They say you should never talk about money with people who have much more or much less than you. Traveling in emerging market countries will quickly make you see how important that rule becomes when negotiating prices. Similarly, when you analyze a firm that’s providing financial services in emerging markets, you need to remove your ethnocentric goggles and try to understand what’s happening in a world that’s different from the one you’re accustomed to.

Brazilian fintech Nu Holdings (NU) has been raised by our readers numerous times because it’s a compelling thesis that’s easy to digest. The Latin American fintech opportunity is massive – perhaps in the range of several hundred billion dollars – and the leader in this space right now appears to be the largest digital bank on the planet – Nubank. As we discovered with other large fintechs like SoFi, it’s a chore to figure out where the revenues come from.

How Does Nubank Make Money?

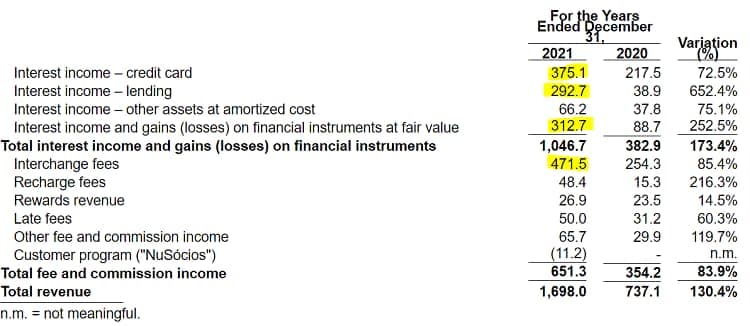

Open the latest earnings deck from Nubank and see if you can figure out how they’re making money. Mention is made of insurance products, credit cards, personal loans, investment products, even crypto, but nowhere in the deck can we quickly glean how this company makes money. After an hour of probing around their collateral, we came across a table on page 212 of the 2021 annual report that shows us where the money comes from.

The four revenue streams highlighted above in yellow account for 85% of the company’s 2021 revenues.

- Interest income from credit cards – 22%

- Interest income from personal loans – 17%

- Interest earned on assets – 18%

- Interchange fees – 28%

The largest of the lot – and the most desirable – would be interchange fees that come from Nubank customers using their credit cards to make purchases. The latest earnings deck tells us 95% of these customers are located in Brazil, 4% in Mexico, and less than 1% in Colombia. If we use this as a proxy for international revenue diversification, Nubank is still heavily dependent on a single country – Brazil – for their fortunes.

When evaluating how these four revenue streams might be impacted by external forces, interchange fees seem the most stable. Consumer spending might flatline or decline a bit, or the interchange fee structure could shift a bit, but this seems to be the most stable and predictable element of their business model. Contrast this to lending which becomes a bit trickier.

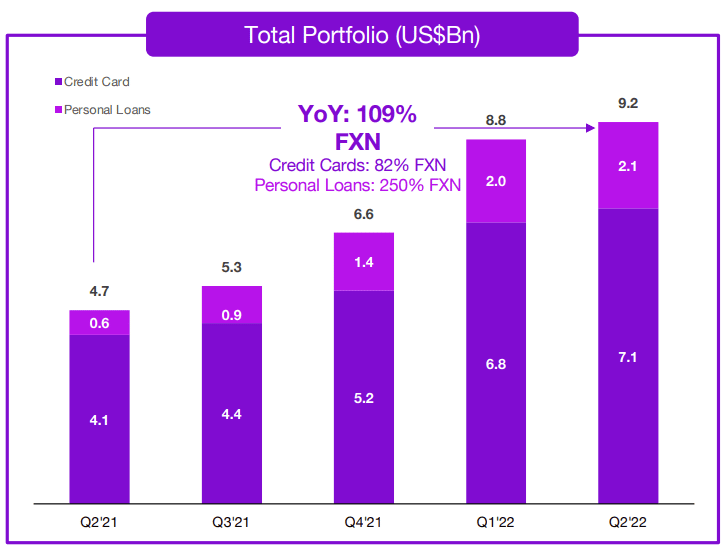

Nubank Personal Loans and Credit Cards

Interest income coming from personal loans and credit cards constituted nearly 40% of 2021 revenues for Nubank with personal loans growing at over 600% year-over-year. Hopefully, they’re being selective with who they lend money to, something StoneCo found out the hard way when their loan portfolio imploded.

To help investors better navigate Nubank, we’ll use their latest earnings deck – Q2-2022 – and point to the relevant slides used to monitor loans and credit card debt outstanding. Page 14 of the deck contains the below chart showing the outstanding balance of credit card receivables and personal loans.

