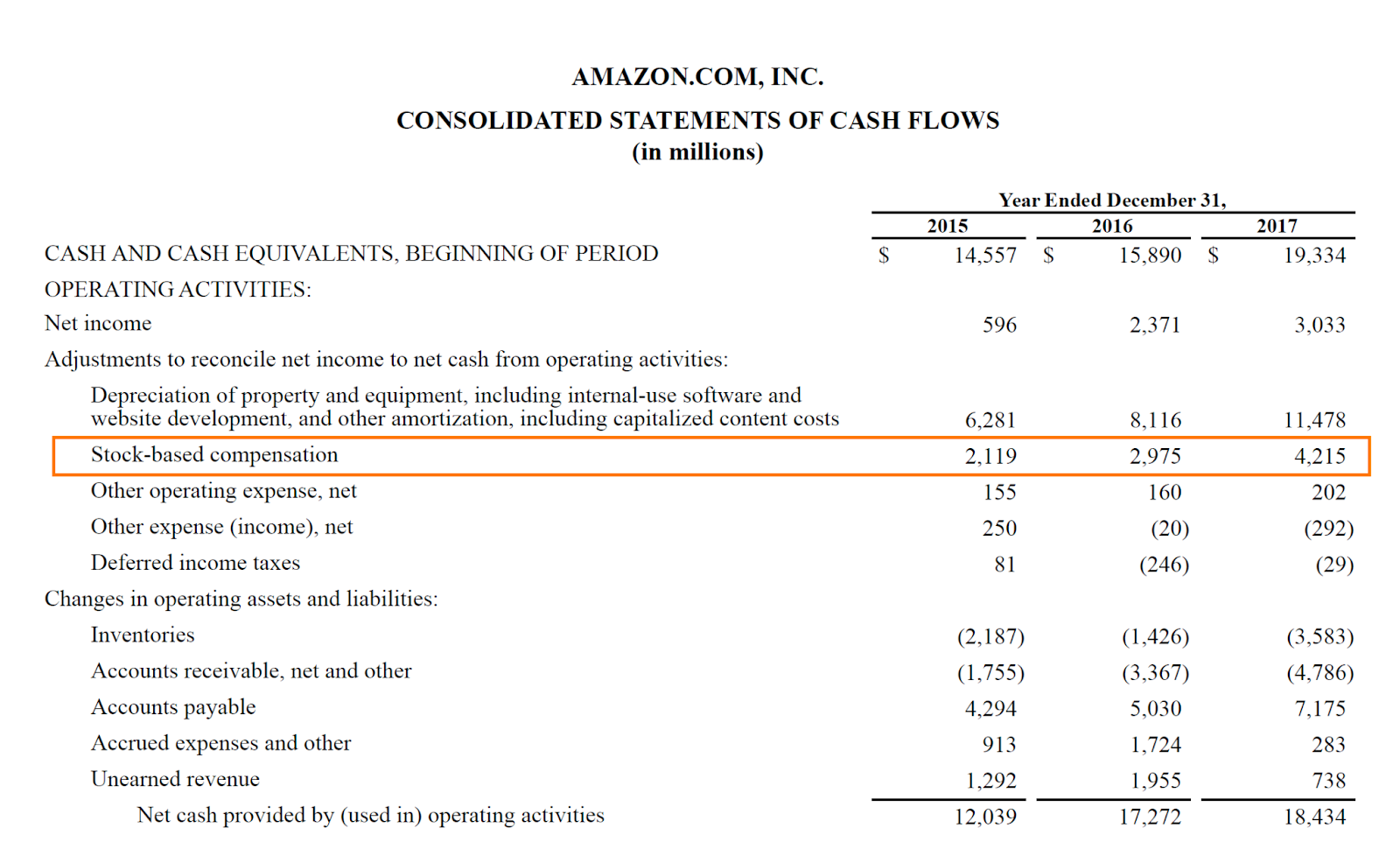

To find out how much a company is paying out in stock-based compensation, head to their investor relations page and pull up their financial statements. Stock-based compensation is a “non-cash expense” and appears on a company’s statement of cash flows. Here is an example of Amazon’s (AMZN) cash flow statement.

Per Harvard Business School, stock-based compensation poses an issue to shareholders in that the shares given to employees have to come from somewhere. So, to compensate employees with shares of company stock, the company will increase the number of shares outstanding. And what does it mean to current shareholders when a company increases the number of shares outstanding? That’s right, little Johnny. Dilution. No loyal shareholder likes to hear that they now own a smaller piece of the pie than they used to. One easy way to monitor this is just by tracking the number of outstanding shares over time.

If you’re worried that a company you’re invested in is giving out too much SBC, you can look at the average level of SBC in the tech industry, which has increased alarmingly in the past couple years. A study published on Barron’s, a popular financial media outlet, reveals that “the average stock-based compensation for the industry rose from just 4.2% of revenue in 2012 to 10.5% in 2020, accelerating to 22.5% in 2021.” The study also found that over a period from 2004 to 2022, the companies with the top 20% most conservative levels of stock-based compensation significantly outperformed the companies with the top 20% most aggressive levels of SBC. We don’t like to put too much faith in past performance, but it’s worth noting that higher levels of stock-based compensation could have the potential to lead to reduced returns.

Our Take On Insider Selling

Our methodology always strives to keep the investing process simple so that it’s accessible to retail investors with no background in investing. Consequently, we believe that minimizing noise helps make the decision process easier. For example, checking in with companies once a year is a great way to cut out noise from quarterly earnings calls. So is not analyzing every insider sale that happens because it can quickly become overwhelming. Here’s a look at the sales from the CEO of Ginkgo Bioworks over the past several months.

This individual received $363.9 million in stock awards for 2021, so it makes sense he’s capturing some of that windfall – $5.973 million in the above transactions alone which are being driven by a 10b5-1 plan. His total holdings have dropped 20% based on the above sales, but consider how that number might increase based on future shares-based compensation. Sure, you can argue that he probably shouldn’t be selling shares of “the next Microsoft” for so “cheap,” and that he lacks confidence that his company will realize the potential he sells investors during every earnings call. Or you can argue that taking a mere $6 million off the table is one of the perks of being a co-founder and CEO of the most exciting synbio company out there. See? It’s complicated.

The biggest problem you’ll face when analyzing insider trading isn’t interpreting the data, it’s aggregating it. A German firm called 2iQ is the leading insider data provider with global coverage of 60,000+ stocks. That’s where institutional investors go to obtain this data, then they use it as a single signal for complex investing models. Most retail investors would be better off ignoring this noise and focusing on the simpler things – survivability factors such as runway and gross margin, revenue growth, SaaS metrics, simple valuation ratio, and overall share count dilution.

Conclusion

Insider selling is never a good sign, but it’s not always a bad one. Just as we wouldn’t blindly follow an analyst’s price target, or a stock-picker’s recommendation, we shouldn’t blindly follow insider buys and sales. Rather, we should use them as a piece of the puzzle when determining what action to take. Next time you see an insider sale, before you panic, look at how much stock-based compensation a company is handing out on their cash flow statement. Look at the size of the sale, and the insider’s total holdings. Is the insider receiving a boatload of SBC and diversifying? Or are they dumping large amounts of shares as a sign of uncertainty in the company? And if you have an easy way to answer those questions, let us know.

Tech investing is extremely risky. Minimize your risk with our stock research, investment tools, and portfolios, and find out which tech stocks you should avoid. Become a Nanalyze Premium member and find out today!

")

{kind=link}