Marko Geber

We have previously covered Nvidia’s (NASDAQ:NVDA) here as a post-FQ2’23-earnings article in September 2022. At that time, the US government’s new restrictions may cause the company to lose a significant $400M in sales derived from China, assuming delays in licensing approval for its accelerators and data center-related chips. Combined with the multiple headwinds of its PC destruction, lowered forward guidance, and the Fed’s aggressive rate hikes through 2023, we had projected that the stock may be decimated with little catalysts for short-term recovery. True enough, the stock hit a bottom at $108.13 by mid-October 2022.

For this article, we will be focusing on NVDA’s massive tailwind for recovery through China’s reopening cadence and approval of foreign/domestic games. Therefore, its GPU and cloud gaming products may see increased domestic demand, potentially boosting its financial performance. The company’s GeForce Now AAA cloud games will also be offered in select vehicles under partner automakers, such as Hyundai, Polestar, and BYD, proving its ambition in providing bundled services. Lastly, by diversifying into the IoT and Automotive markets, the management expands its strategic exposure to many end markets, supporting its premium valuations indeed.

The GPU & Cloud Gaming Investment Thesis

The macroeconomic outlook remains uncertain through 2023, due to the rising inflationary pressure impacting global discretionary spending. The US consumer index for computers has been declining by -4.4% YoY and -2.7% sequentially by November 2022, with the Information technology commodities plunging drastically by -11.5% YoY and -1.8% sequentially. Will things lift in the intermediate term? Market analysts think so, due to NVDA’s projected revenue CAGR of 10.1%, EPS of 8.6%, and Free Cash Flow generation of 17.1% through FY2025 (the equivalent of CY2024).

On the other hand, we are more bullish since the next cycle for GPU and PC replacements will be sometime in 2024. This is attributed to the hyper-pandemic demand for corporate and personal devices in 2020, when NVDA recorded a massive YoY jump in revenue at 52.7%, Intel (INTC) at 8.2%, and Microsoft (MSFT) at 14.18%. Furthermore, with an average product replacement cycle of GPUs for five years and PC CPUs for six years, NVDA’s projected top and bottom line growth in 2024 may naturally be revised upward.

In addition, the Fed’s recent meeting minutes suggest that interest rate cuts may occur from 2024 onwards, suggesting a notable deceleration in inflation rates then. With the improvement in macroeconomics, we may see global consumer demand returning, triggering the uplifting of market sentiments as well.

We may also see a healthy rebound for GPU and gaming products in the short term, attributed to China’s reopening cadence. After three years of continuous lockdowns, market analysts project a flurry of ‘revenge’ spending, significantly aided by the rapid loosening of gaming regulations in the country after 18 months of restrictions. The National Press and Publication Administration, China’s video game regulator, has finally granted publishing licenses to 44 foreign games on 29 December 2022, on top of the 468 domestic games for the whole year. This marks a significant reversal in the government’s stance, which has not approved of any foreign games since the start of the crackdown, against the 180 in 2019.

NVDA notably commanded 88% of the world’s discrete GPU sold by Q3’22. Since China’s domestic offerings fall short of the company’s products, it is unsurprising that NVDA’s PC/ gaming chips remain highly popular amongst Chinese consumers. In addition, China (including Hong Kong and Taiwan) accounted for 58.1% of the company’s revenue in 2022 and 52.7% in 2019. As a result, the stock has recovered moderately by 13.3% with the recent game approvals, aided by the release of a trade-compliant A800 GPU in November 2022. Jensen Huang, CEO of NVDA, said:

So our expectation is that for the US and also for China, we will have a large number of products that are architecturally compatible, that are within the limits and that require no license at all. (Tech Wire Asia)

China remains a significant player in the global games market, with over 685M gamers comprising nearly half of the country’s population. Its domestic gaming revenue growth has unfortunately declined by -5.4% YoY to $43.5B in 2022, due to strict gaming regulations. However, things may rapidly rebound, with the market expected to reach $50.78B by 2023, attributed to the massive pent-up demand and new game approvals. In comparison, the US gaming market is valued at $90.13B in 2022, suggesting its leading position globally.

In addition, NVDA partnered with Tencent Games (OTCPK:TCEHY), a Chinese entertainment giant with up to 54% of the domestic gaming market share in 2022, to develop the START cloud gaming infrastructure and joint gaming innovation lab in 2019. New AI applications will be explored for game developments, game engine optimizations, and new lighting techniques, highly dependent on the former’s leading GPU technology.

This also builds upon NVDA’s leading cloud gaming service, GeForce Now, which features premium subscription services of up to $19.99 per month or $99.99 for six months. With more than 1.5K game titles in its library, including top games from Ubisoft, Epic Games, and Electronic Arts, it is no wonder that the company has established itself as one of the global gaming leaders.

In the meantime, NVDA continued to report decent growth in the data center segment at 0.7% QoQ and 30.6% YoY in the latest quarter. Notably, the company recorded impressive automotive pipeline wins of over $11B in FQ2’23 for the next six years, increasing by 37.5% YoY.