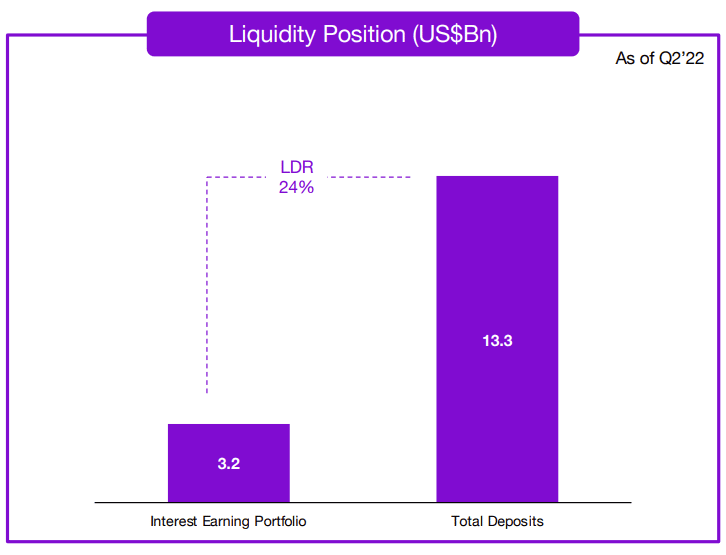

The credit card receivables seen above are not all interest bearing, and the actual number can be found on page 30 of the deck – what they call their “interest earning portfolio” – in a chart that shows the loan to deposit ratio (LDR) which Nubank expects to always be above 14%.

In addition to making sure that deposits keep growing to match the growth in lending, investors also need to watch how the interest earning portfolio performs.

We are seeing a significant increase in personal loans driven by customer demand and as more customers become eligible for our personal loan product. Credit card balances are also rising, driven by an increase in PV, primarily as a result of the overall progressive recovery of PV levels as the economic effects arising from COVID-19 gradually subside and we add new customers.

Credit: Nubank

Rising credit card balances hardly seems like a leading indicator of consumer financial health. If you make a personal loan offering available to people, they’re more likely to avail themselves of it. Nubank also expanded the number of ways in which they can monetize their credit card portfolio, which means more things can be financed, and we all just have to hope and pray that Brazilian consumers aren’t overextending themselves.

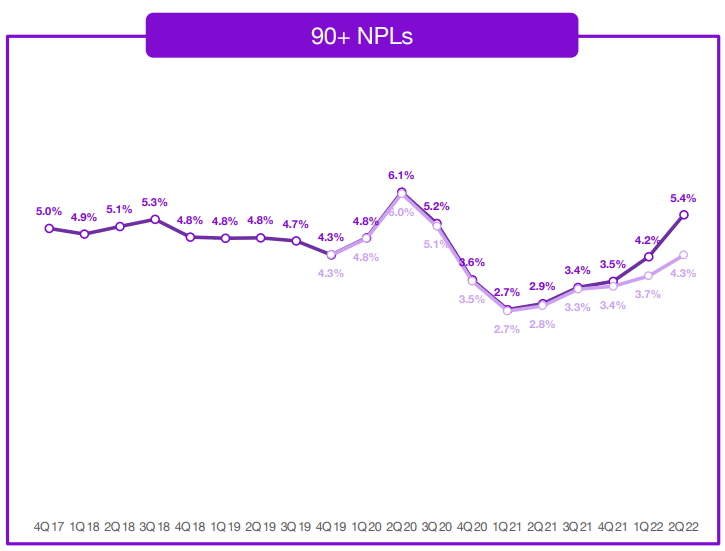

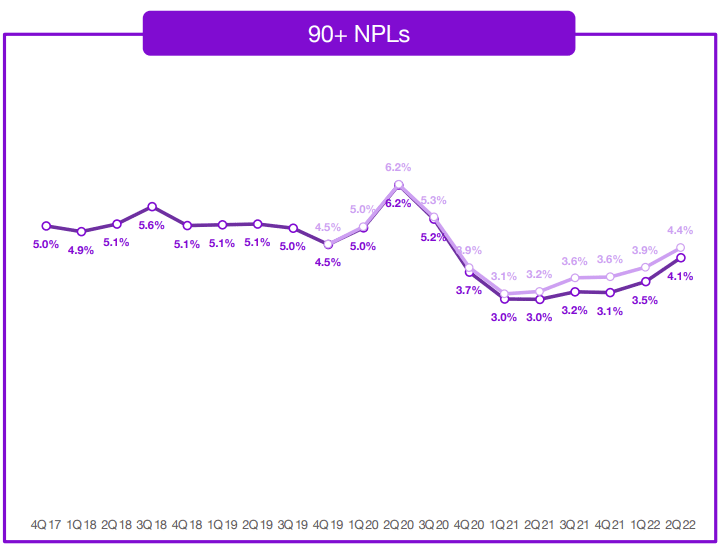

One way to gauge the quality of Nubank’s loan/credit portfolio is by looking at non performing loans (NPLs) as a percentage of total loans. The below chart shows the percentage of NPLs over time (people who have missed a payment for 90 days or more).

The above chart can be found on page 32 of the earnings deck in an appendix. That’s because a recent methodology change by Nubank produces the much nicer chart seen below (page 24 of the deck) which is what you can expect to see going forward.

The methodology change was simply to write off NPLs after 120 days, not 365 days. In other words, get the NPLs off the balance sheet faster and bring the ratio down. It’s a great example of how complexity allows for companies to craft the narrative as the environment changes. Corporations do this all the time, but it becomes difficult to keep track of when you have so many moving parts.

