hapabapa/iStock Editorial through Getty Photographs

Everybody who pays consideration to monetary information will pay attention to Netflix’s (NASDAQ:NFLX) large share value decline following the Q1 earnings report on April nineteenth. The reported Q1 EPS was 22% above the consensus anticipated worth. The prevailing narrative is that the decline within the variety of subscribers and predicted additional shrinkage, an sudden state of affairs, triggered the sell-off. The shares fell 35% on the buying and selling day following the report, April twentieth, and are down one other 5% on April twenty first.

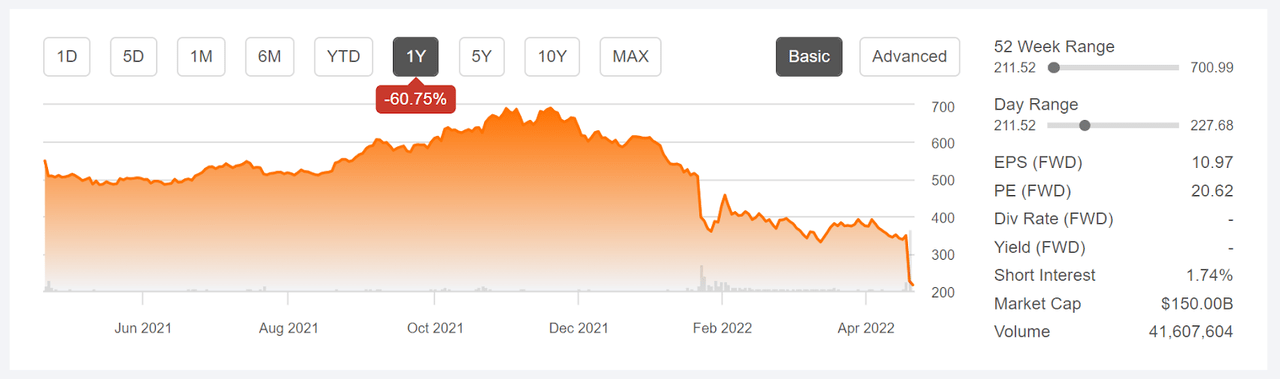

Looking for Alpha

12-Month value historical past and fundamental statistics for NFLX (Supply: Looking for Alpha)

The discount in subscriber numbers is a shock as a result of a lot of the muse for the valuation is on excessive anticipated progress. After the post-earnings collapse, the ahead P/E is 20.6 and the TTM P/E is 21.6, multiples that don’t require a excessive progress price to justify. That is, in reality, a decrease P/E than many utility shares. By the use of instance, Southern Firm (SO) has a ahead P/E of 21.56 and Duke (DUK) has a ahead P/E of 21.13.

The latest decline should be thought-about in a bigger context. NFLX hit a 12-month excessive shut of $691.69 on November 17, 2021 and had fallen 50.4% to shut at $348.61 simply previous to the Q1 report. The present share value is 68.6% under the 12-month excessive shut. After reporting report Q1 EPS for 2021 on April twentieth, the quarterly earnings had been decrease in Q2 and Q3 after which dramatically decrease nonetheless for This autumn. In different phrases, the outcomes by means of a lot of 2021 offered ongoing proof of slowing progress and the worth declined consequently. The outsized drop on April twentieth might sign extra about investor capitulation at an enormous scale than being a rational response to the latest outcomes.

My argument is that Netflix has been struggling over no less than the final 12 months and that there was strong proof of issues with the valuation, however many buyers ignored these information factors. I final wrote about NFLX greater than a yr in the past, on February twenty eighth, after I assigned a promote ranking.

Looking for Alpha

Efficiency of NFLX since my final evaluation on February 28, 2021 (Supply: Looking for Alpha)

Once I wrote this publish, NFLX had missed EPS expectations for the previous 4 quarters and the TTM P/E was 93. The Wall Avenue consensus ranking was bullish and the 12-month consensus value goal was about 15% above the share value at the moment. A major crimson flag was that there was a excessive degree of dispersion among the many particular person analyst value targets, lowering the meaningfulness of the consensus worth. Amongst 31 analysts that ETrade aggregated in calculating the consensus, the best 12-month value goal was $750 and the bottom was $340. As I’ve famous in a lot of my posts, having the best value goal at 2X or larger than the bottom is my rule of thumb for discounting the consensus. Analysis has proven that the consensus value goal has a unfavourable correlation with subsequent efficiency when dispersion is excessive. In different phrases, the Wall Avenue consensus evaluation was sending a bearish sign in February of 2021, although the consensus ranking was bullish and the consensus value goal indicated an anticipated 15% achieve. I didn’t name out this value goal dispersion situation in my February 2021 publish, though I do in lots of different posts.

