Up to date on Might fifth, 2022 by Quinn Mohammed

Worldwide REITs could possibly be a precious choice for buyers occupied with diversifying their portfolios. There are lots of worldwide Actual Property Funding Trusts based mostly exterior the U.S. with high quality enterprise fashions and excessive dividend yields.

One instance is Granite Actual Property Funding Belief (GRP.U) (GRT-UN.TO), a REIT based mostly in Canada. Not solely does Granite have a confirmed enterprise mannequin, nevertheless it additionally pays a strong 3.4% dividend yield, which is about twice the extent of the S&P 500.

Granite additionally pays its dividend month-to-month; a extra engaging dividend schedule than REITs which pay dividends quarterly.

Granite is one among solely 50 shares that pays month-to-month dividends. You may entry the complete database of month-to-month dividend shares (together with necessary monetary metrics equivalent to price-to-earnings ratios and dividend yields) by clicking on the hyperlink under:

Granite is listed in each Toronto and New York, and for this text, we’ll be utilizing the New York itemizing and US {dollars}.

This text will define Granite’s enterprise mannequin and talk about its deserves as a dividend inventory.

Enterprise Overview

Granite owns and manages predominantly industrial actual property properties in North America and Europe. It transformed to a REIT on January 3, 2013, and has reworked itself right into a leaner, extra environment friendly belief, with higher-quality belongings.

Supply: Investor presentation

Over time, Granite has grown from a smaller, much less precious portfolio that was nearly solely dependent upon one tenant (Magna), to a diversified, a lot bigger portfolio with considerably increased common property values. The belief has undergone a metamorphosis in recent times to achieve these objectives, and it’s clear that effort has paid off.

Magna is now 22% of the portfolio, and the portfolio as a complete is meaningfully extra diversified between tenants and property varieties.

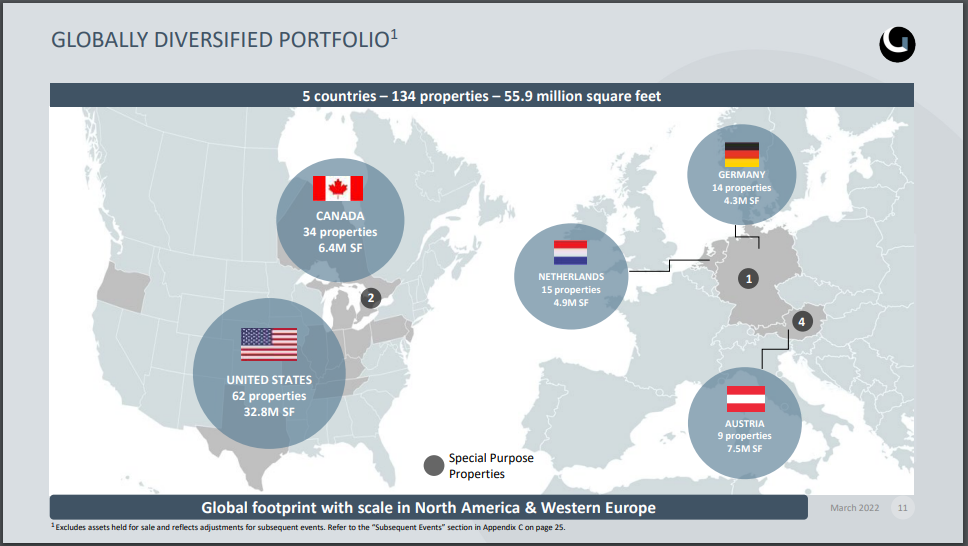

The belief’s income-producing portfolio include Multi-Function, Logistics and Distribution Warehouses, and Particular-Function services. It owns a complete of 55.9 million sq. ft unfold throughout 134 properties in Europe, Canada, and the U.S. Mixed, these properties have a carrying worth of almost $8 billion.

Supply: Investor presentation

Granite is current solely in nations with little or no geopolitical threat, and in properties and industries with robust long-term fundamentals. It’s nonetheless very closely concentrated within the US and Canada, with slightly greater than two-thirds of its properties sq. footage situated in North America.

Nonetheless, its worldwide publicity supplies a diversifying element to the belief’s outcomes. Granite focuses on properties that help e-commerce growth and are situated strategically to help such companies in the most effective markets.

