akinbostanci/iStock Unreleased through Getty Photographs

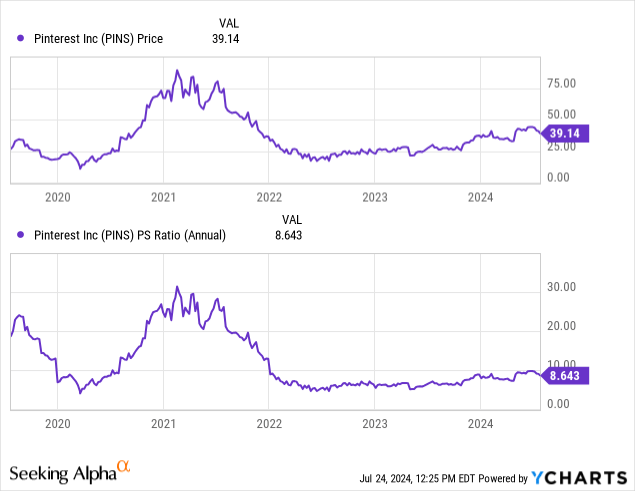

Pinterest (NYSE:PINS) has carried out nicely for shareholders previously yr with a 40% enhance. As we will see above, since 2022, Pinterest has seen its P/S a number of under 10, and at the moment sits round an inexpensive 8, with an estimated gross sales development of 20% or a P/S development ratio of 0.4, just about according to comparable social media platforms like Reddit (RDDT) and Snapchat (SNAP).

Pinterest stories on 7/30 with consensus analyst estimates of $0.28 EPS (32% increased YoY) and $848Mn revenues (20% increased YoY). Within the final 4 years, Pinterest has overwhelmed EPS estimates in 15 out of 16 quarters and income estimates 13/16 quarters. Fairly good at sandbagging! Administration guided to $835Mn to $850Mn in revenues.

Administration additionally guided to EBITDA margins being increased than final yr (22%) for the total yr, throughout its name.

Earnings apart, what are the long-term prospects of Pinterest and the way does it stack up with competitors?

Carving its personal area of interest

I consider Pinterest has held its personal with so many different robust opponents, resembling Fb, TikTok, Reddit (RDDT) and Snapchat (SNAP) as a result of it has a totally totally different focus and area of interest. Theirs’s is a singular and distinct area, in contrast to different social media platforms, which are likely to give attention to leisure, whereas Pinterest zeroes in on ahead industrial intent.

Nearly all of Pinterest customers have an intent to purchase, which is way extra precious to advertisers.

Pinterest has a Zen like high quality about it, visually interesting, much less poisonous and fewer damaging, a targeted goal for its customers, with no strain on the variety of followers or private drama.

As a social media consumer, I see and perceive that whereas social media platforms will overlap, no single platform can fulfill every part, not even the mighty Fb. When platforms like Pinterest have sure talent units, resembling fulfilling thought wants or visually augmenting design concepts, they’re filling a aggressive void. As such, this can be a large aggressive benefit and will stay so, for 2 causes – one is the talent set, the second is the community impact or the flywheel. From Pinterest’s 10K, emphasis mine.

Design and product concepts come from quite a lot of sources together with retailers, manufacturers, creators, publishers and customers. Content material codecs embrace photographs that let you click on into an thought to study extra, movies that present the steps of an thought, and merchandise that manufacturers and retailers add from catalogs.

Our customers typically come to the platform to get inspiration for a lot of of life’s moments, which may result in discovering new merchandise and types. In consequence, industrial content material from manufacturers, retailers and advertisers is central to Pinterest. We consider that in-market shoppers on Pinterest are typically early of their journey towards a purchase order determination and don’t but know precisely what they need to buy. Accordingly, we consider that they’re open to discovering new merchandise and types on Pinterest moderately than merely navigating to manufacturers they already know, as is widespread on conventional search engines like google and yahoo and e-commerce platforms. This creates a singular flywheel the place related advertisements cannot solely improve the consumer expertise, but in addition drive extra worth for advertisers within the type of elevated views, clicks, and conversions.

Ladies comprise 2/3 thirds of Pinterest’s consumer base and Gen Z over 40%; Gen Z can be the quickest rising cohort. Anecdotally, whereas chatting with customers, I learnt most had been blissful going there as a result of it helped them with design concepts and helped them with the method of selecting a number of issues.