One other main concern in early 2021, one which carried numerous weight in my evaluation, was that the choices market was sending a strongly bearish sign. In analyzing shares and ETFs, I depend on the market-implied outlook, a statistical forecast of value returns that’s calculated from choices costs and represents the consensus view amongst consumers and sellers of choices.

I assigned a promote ranking to NFLX based mostly on the very excessive valuation, the 4-quarter string of earnings misses, and the bearish market-implied outlook to early 2022. I didn’t cite the excessive dispersion among the many analyst value targets as a priority, however this was additionally a warning signal.

For readers who’re unfamiliar with the market-implied outlook, a short clarification is required. The value of an choice on a inventory displays the market’s consensus estimate of the likelihood that the inventory value will rise above (name choice) or fall under (put choice) a particular degree (the choice strike value) between now and when the choice expires. By analyzing the costs of name and put choices at a spread of strike costs, all with the identical expiration date, it’s attainable to calculate the probabilistic value forecast that reconciles the choices costs. That is the market-implied outlook. For a deeper clarification than is offered right here and within the earlier hyperlink, I like to recommend this glorious monograph revealed by the CFA Institute.

With greater than a yr since my final evaluation, and with NFLX buying and selling at a a lot decrease valuation, I’m revisiting my ranking. I’ve calculated the market-implied outlook by means of the top of 2022 and I evaluate this to the present Wall Avenue consensus outlook, as in my earlier publish.