Supply: Investor presentation

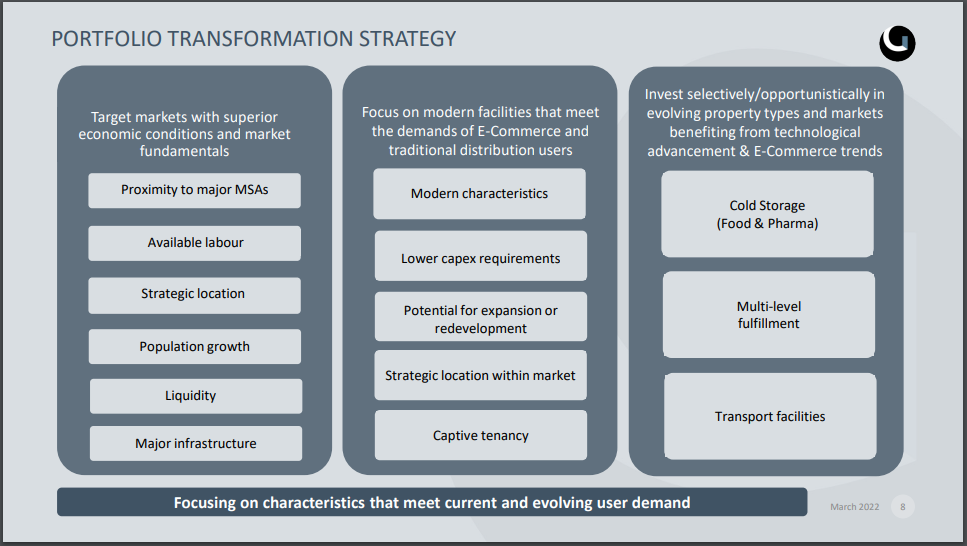

Granite seeks out areas which have proximity to main cities and have favorable demographics, together with main infrastructure, and obtainable labor swimming pools. As well as, it buys properties which might be already trendy, that means capital expenditure wants are low, with tenants which have excessive switching prices.

These traits imply that Granite is selecting solely essentially the most favorable properties to personal with long-term tenants which have the most effective likelihood of thriving in varied financial climates. Lastly, it focuses on the big shift to e-commerce, with a specific deal with meals and prescription drugs.

In brief, Granite is betting that these traits will gas its future progress, and outcomes have actually supported that notion.

Development Prospects

Granite’s outlook is constructive from a basic perspective, with the belief within the midst of a metamorphosis. Granite is within the ultimate phases of its years-long transformation through which it’s optimizing its value of capital, leverage on the stability sheet, and reaching what it considers a saturation level in important goal markets.

The belief went by means of a interval of serious transition in recent times, switching out its CEO, board, and management crew. As we speak, the belief is targeted on remodeling its portfolio by means of the sale of non-core belongings, enhancing its presence within the U.S, and making purchases in choose European markets.

Granite delivered on its prior acknowledged purpose of boosting the portfolio to greater than 40 million sq. ft and carrying worth of greater than $4 billion, and is now approaching $8 billion, so we imagine the very best ranges of progress are probably behind the corporate. That stated, future progress might be comprised primarily of rental will increase, and selective acquisitions which might be accretive to FFO. Acquisitions make up a big a part of the corporate’s progress technique, as they’ve accomplished roughly $2.0 billion in acquisitions over the past two years in key places.

Granite seems to have achieved its progress objectives sooner than anticipated, and in consequence we anticipate incremental funding to gradual considerably within the coming years. There may be nonetheless a growth pipeline in progress, with some properties in Europe and North America. Nevertheless, Granite’s transformative strikes have largely been accomplished.

Tendencies for e-commerce stay overwhelmingly constructive and given the affect on bodily retailers of COVID-19, it seems the pattern in direction of e-commerce has solely accelerated, which is a constructive for Granite. It’s due to this fact concentrating belongings that match its funding standards to capitalize.

Granite’s progress outlook is favorable, on condition that it ought to proceed to see increased hire costs, in addition to a bigger funding e-book by means of acquisitions and growth.

Dividend Evaluation

Granite at the moment pays a month-to-month dividend of $0.2583 per share in Canadian {dollars}, which equates to ~$0.20 month-to-month in US {dollars}. The newest dividend improve got here in December of 2021, within the quantity of three.3%.

On an annualized foundation, the present common dividend fee is $3.0996per share in Canadian forex. In U.S. {dollars}, this works out to roughly $2.43 per share. This equates to a 3.4% yield.

It must be famous that if buyers personal the U.S. itemizing, the dividend might be topic to forex threat as it’s translated from Canadian {dollars} to U.S. {dollars}. The dividend to U.S. buyers will rely partly upon prevailing change charges, which at the moment stand at $1 CAD = $0.78 USD. One other necessary consideration for investing in worldwide shares is withholding taxes.

Word: As a Canadian inventory, a 15% dividend tax might be imposed on US buyers investing within the firm exterior of a retirement account. See our information on Canadian taxes for US buyers right here.

Granite’s 3.4% dividend yield is supported with underlying money circulation. Primarily based on adjusted FFO for 2021, Granite’s payout ratio is 80%. That’s about according to earlier years and is taken into account protected within the REIT universe.

We imagine Granite goes to develop FFO within the coming years and cut back the payout ratio, so at the side of the present honest payout ratio, we see the distribution as protected.

Remaining Ideas

Buyers can obtain excessive ranges of earnings and diversification advantages by contemplating REITs based mostly exterior america. Granite REIT is an efficient instance of a global REIT with a high-quality enterprise mannequin, and a good dividend yield of three.4%.

The belief has largely accomplished its transformation effort that diversified its portfolio, decreased threat, and enhanced its earnings progress prospects. We see this as supportive of future dividend will increase, because the payout ratio has been decreased considerably. Consequently, Granite stays a lovely choice for buyers searching for month-to-month dividends and a 3%+ dividend yield.

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

")

{kind=link}