Why would the availability facet (manufacturers, retailers, and advertisers), change or flock to Fb, Instagram or TikTok once they have 480Mn Month-to-month Lively Customers finishing the inventive, and monetization course of? Equally, why would customers waste time on Fb, Instagram and TikTok for merchandise they will not discover, which can be found in droves on Pinterest.

I consider this distinctive id and area of interest is a giant aggressive benefit, just like the one Reddit enjoys with its Subreddits, and TikTok enjoys with its influencers. I consider this power will proceed to assist it develop and compel customers to remain loyal.

Monetization Initiatives

Pinterest’s funnel execution needs to be spot on, principally simpler and sooner monetization, which initially it was unable to do with far an excessive amount of wastage on creativity or design assist; merely, there weren’t sufficient deep hyperlinks to promote. With a consumer intending to purchase, they wanted extra direct hyperlinks from sellers.

They began enhancing on this from 2023 and have been executing higher with extra click on throughs served and transformed in Q1-24. 97% of decrease funnel income adopted direct hyperlinks in Q1-2024

Secondly, their API initiative has additionally yielded higher outcomes with API for conversion masking 40% of income in Q1-24. Administration additionally cited that they’ve seen their funds share of sellers, enhance on account of efficiency, with double the variety of clicks in This autumn-23 and Q1-24. This was extra pronounced with bigger and extra refined sellers, who’re measuring efficiency higher.

Whereas Pinterest has third social gathering advertisers resembling Google and Amazon additionally rising income, they had been extra impressed with their very own direct initiatives in contributing to income development in Q1-24.

Good monetary efficiency previously 6 years

Pinterest Financials (Pinterest, Looking for Alpha, Fountainhead)

Pinterest has grown at an excellent income CAGR of 36% from a paltry $473Mn in 2017 to a excessive $3Bn enterprise final yr with 480 Month-to-month Lively Customers. Money Stream was additionally robust for the final three years, with margins of 29, 17 and 20%.

Weaknesses

Focus

Pinterest is concentrated in two areas – CPG (Shopper Packaged Items) and Retail, which may very well be a dampener to development.

Stalling development and poor ARPUs

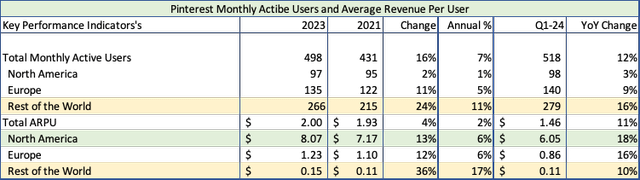

US Month-to-month Lively Customers had stalled at 97Mn customers in 2023, it was 95Mn in 2021, barely rising to 98Mn in Q1-24.

Europe had grown from 122Mn to 135Mn in 2023 a 5% annual development, which elevated to 9% development in Q1-24.

However the one actual development within the final 2 years has come from the Remainder of the World from 215 to 266, an 11% annual enhance additional rising by 16% YoY in Q1-24.

We will see that within the ARPUs as nicely, annualized will increase had been 6% every for North America and Europe, whereas ARPU for the remainder of the world jumped 17%. In Q1-24, Pinterest had a significantly better YoY development fee with North America and Europe outpacing the remainder of the world at 18% and 16% in comparison with 10%.

Nevertheless, the Remainder of the World’s ARPU was a measly 15 cents in comparison with $1.23 for Europe and $8.07 for North America, which implies total ARPU is not going to enhance simply and will likely be weighed down with decrease ARPU’s from the remainder of the world.

Pinterest KPIs (Pinterest, Fountainhead)

I had highlighted the identical downside of decrease ARPUs and weak spot of smaller gamers preventing for scraps in my Reddit article. Reddit’s US ARPU is simply $4.8, Snapchat’s is $8.96, whereas Fb’s is $68.4. This side of the social media business does not augur nicely for smaller gamers like Pinterest.

No Pricing Energy

In 2023, even because the variety of advertisements elevated by 31%, the value per advert dropped as a lot as 17%. Equally, in Q1-24 the variety of advertisements served elevated by a whopping 38%, however costs dropped 11%.