Wall Avenue Consensus Outlook for NFLX

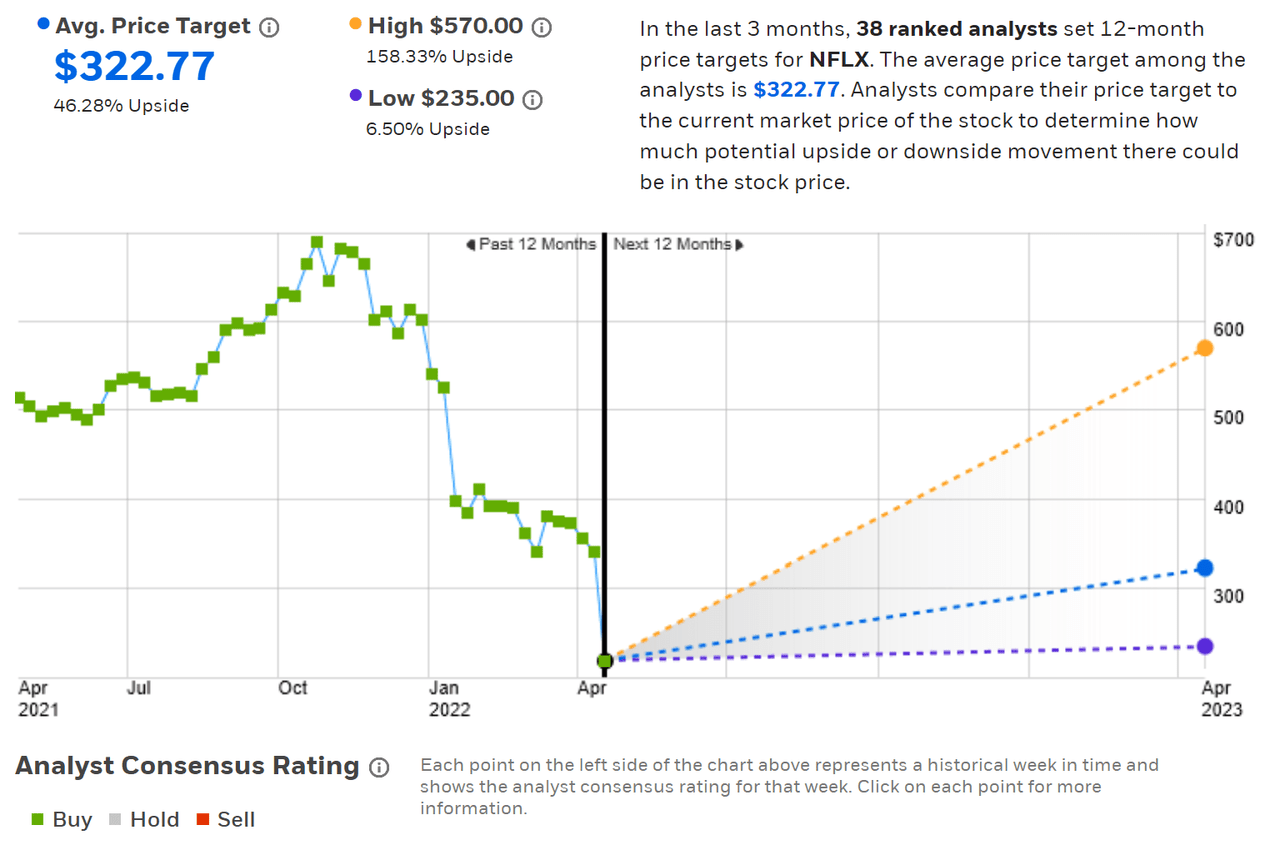

ETrade calculates the Wall Avenue consensus outlook by aggregating the views of 38 ranked analysts who’ve revealed scores and value targets for NFLX over the previous 3 months. The consensus ranking is bullish and the consensus 12-month value goal is 46.3% above the present share value. As in my evaluation final yr, there’s a massive unfold among the many particular person value targets. The best is 2.4X the bottom. The analysis on the predictive worth of the consensus signifies that that is really a bearish outlook due to the excessive dispersion.

ETrade

Wall Avenue consensus ranking and 12-month value goal for NFLX (Supply: ETrade)