Investors will want to keep a close eye on the NPL metrics because they should provide a leading indicator as to when customers run into problems paying their bills. Inflation has been soaring in Brazil, and people who need to eat won’t hesitate to use debt to put food on the table. That’s even the case in developed markets.

Interest Earned on Assets

The risk-free rate of return is the interest rate an investor can expect to earn on an investment that carries zero risk. “There’s no such thing as an investment with zero risk,” you might say, and you’d be right. Yet for some reason, financiers collectively agreed that a 3-month government Treasury bill is the least risky asset one can own. Therefore, investors can expect to be compensated accordingly.

Investing in a risk-free asset will currently give you around 3% yield. Contrast this to the Brazilian 10-year bond which yields nearly 12% for good reason. Investors are being compensated for the risks they’re taking, Nubank being one of them (our emphasis in bold).

We generate interest income from our interest-earning portfolio and interest on corporate cash, which we invest primarily in government bonds.

Credit: Nubank

This is where things start to get very complicated when we consider the impact of interest rate changes on bond prices, the yield curve, the duration of Nubank’s bond portfolio, and the list goes on. It’s not only an incredibly complex web of interrelated variables, it’s also boring as hell. So, we’ll conclude by saying that in order to understand how interest rates will affect Nubank, you can start with the sensitivity analysis work they’ve presented on page 256 of their annual report and shoot holes in that.

Aping the Oracle of Omaha

There are plenty of reasons to be bullish on the growth of Latin America which attract even the most conservative investors. Retail investors often point to the investments made by Warren Buffet in Latin American (LATAM) fintechs as proof of their prospects but we always need to take institutional investor participation with a grain of salt.

Since Buffett is an active investor, the companies he chooses to hold are solely based on his belief that they stand to appreciate in price. Looking at Berkshire Hathaway’s current holdings, more than 40% of the portfolio consists of Apple shares. Contrast this to his Brazilian fintech holdings – 0.13% in Nubank and 0.03% position in StoneCo. Here’s how this looks in the context of a $100,000 portfolio:

- Nubank: $133.50

- StoneCo: $27.40

Warren Buffet has very insignificant exposure to these two Brazilian fintech stocks, something that needs to be considered when pointing to his vote of confidence. That said, at today’s prices you’re paying less for Nubank shares than what Buffett did, something that may relate to a sale restriction being lifted this past spring which is temporarily depressing the share price. Or it could be that valuation models need to be revisited in the face of Brazil’s surging inflation and higher interest rates.

Valuing Complexity

Unless your day job involves analyzing Brazilian fintech stocks, you’ll be hard-pressed trying to keep track of all the acronyms, charts, buzzwords, and nomenclature Nubank throws at you, all while considering that the truth lies below a deceptive layer of derivatives. Nubank receives interest payments in Brazilian reals, then pays hosting providers in U.S. dollars. It’s critically important to hedge away the risk associated with that volatile currency pair, and such strategies become complex in a hurry. Just days ago, a major U.S. bank regulator warned that the fintech sector has been running amok with many unknown risks and little regulation to keep things under control.

As we learned from the 2008 financial crisis, risks that are unseen have a tendency to grow and later to be the source of nasty surprises.

Michael Hsu, Acting Comptroller of the Currency

Ah yes, big banks are feeling the threat of fintech and are propelling their puppet in the U.S. government to warn everyone, but if you sift through the Nubank 20F or the SoFi 10-K, you’ll start to see his point.

Many investors make the mistake of setting arbitrary price targets based on share price. Some might think five dollars a share for Nubank is a steal, but they may be falling prey to the propensity for retail investors to confuse the price of a share for the value of a share. When setting a price target, always use a valuation ratio instead of a share price. Since growth stocks usually aren’t profitable, we use our simple valuation ratio – market cap divided by annualized revenues. Here’s that number for Nubank:

- 25,042 / (411.57 * 4) = 15

And here’s that number for a handful of fintech firms plucked from our tech stock catalog.

| Asset Name | Nanalyze Valuation Ratio |

| Robinhood | 7 |

| Remitly | 3 |

| Adyen | 7 |

| Block (Square) | 2 |

| PayPal | 4 |

Shares of Nubank would hardly be considered cheap right now, but that’s because investors have strong expectations of future growth. And that’s one thing you cannot argue with. Nubank is growing revenues like mad.

Conclusion

Loads of potential can be realized in LATAM fintech and Nubank is a leader in this space that’s presently expanding into other geographies. Brazilians probably stand the best chance of navigating this space as they possess an active understanding of what’s happening. Financial firms are extraordinarily complex, to begin with, especially fintechs trying to displace banks (think SoFi). Trying to understand complex fintechs in non-native jurisdictions becomes next to impossible. Retail investors of Brazilian descent will be better suited to monitor the health of Nubank’s business. For all others, don’t invest unless you’re willing to put in the time to truly understand what you’re getting into.

Tech investing is extremely risky. Minimize your risk with our stock research, investment tools, and portfolios, and find out which tech stocks you should avoid. Become a Nanalyze Premium member and find out today!

Earnings Preview: Decrease income and earnings anticipated for This fall 2025")

")

{kind=link}