Lanie Beck, Senior Director of Content & Marketing Research, Northmarq. Image courtesy of Northmarq

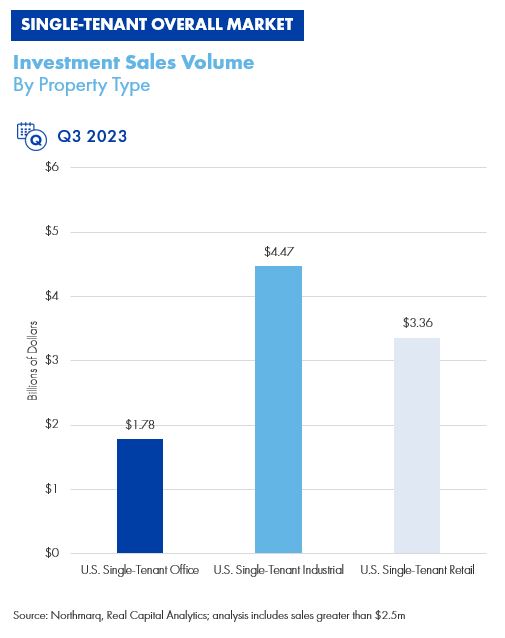

Investment sales for single-tenant retail properties, which saw a third-quarter transaction volume increase of 51.4 percent to a total $3.4 billion, were the bright spot in the net lease market’s third quarter, when single-tenant office and single-tenant industrial both posted sales volume decreases, according to Northmarq.

The Northmarq Q3 2023 Market Snapshot report noted overall single-tenant net lease sales volume has been steadily declining each quarter since reaching an all-time high in the fourth quarter of 2021. Overall volume reached a new recent low of $9.6 billion during the third quarter of 2023, down 9.8 percent from the second quarter and 48.3 percent from the third quarter of 2022.

With only $31.7 billion in sales by the end of the third quarter, the STNL overall market is likely to post its slowest year of activity in over a decade, according to Lanie Beck, Northmarq senior director, content & marketing research. Beck also points to the continuing bid-ask gap that is keeping transaction volumes down as buyers decline to pay what sellers believe their properties are worth.

READ ALSO: Where the Smart Money Is Investing in CRE

Since reaching an all-time high at year-end 2021, quarterly activity has been reduced by more than 78 percent, illustrating just how substantial an impact economic uncertainty can have on the market, Beck said in prepared remarks.

Investment sales volume by property type, quarterly. Chart courtesy of Northmarq

Rising interest rates have sidelined many investors this year, she said. In the past year and a half, the Federal Open Market Committee has raised interest rates 11 times, bringing the key federal funds rate to a target range of 5.25 to 5.5 percent, the highest level in 22 years. While the FOMC kept interest rates steady at its November meeting last week, Federal Reserve Chair Jerome Powell has not ruled out another rate hike in the near future, possibly as soon as the December FOMC meeting, as it continues attempts to curtail inflation.

Noting there was only a total of $9.6 billion in transactions in the net lease sector in the third quarter, Beck said a fourth-quarter rally is unlikely with the threat of another interest rate looming.

In the past 12 months, cap rates in the single-tenant net-lease market have risen by an overall average of 50 basis points. Northmarq states there was another significant jump in the third quarter, with cap rates rising 19 basis points to a new overall average of 6.13 percent. All single-tenant net lease sectors reported cap rate increases in the third quarter, with the retail market the only sector to have a sub-6 percent average cap rate.

Private buyers continue to make most of the investments. During the first nine months of the year, private buyers accounted for 45 percent of the activity. Public REITs and domestic institutional investors followed at 20 percent each.

Retail investments jump

While activity in the single-tenant retail sector is down more than 25 percent year-over-year, it was the only net lease sector to report an investment volume uptick in the third quarter. However, Beck noted the second quarter of 2023 was a particularly slow period for retail transactions.

Investment sales volume by property type, annual. Chart courtesy of Northmarq

She stated the volume was well below the recent average and slightly below volumes reported at the height of the pandemic. Beck projects that once combined with sales levels from earlier in the year, single-tenant retail should be able to post a moderate annual sales volume total. However, she cautions it won’t be anywhere near the activity reported over the past two years.

Looking ahead, Northmarq expects both opportunities and challenges for the single-tenant retail market. New developments are occurring, particularly in quick-service restaurants, free-standing grocery stores and dollar stores. Other sub-sectors that are reporting high levels of new construction include aftermarket auto parts stores, gas stations and convenience stores.

But there have been closing announcements already made this year including among the big three retail pharmacy brands that are expected to close hundreds of stores. Walmart is closing several supercenter and neighborhood market locations and casual dining brand Applebee’s is also closing locations. Going forward, some retailers will take advantage of strong consumer demand while others may not be able to do so.

Industrial, office face challenges

The single-tenant industrial market had $4.5 billion in sales volume in the third quarter, down 23.5 percent from the second quarter and down 51.6 percent year-over-year. With just over $16.2 billion in sales posted year-to-date, the sector may have its slowest year on record in six or more years, according to Northmarq.

Rendering of Intel’s manufacturing plants in Ohio. Image courtesy of Intel Corp.

Despite the slower volume, Beck notes industrial assets are still attractive to investors and lenders and new state-of-the-art facilities are continuing to be built in strategic markets across the country driven by e-commerce, technology and other industries. Among the major investments being made are the $20 billion mega-site in central Ohio being built by Intel and a multistory, 4.1 million-square-foot facility being developed by Amazon in Los Angeles.

Transaction volumes in the single-tenant office market only tallied $1.8 billion during the third quarter, a 31 percent drop from the second quarter and a 63 percent year-over-year decrease. Since fourth-quarter 2021, net lease office sales are down 82 percent.

Northmarq states health care has been an important subset of single-tenant office and has helped boost recent activity. However, investor demand has been more for urgent care centers, dialysis facilities, medical office buildings and other specialty health-care properties and isn’t likely to include traditional office product. Crossover into research and development facilities and lab space is expected to continue.

{kind=link}