JPSchrage/iStock through Getty Photographs

Introduction

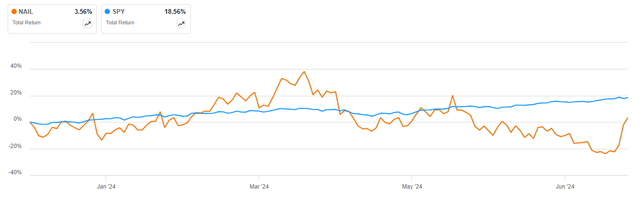

The Direxion Each day Homebuilders & Provides Bull 3X Shares ETF (NYSEARCA:NAIL) has considerably underperformed the SPDR S&P 500 ETF (SPY) up to now in 2024, delivering a 3.5% whole return towards the 18.5% acquire in the benchmark ETF:

NAIL vs SPY in 2024 (In search of Alpha)

Whereas among the underperformance is because of the fairly excessive expense ratio of 0.97%, I nonetheless assume the ETF is sensible for traders with a short-term horizon who wish to profit from the anticipated pivot in FED financial coverage over the following few years. With an undemanding valuation of underlying holdings and the substantial leverage employed by the ETF, traders keen to take the chance could obtain a return within the low-to-mid double digits.

ETF Overview

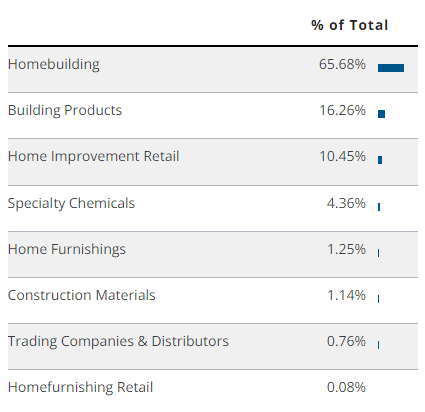

You possibly can entry all related NAIL info on the Direxion web site right here. The ETF seeks to ship 300% of the every day efficiency of the Dow Jones U.S. Choose Dwelling Development index. The portfolio is closely invested in homebuilding shares which account for 65.68% of internet belongings, adopted by constructing merchandise at 16.26% and residential enchancment retail at 10.45%:

Portfolio allocation throughout sectors (Direxion web site (Accessed July 2024))

Giant Holdings and Focus

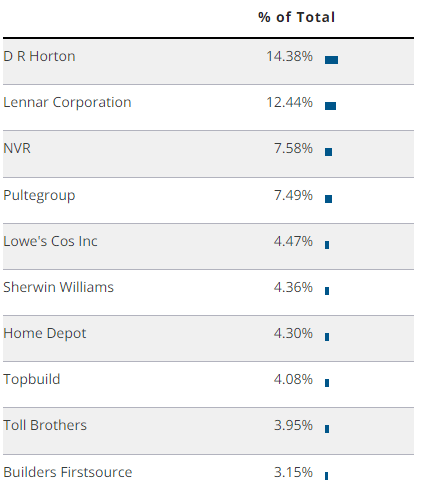

You possibly can entry all NAIL holdings right here. The portfolio consists of 44 separate shares however stays extremely concentrated nonetheless, with the highest ten positions accounting for 66.2% of internet belongings:

Prime ten NAIL positions (Direxion web site (Accessed July 2024))

Portfolio fundamentals

Whereas the expense ratio of 0.97% is sort of excessive for such poor diversification, the concentrated portfolio permits for a greater grasp of underlying holding dynamics and valuation, as proven under:

| Firm | In search of Alpha Quant Ranking | Ahead P/E |

| D.R. Horton | Purchase (3.89) | 10.83 |

| Lennar Company | Maintain (3.04) | 11.30 |

| NVR | Maintain (3.06) | 16.34 |

| PulteGroup | Sturdy Purchase (4.76) | 9.08 |

| Lowe’s Corporations | Maintain (3.27) | 19.13 |

| Sherwin-Williams | Maintain (3.05) | 28 |

| Dwelling Depot | Maintain (3.25) | 23.57 |

| TopBuild | Purchase (4.44) | 19.82 |

| Toll Brothers | Maintain (3.40) | 8.74 |

| Builders FirstSource | Maintain (2.70) | 12.04 |

Weighted Common (Place weight * indicator) | 3.54 | 14.36 |

Supply: In search of Alpha & Writer calculations

We observe that the highest ten holdings have a weighted common ahead P/E of 14.36 (earnings yield of 6.96%) and a weighted common In search of Alpha quant ranking of three.54. You possibly can be taught extra about In search of Alpha quant scores right here.

