Published on March 24th, 2023 by Aristofanis Papadatos

Keyera Corporation (KEYUF) has two appealing investment characteristics:

#1: It is a high-yield stock based on its 6.9% dividend yield.

Related: List of 5%+ yielding stocks.

#2: It pays dividends monthly instead of quarterly.

Related: List of monthly dividend stocks

You can download our full Excel spreadsheet of all monthly dividend stocks (along with metrics that matter, like dividend yield and payout ratio) by clicking on the link below:

The combination of a high dividend yield and a monthly dividend render Keyera Corporation appealing to individual investors.

But there’s more to the company than just these factors. Keep reading this article to learn more about Keyera Corporation.

Business Overview

Keyera Corporation engages in the gathering and processing of natural gas; and transportation, storage, and marketing of natural gas liquids in Canada and the U.S. It operates through Gathering and Processing, Liquids Infrastructure, and Marketing segments. The company was formerly known as Keyera Facilities Income Fund and changed its name to Keyera Corporation in 2011. Keyera was founded in 2003 and is headquartered in Calgary, Canada.

Keyera has some attractive characteristics. First of all, it has assets in high-value markets, which are characterized by high barriers to entry.

Source: Investor Presentation

Keyera also operates with a highly integrated business model, which results in wide profit margins. In addition, the company is making great efforts to reduce its carbon dioxide emissions and has set ambitious goals for emission reductions.

As Keyera has a business focused on natural gas and natural gas liquids, it has exhibited a highly volatile performance record due to the cycles of the natural gas industry. On the other hand, Keyera is less vulnerable to the cycles of the price of natural gas than natural gas producers. As a result, it has remained profitable every single year over the last decade, in sharp contrast to most upstream players in this industry.

Just like almost all the oil and gas producers, Keyera saw its earnings collapse in 2020 due to the plunge of the price of natural gas caused by the pandemic. However, in contrast to its peers, the company remained profitable in that exceptionally adverse year. Even better, thanks to the massive distribution of vaccines worldwide, the natural gas market recovered in 2021, and thus the company returned to high profitability in that year.

On the other hand, investors should note that the defensive business model of Keyera has two faces. It renders the company more resilient to the downturns of its industry but does not allow it to benefit as much as the upstream companies during boom times.

In early 2022, the onset of the war in Ukraine rendered the global gas market extremely tight. As a result, the price of natural gas skyrocketed to a 13-year high last year. That rally led gas producers to post record profits last year. On the contrary, Keyera saw its earnings per share dip 6%, mostly due to increased capital expenses.

Growth Prospects

Keyera tries to grow its earnings by enhancing the capacity of its facilities and by expanding its network. The company is currently in the process of integrating its North region gathering and processing facilities with the heart of its integrated value chain at Fort Saskatchewan. When this project is completed, it will significantly enhance the growth potential of Keyera.

On the other hand, as mentioned above, Keyera is sensitive to the cycles of the natural gas industry. This is clearly reflected in the volatile performance record of the company. During the last nine years, Keyera has grown its earnings per share by only 2.4% per year on average.

Keyera currently enjoys strong business momentum, partly thanks to the Ukrainian crisis and the deep production cuts implemented by OPEC in an effort of the cartel to support the price of oil. Due to the tight production quotas of OPEC, the U.S. and Canada have become the primary global producers that are increasing their production in order to balance the market. As a result, higher volumes of natural gas pass through the network of Keyera.

Given the positive business momentum but also the volatile nature of the business of Keyera, we expect its earnings per share to grow by about 2.5% per year on average over the next five years, roughly in line with the historical growth rate.

Dividend & Valuation Analysis

Keyera is currently offering an above-average dividend yield of 6.9%, which is more than quadruple the 1.6% yield of the S&P 500. The stock is thus an interesting candidate for income-oriented investors but the latter should be aware that the dividend is not safe due to the cyclical nature of the natural gas industry.

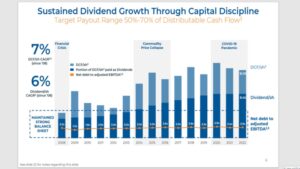

Keyera is doing its best in the factors of its business it can control. Since 2008, the company has grown its distributable cash flow per share by 7% per year on average.

Source: Investor Presentation

Keyera targets a payout ratio of 50%-70% and has a strong balance sheet, with a leverage ratio (Net Debt to EBITDA) of 2.5. As a result, its dividend has a margin of safety.

On the other hand, due to the cyclicality of the business of Keyera, its dividend is not entirely safe. In addition, U.S. investors should be aware that the dividend received from this stock depends on the exchange rate between the Canadian dollar and the USD.

In reference to the valuation, Keyera is currently trading for 19.0 times its earnings per share in the last 12 months. We assume a fair price-to-earnings ratio of 18.0 for the stock. Therefore, the current earnings multiple is somewhat higher than our assumed fair price-to-earnings ratio. If the stock trades at its fair valuation level in five years, it will incur a -1.1% annualized drag in its returns.

Taking into account the 2.5% annual growth of earnings per share, the 6.9% current dividend yield, and a -1.1% annualized contraction of valuation level, Keyera could offer a 7.5% average annual total return over the next five years. This is a decent expected return, but we recommend waiting for a lower entry point in order to enhance the margin of safety and increase the expected return.

Final Thoughts

Keyera has a more defensive business model than natural gas producers and is offering an exceptionally high dividend yield of 6.9%. Thanks to its strong balance sheet, the company is not likely to cut its dividend anytime soon. As a result, it is likely to entice some income-oriented investors.

However, the company has exhibited a highly volatile performance record due to its business cycles. Therefore, investors should wait for a more attractive entry point.

Moreover, Keyera is characterized by extremely low trading volume. This means that it may be hard to establish or sell a large position in this stock.

If you are interested in finding more high-quality dividend growth stocks suitable for long-term investment, the following Sure Dividend databases will be useful:

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly:

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

")

")

{kind=link}