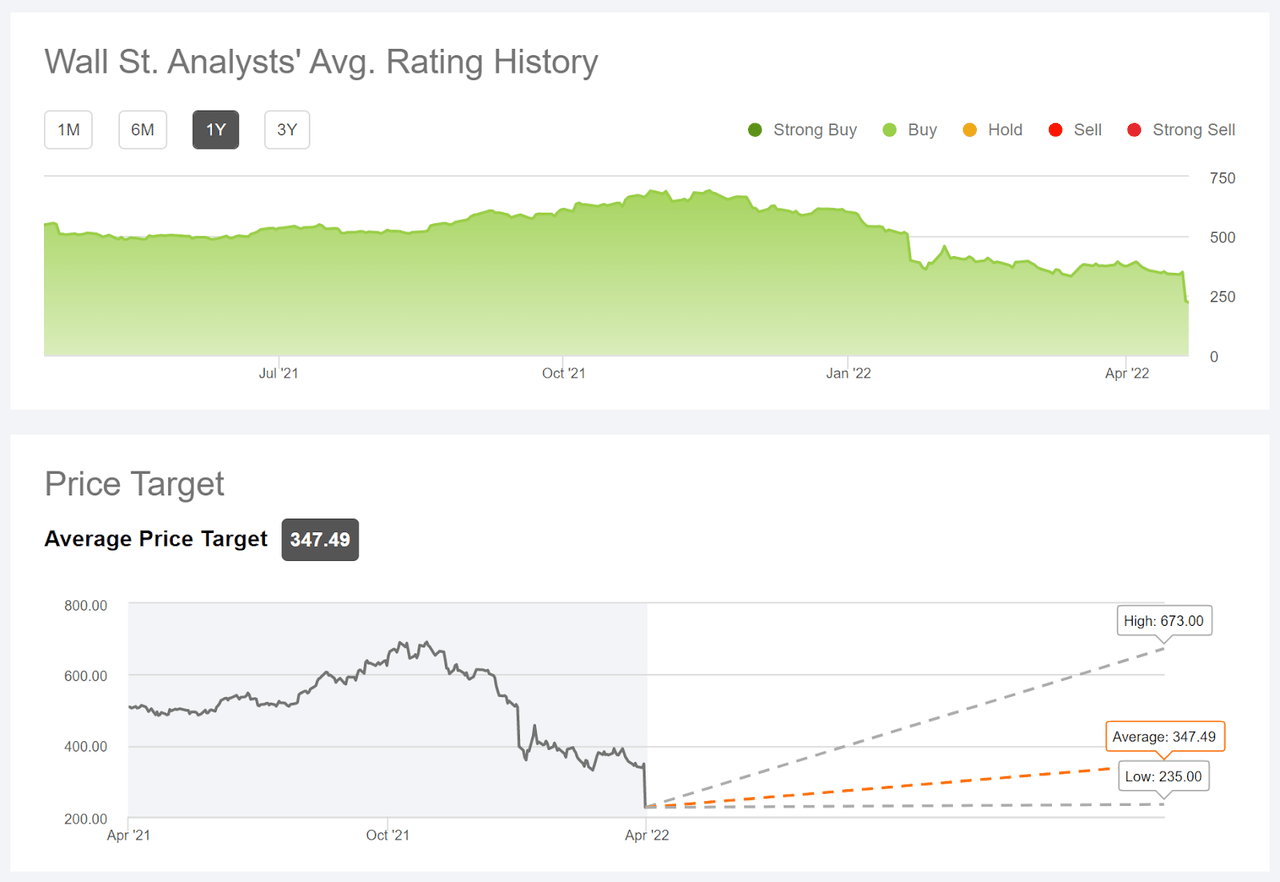

Looking for Alpha calculates the Wall Avenue consensus outlook utilizing scores and value targets issued by 44 analysts who’ve revealed their views over the previous 90 days. The consensus value goal is even larger than ETrade’s and the dispersion among the many particular person value targets can also be larger than in ETrade’s analyst group. Looking for Alpha’s model of the consensus ranking is a maintain / impartial, versus ETrade’s consensus purchase ranking.

Looking for Alpha

Wall Avenue consensus ranking and 12-month value goal for NFLX (Supply: Looking for Alpha)

The Wall Avenue consensus outlooks calculated by ETrade and Looking for Alpha are constant, with consensus 12-month value targets which might be about 50% larger than the present share value and a really excessive degree of dispersion among the many particular person analyst value targets.

Market-Implied Outlook for NFLX

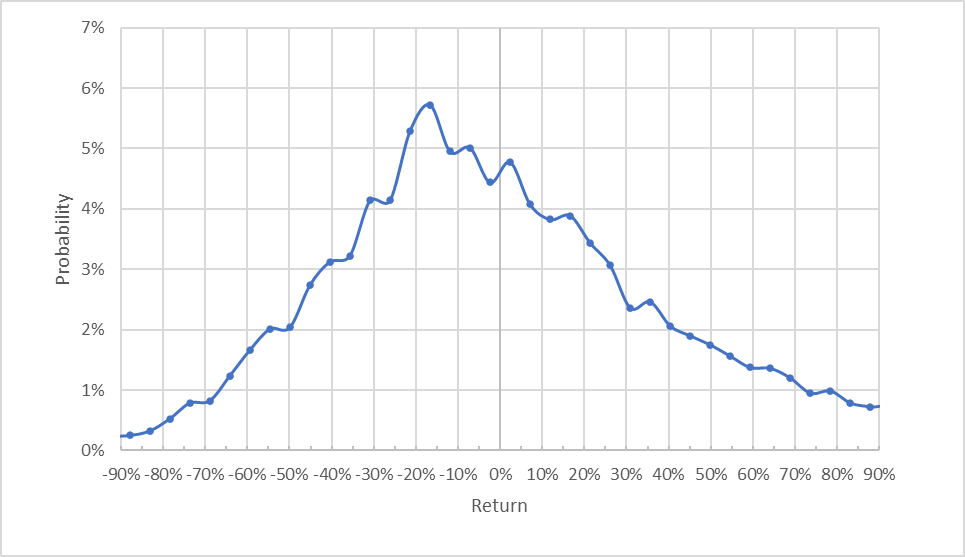

I’ve calculated the market-implied outlook for NFLX for the 9-month interval from now till January 20, 2023, utilizing the costs of name and put choices that expire on this date.

The usual presentation of the market-implied outlook is a likelihood distribution of value return, with likelihood on the vertical axis and return on the horizontal.