This is significantly aided by NVDA’s partnership with BYD (OTCPK:BYDDF), which is expected to produce 1.78M vehicles in 2022, with an impressive planned capacity of up to 4M by 2024. Combined with the future launch of its GeForce Now cloud gaming in partner automakers such as Hyundai (OTCPK:HYMTF), Polestar (PSNY), and BYD, there is no doubt that the company is committed to maintaining its leadership in the GPU and cloud gaming market indeed. Danny Shapiro, Automotive VP in NVDA, said:

The ability to stream these popular titles from gamers’ libraries, along with dozens of free games, will bring the in-vehicle infotainment experience to new heights. These are the first automakers to offer NVIDIA cloud gaming in their cars. With accelerated computing, AI and cloud streaming, we’re delivering new levels of vehicle automation, safety, convenience, and enjoyment to the car. (Tech Wire Asia)

Due to the outlier nature of the past three pandemic years, it is unrealistic to expect that NVDA will record similar outsized growth in the coming years. Nonetheless, due to its strategic diversification, the company may continue growing its top and bottom line excellently. The global EV and industrial IoT market are expected to grow to $1.1T and $1.74T in value by 2030, at a CAGR of 22.5% and 20.47%, respectively. While the competition for IoT end markets remains intense with many players, such as Qualcomm (QCOM), ON Semiconductor (ON), MediaTek (OTCPK:MDTKF), Texas Instruments (TXN), and STMicroelectronics (STM), the market is inherently large enough to accommodate multiple players.

Due to these measures, NVDA may be able to mitigate its strategic exposure to future demand destructions, preventing a similar impact on the PC end market witnessed in 2022.

The Premium Investment Thesis

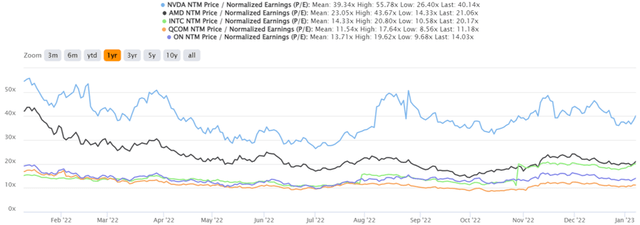

NVDA, AMD, INTC, QCOM, 1Y P/E Valuations

S&P Capital IQ

Now, does this mean that NVDA deserves its premium valuation? In some way, it may be hard to justify P/E valuations of 40.14x, due to the supposed 70% chance of a recession in 2023. The stock also trades with immense baked-in premiums, compared to its peers such as Advanced Micro Devices (AMD), INTC, QCOM, and finally, ON.

These stocks are relevant indeed, since NVDA competes with AMD on AI/data center/ GPU chips, INTC on AI/data center/GPU chips, and QCOM on automotive chips/ Advanced Driver Assistance Systems [ADAS]. While NVDA may not share similarities with ON, the latter’s focus on automotive/renewable Silicon Carbide chips suggest its dominant position in a non-direct industry.

Notably, NVDA trades nearly double AMD’s and INTC’s valuations at NTM P/E of 21.06x and 20.17x, respectively. Despite QCOM’s stellar automotive pipeline wins of over $30B, growing aggressively by $11B QoQ/ $20B YoY, and ON’s growth in the automotive/ renewable/ industrial long-term supply agreements by $5.3B QoQ to $14.1B, NVDA also trades nearly triple both.

In our opinion, the reason is simple. Due to intense competition and massive R&D efforts associated with cutting-edge digital chips, it is naturally difficult to determine which company offers the best chips for each category. However, it cannot be denied that NVDA has its finger in all of these pies, with a sustained focus on innovation towards the data centers, AI, IoT, gaming, and automotive end-markets. This is attributed to the elevated R&D expenses of $6.85B, the equivalent of 23.9% of its revenues over the last twelve months, despite the short-term impact of PC decline. Due to this reason, we reckon that a certain premium is justified.

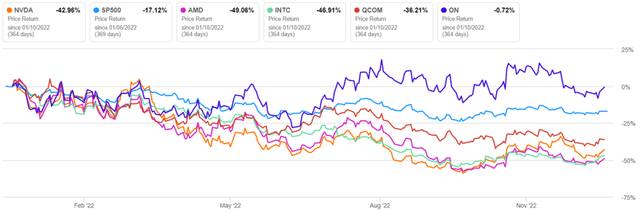

NVDA 1Y Stock Price

Seeking Alpha

On the other hand, the complex yardstick and the ever-changing market offerings make it almost impossible for anyone to determine the exact P/E valuation that NVDA deserves. The ratio has obviously been impacted by the pessimism in the stock market as well. Therefore, we must highlight that NVDA remains a speculative play, only suitable for investors with high conviction.

Naturally, we commend anyone who had been opportunistic enough to load up at the recent rock-bottom P/E levels of 32.50x or low entry point of $112.27 in October 2022. That would have provided many long-term investors with the rare chance to dollar cost average from the hyper-pandemic levels.

So, Is NVDA Stock A Buy, Sell, or Hold?

Based on NVDA’s projected FY2025 EPS of $5.69 and NTM P/E of 40.14x, we are looking at an aggressive price target of $228.39. This number mirrors the consensus estimate’s target of $207.29 as well, suggesting an excellent 32.64% upside potential from current levels.

The question would be whether it is still wise to add at current levels, since the NVDA stock has also recorded a tremendous rally of 39.2% since mid-October 2022. It really depends on individual investors’ risk tolerance and investing trajectory.

We choose to continue rating the NVDA stock as a buy here, with the caveat that it should consequently match or reduce the investor’s dollar cost average. By doing so, the portfolio would be less exposed to short-term macroeconomic uncertainties. On the other hand, bottom-fishing investors may opt to wait for another low $100s entry point, since it is still early in the year. It is not necessary to chase the rally.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

")

")

{kind=link}