Klaus Vedfelt/DigitalVision via Getty Images

The RIVN Investment Thesis Remains Highly Speculative

We are skeptical about Rivian Automotive’s (NASDAQ:RIVN) execution in the near term, attributed to its goal of producing 50K vehicles in 2023 (+105.5% YoY). For now, it only produces 9.39K EVs in FQ1’23 (-6.5% QoQ/ +268.2% YoY) while delivering 7.94K (-1.3% QoQ/ +550.8% YoY), otherwise an annualized production sum of 37.56K (+54.3% YoY).

While the quarterly gap between production and delivery numbers is commonly reported, attributed to the timing lag of consumers’ receipts, we are starting to observe a widening gap between capacity and demand. For example, based on the automaker’s FY2022 and FQ1’23 production/ delivery numbers, 5.45K vehicles are still undelivered thus far.

A similar trend is reflected on RIVN’s balance sheet, with growing inventories of $1.82B in the latest quarter (+35.8% QoQ/ +269% YoY), while inventory write-downs and losses on firm purchase commitments have also increased to $229M at the same time (+2.2% QoQ/ +21.8% YoY).

As a result, even if the automaker meets its ambitious production target for the fiscal year, attributed to its backlog still extending through 2024, it is uncertain if consumer demand remains robust, especially due to its hefty price tag of over $73K for R1T pick-up trucks and $78K for R1S SUVs.

This means that only RIVN’s most basic models qualify under the IRA EV $7.5K tax credit, with a cut-off point of $80K for both trucks and SUVs. This may trigger further headwinds to its sales, as competitors such as Ford (F) and Tesla (TSLA) continue the aggressive price war to boost delivery volumes.

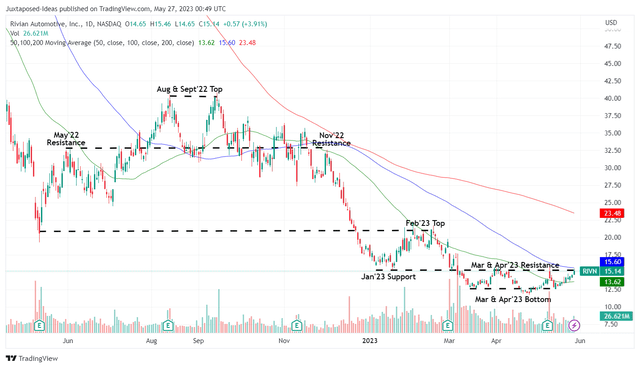

RIVN 1Y Stock Price

TradingView

The same pessimism has been embedded in RIVN’s stock prices, with it already drastically declining by -60.47% since its September 2022 top or by -19.89% YTD. Then again, here is where the stock appears interesting, attributed to a few positive developments.

Firstly, its gross margins have gradually improved to -80.9% by FQ1’23 (+69.9 points QoQ/ +447.5 YoY), with its operating expenses similarly moderating to $898M (+12.9% QoQ/ -16.6% YoY). Combined with the modest capital expenditure guidance of $2B for FY2023 (+47% YoY) attributed to the Enduro ramp-up, we may see the automaker’s cash burn decelerate ahead.

Secondly, RIVN has made the strategic choice to replace the previously outsourced Bosch motors with its in-house Enduro motors from FQ2’23 onwards, allowing it to improve its cost efficiencies while enhancing supply chains. This is on top of the supposedly improved energy efficiency and increased drive range.

The vertical integration may then aid the automaker in narrowing its losses through a more efficient COGS, while allowing it to offer lower-priced R1 variants moving forward. This cadence may enable it to penetrate the lower-to-mid-range market, expanding its audience at a time when EV competition is growingly intense.

It also made the switch from NCA to LFP chemistry battery packs, which are reportedly 20% cheaper to produce. While the transition is still ongoing, RIVN has already reported narrowing losses of approximately -$75K per vehicle in FQ1’23, compared to -$95K in FQ4’22, as highlighted in the recent FQ1’23 earnings call:

Question By Rod Lache

So broad strokes, would you say that on the gross profit line and a clean run rate was a bit over $600 million loss on 8,000 units delivered versus $760 million or so on kind of similar delivery volume last quarter…

Answer By Claire McDonough

Rod, that’s correct. That’s the run rate that we’re working on. As I mentioned in my prepared remarks on the Q1 walk from current Q1 gross profit, excluding the impact of LCNRV to where we expect to be in Q4 of 2024. And as you rightfully noted, we saw a 17% improvement quarter-over-quarter as we went from Q4 to Q1. (Seeking Alpha)

Thirdly, RIVN’s balance sheet appears healthy as well, at $11.24B of cash/ short-term investments (-2.7% QoQ/ -31.5% YoY), with moderate growth in long-term debts to $2.71B (+120% QoQ/ YoY) attributed to the 2029 Green Convertible Notes.

While the latter has also triggered a higher annualized interest expense of $152M (+15.1% QoQ/ +72.7% YoY), we are not overly worried for now, since the elevated interest rate environment is only temporary, likely lifting by 2025, if not 2024. We suppose this cadence may further support the automaker’s goal of funding its operations through 2025.

Lastly, RIVN continues to iterate its ambitious goal of “approximately 25% gross margin target, high teens EBITDA margin target, and approximately 10% free cash flow margin target.” While the feat may not occur over the next few years, we think it is important to have a long-term goal, with the management already aiming to achieve positive gross margins by FY2024.

Combined with the post-March 1 orders likely to trigger improved Average Selling Prices, we are optimistic that the automaker may achieve its FY2024 goal after all, with the management already looking to negotiate its supplier contract rates as of May 2023.

As a result, we are cautiously rating the RIVN stock as a speculative Buy here, with the caveat that the portfolio must be sized appropriately in the event of capital losses. Otherwise, bottom-fishing investors may still wait a little longer for the May 2023 bottom of $12, since the macroeconomic outlook remains uncertain over the next few quarters, with the automaker likely to be EPS unprofitable through FY2027.

This autumn 2025 Earnings Name Transcript")

Q1 2023 Earnings Call Transcript")

{kind=link}