Valuation – Recommending a purchase

Q2-2024 outcomes are anticipated on July thirtieth and there are a number of key elements to look out for.

- Administration was very clear to not anticipate hockey stick moments for any quarter; they consider that the measures for better conversion resembling elevated use of APIs and direct hyperlink seize function with a lag. As I discussed earlier, some initiatives began in This autumn-23 began accelerating in Q1-24 and these will proceed in Q2-24 as nicely.

- Improve in vendor’s funds share, which comes solely on account of efficiency. That also needs to present up in Q2 earnings and be scrutinized totally.

- Administration guided to raised adjusted EBITDA margin for 2024, which was 22% for the entire yr of 2023. When questioned about AI and R&D spend, like everybody else, they too are spending on it, and have cautioned to anticipate headcount will increase. A couple of days again, Alphabet (GOOG) obtained burnt for not displaying sufficient AI income and even AI associated income. I’m a long-term investor, and I can perceive that you simply can not produce monetizable AI with out spending on it, however who is aware of how impatient merchants may be if bills change into increased?

Pinterest Forecast (Pinterest, Looking for Alpha, Fountainhead)

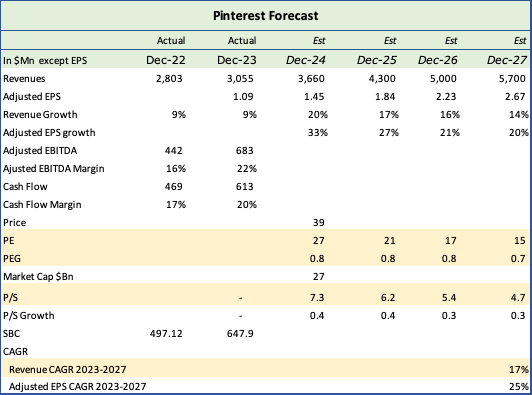

I anticipate Pinterest to develop income at a CAGR of 17% from 2023 to 2027, with leap of 20% in 2024, regularly rising at 17-14% within the subsequent three years, fueled by a gradual enhance in direct hyperlink gross sales and conversions. The margins are fairly spectacular with money movement at 20%, and adjusted EBITDA at 22%. As margins enhance, EPS is slated to develop a lot sooner from $1.09 in 2023 to $2.67, or over 25% a yr, this isn’t only a gross sales development story and I might have hesitated to purchase only a 17% grower at 7x gross sales, however nice money movement and earnings undoubtedly tilted it in the direction of a purchase.

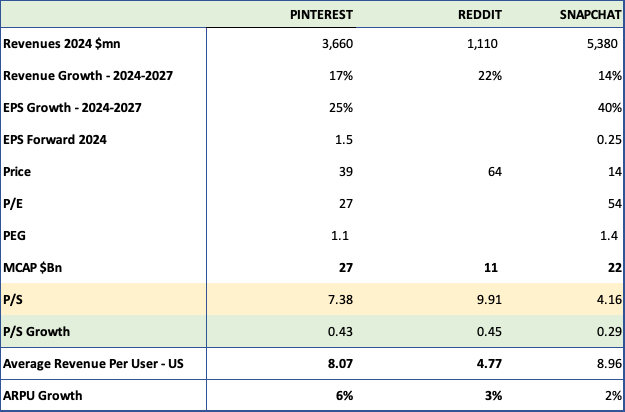

Pinterest stacks up nicely in comparison with Snapchat and Reddit. Whereas Reddit grows revenues sooner at 22%, it has no income to talk of, and a a lot decrease ARPU and development, however is priced comparable at a P/S development of 0.45 to Pinterest’s 0.43

Snapchat, alternatively, is rising revenues slower at 14%, and priced decrease at a P/S development of 0.29.

Pinterest opponents (Pinterest, Looking for Alpha, Fountainhead, Snapchat, Reddit)

Greater than the numbers, I like…

- The distinctive web site and platform with its area of interest of serving to patrons with concepts and design.

- The intent to purchase precious consumer base.

- The flywheel, which no different platform can simply replicate.

- The drive towards higher monetization.

These are all huge pluses, making it GARP (Development at A Cheap Value) story. I am placing in an order to purchase.

")

")

{kind=link}