Future Federal Reserve Coverage

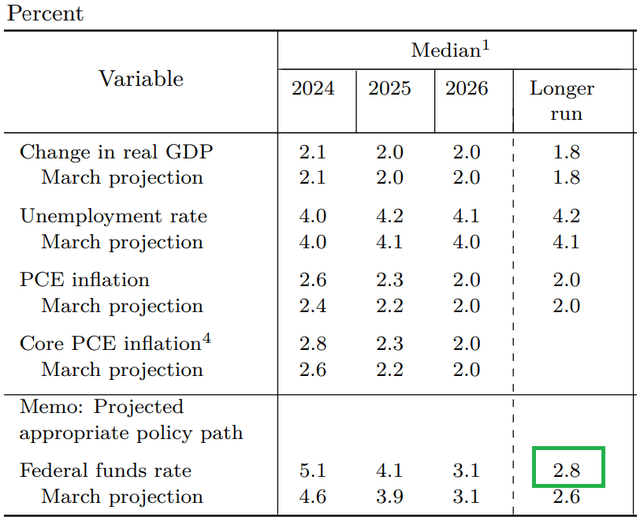

The homebuilding sector will likely be one of many key beneficiaries of decrease rates of interest as curiosity on mortgages carefully follows the FED funds price. Decrease mortgage funds will in flip improve the demand for housing. Futures pricing signifies the FED is prone to convey charges to 3.75-4.00% in July 2025, 1.5% decrease than present ranges. Moreover, in its June 2024 abstract of financial projections, FED officers signaled they anticipate additional cuts put up 2025, to a stage of about 2.8% in the long run:

Outlook for macroeconomic indicators ((Federal Reserve June 2024 Abstract of financial projections))

The earnings yield outlined within the earlier part stands at a weighted common of 6.96%. Combining it with the long-term GDP nominal development price of about 3.8% we see that traders are taking a look at a possible low double-digit return, even earlier than we issue within the one-off enhance from decrease rates of interest. Since dwelling constructing is quite capital intensive, you could be on the cautious facet and solely add inflation of two% quite than a lift from nationwide GDP development of 1.8%. Nonetheless, you’re looking at a excessive single-digit return, which is sort of good.

We should always notice the above return expectation is extra of a medium-term outlook and doesn’t think about leverage (which at 300% for NAIL is game-changing). Due to this fact the precise return traders could obtain could possibly be within the low-to-mid double digits if homebuilding shares leap as I anticipate.

Dangers

The principle danger going through traders in NAIL is an surprising pickup in inflation, which might freeze the Federal Reserve’s plans to steadily cut back rates of interest over the following few years. Moreover, homebuilding is a cyclical trade, therefore a possible recession someday sooner or later could dampen demand for houses. Recession danger is arguably extra manageable for the reason that FED is prone to minimize charges, reducing mortgage prices, and to an extent mitigating the recession’s affect on housing specifically.

The opposite reality to notice is that the expense ratio of 0.97% is sort of excessive for such a concentrated ETF. Over the long run, you’re prone to pay 1/10 of your potential return as charges to the ETF supervisor. As such, I view NAIL as extra of a speculative/buying and selling ETF over the following few years because the FED cuts charges and homebuilding shares admire. After that one-off enhance, nevertheless, I believe you’re higher off replicating the ETF’s portfolio to avoid wasting on charges.

Lastly, we must always notice that since NAIL is monitoring the underlying index’s efficiency threefold, it will likely be fairly a risky ETF as homebuilding shares will transfer strongly on every inflation/jobs report or Federal Reserve coverage assembly.

Distributions

NAIL pays a quarterly dividend however with a yield of 0.25% clearly the principle attraction of the ETF is just not in its revenue potential. We should always notice that numerous parts, akin to D.R. Horton (DHI) conduct sizable share buyback packages. As such, you shouldn’t leap to the conclusion that NAIL holdings are by default not shareholder-friendly.

Conclusion

The Direxion Each day Homebuilders & Provides Bull 3X Shares ETF has considerably lagged the broad U.S. market up to now in 2024. In opposition to the backdrop of expectations for FED price cuts that may materially enhance the housing market and an undemanding valuation of prime ten holdings, I believe NAIL will likely be a worthwhile funding over the following few years. I’d notice nevertheless that the excessive expense ratio coupled with excessive focus in just a few names cut back the long-term attraction of NAIL as a buy-and-hold funding. Nonetheless, the ETF could current the perfect alternative for traders with a short-term horizon, and as such I price it a purchase.

Thanks for studying.

")

{kind=link}