Geoff Considine

Market-implied value return possibilities for NFLX for the 9-month interval from now till January 20, 2023 (Supply: Creator’s calculations utilizing choices quotes from ETrade)

The outlook for the subsequent 9 months is considerably tilted to favor unfavourable returns. The utmost likelihood corresponds to a value return of -17% for this era. The anticipated volatility calculated from this outlook is 51% (annualized). For comparability, ETrade calculates 47% implied volatility for the January 20, 2023 choices.

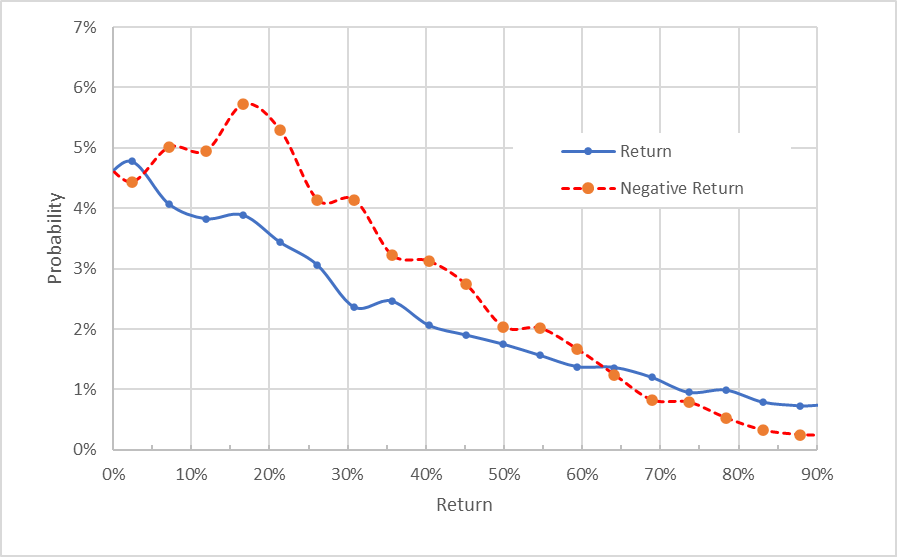

To make it simpler to straight evaluate the chances of constructive and unfavourable returns, I rotate the unfavourable return facet of the distribution concerning the vertical axis (see chart under).

Geoff Considine

Market-implied value return possibilities for NFLX for the 9-month interval from now till January 20, 2023. The unfavourable return facet of the distribution has been rotated concerning the vertical axis (Supply: Creator’s calculations utilizing choices quotes from ETrade)

This view actually illustrates that the chances of unfavourable returns are persistently and considerably larger than the chances of constructive returns of the identical dimension, throughout a variety of probably the most possible outcomes (the dashed crimson line is nicely above the strong blue line over many of the left ⅔ of the chart above). This can be a bearish outlook.

Concept means that the market-implied outlook will are likely to have a unfavourable bias as a result of risk-averse buyers are likely to overpay for draw back safety (put choice), however there isn’t any solution to measure whether or not this bias is current. Contemplating the potential for a unfavourable bias within the broader context of the vary of market-implied outlooks that I’ve calculated doesn’t change my interpretation of this market-implied outlook as considerably bearish.

Abstract

NFLX’s big drop following earnings represents a broad capitulation, as many buyers seem to have misplaced religion within the firm’s trajectory. A variety of indicators have been sending bearish alerts over the previous yr and the inventory’s excessive valuations amplified the impacts of dangerous information. The very excessive dispersion amongst particular person value targets remains to be current. The market-implied outlook continues to be bearish as nicely. Whereas the consensus value goal is round 50% above the present value, the rolling 90-day window that’s sometimes used implies that a few of the value targets had been made previous to the latest information which is, clearly, main many to reevaluate the corporate’s prospects. Towards all of this unfavourable information, after all, the decrease valuation makes the shares significantly extra interesting. I’m altering my ranking on NFLX from bearish/promote to impartial/maintain, although there may be an elevated likelihood of further declines from right here. NFLX is probably not the expansion engine that buyers have come to anticipate, however the firm has a lot to admire.

")

")

CEO Hans Vestberg on Q1 2022 Outcomes – Earnings Name Transcript")

{kind=link}