zhnger

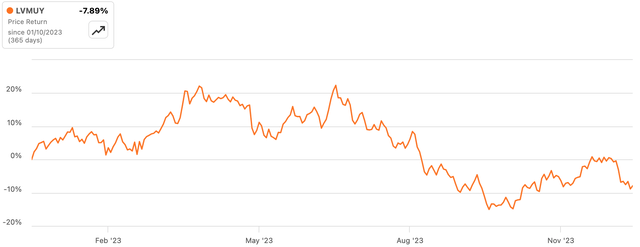

Shares of luxury goods empire LVMH Moët Hennessy Louis Vuitton (OTCPK:LVMUY)(OTCPK:LVMHF) have been uncharacteristically soft recently, delivering a circa negative 6% total return over the past 12 months amid fears of a broader slowdown in the global luxury market.

Source: Seeking Alpha

While this may well be coming to pass, LVMH is a best-in-class operator, and I expect it to hold up relatively well as a result. With the shares now at 21.5x TTM EPS, I expect long-term growth to land just high enough to make a current investment worthwhile, and I attach a Buy rating to the stock.

LVMH Overview

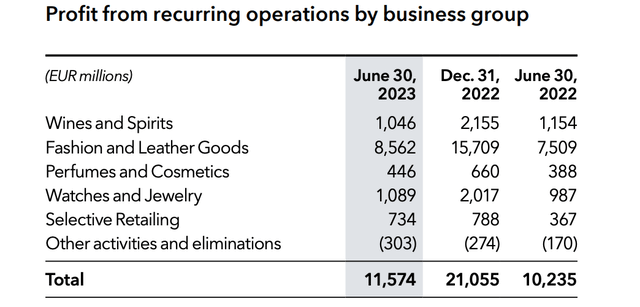

LVMH owns an empire of luxury brands, including namesakes Louis Vuitton, Moët, Hennessy, as well as other world famous names such as Christian Dior, Bulgari, TAG Heuer and Guerlain. By business group, Fashion & Leather Goods accounts for over 70% of group operating profit, followed by Wines & Spirts, Watches & Jewelry, Selective Retailing and Perfumes & Cosmetics.

Source: LVMH 1H 2023 Results Release

While the company doesn’t officially break down sales by specific brand, it has provided enough tidbits to suggest that Louis Vuitton is a €20 billion business, making it responsible for around 25% of group sales. Margins in the Fashion & Leather Goods segment are already the strongest in the group (EBIT margin is around 40% for that segment), with Louis Vuitton margins likely higher than that. Thus, Louis Vuitton will be an even bigger contributor to group earnings than sales.

One key aspect to appreciate about the Louis Vuitton brand is that LVMH takes on the entirety of both production and distribution. It does not sell through wholesale channels. In theory, this should come with minuses as well as plusses. In terms of the latter, growing wholesale channel sales can lead to significant fixed-cost leverage given the absence of store-level expenses. The downside is that luxury is an unusual industry because perceived scarcity/exclusivity is what generates demand and therefore sales. While 99% of businesses would be very happy growing volumes by a lot, in the luxury industry this has to be monitored closely. As a result, wholesale channel sales present a larger risk of over-saturation and markdowns to shift stock, which could damage the brand, as has happened to peers like Burberry (OTCPK:BURBY)(OTCPK:BBRYF) in the past.

Furthermore, Louis Vuitton is likely intensely profitable at the store-level in any case, as €20 billion in annual sales are leveraged over a small store footprint (~460 currently) with relatively little sold online. Taking the risk with the wholesale channel is probably not worth any little extra benefit it would bring.

Another key thing to appreciate about LVMH’s business is the alcohol segment. Although it has a cyclical bent, especially its Cognac and Spirits business, this segment can act as a stabilizer to the fashion part the business. For years, analysts have wondered whether the company might offload this division, as there is little overlap and synergies that can be gleaned between it and the other operating groups. Because LVMH is basically a publicly-listed family business (headed by Bernard Arnault), my guess is that this stabilizing presence is appreciated, as family run businesses are often less concerned with pleasing Wall Street and more concerned with long-term wealth building and preservation. I consider it a plus and a key differentiator to peers.

Sales Growth Moderating

Recently, the market has been concerned about a potential slowdown in the global luxury market. While I see this as inevitable, LVMH is still producing decent numbers.

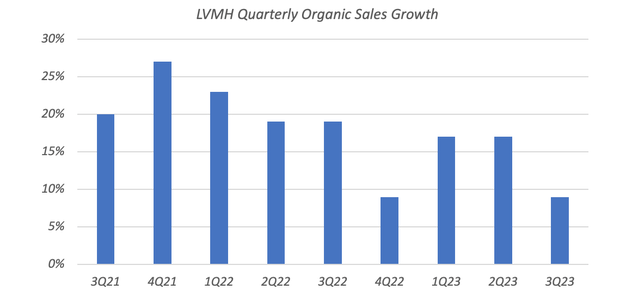

In the most recent quarter for which we have data (Q3 2023), the company reported 9% year-on-year organic revenue growth at constant exchange rates. This figure isn’t actually bad in its own right and even relative to peers – it is worse than best-in-class Hermès (OTCPK:HESAY)(OTCPK:HESAF)(16% YoY growth in Q3), but better than Burberry (1% YoY growth in its fiscal Q2, which maps to LVMH’s Q3 2023) and Gucci owner Kering (OTCPK:PPRUY)(OTCPK:PPRUF)(9% YoY decline in Q3). However, it did represent a sizable slowdown on the 17% growth reported in both Q1 and Q2, spooking analysts a little.

Data Source: LVMH Quarterly Results Releases

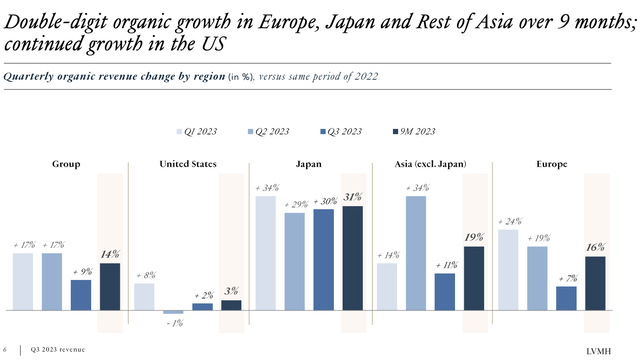

Digging a little deeper, performance in the United States continued to be relatively soft, with organic sales up just 3% year-on-year. This is a key market for LVMH, accounting for around a quarter of group sales. As I commented in a recent piece on peer Burberry, a large portion of this is due to normalizing consumer behavior post-COVID, with headwinds coming from a resumption of student loan repayments and the drawdown of stimulus money. Previously, U.S. sales had ballooned from €12.6 billion in 2019 to €21.5 billion in 2022, fueled by the huge COVID fiscal stimulus. This growth CAGR was always unsustainable and now requires a period of digestion, so the slowdown here does not concern me too much.

Source: LVMH Q3 2023 Trading Update Presentation

One bright spot is the Chinese customer base. While Asia ex-Japan sales moderated to 11% from 23% in H1, a portion of this is simply because Chinese customers have been traveling abroad again. This was a key source of sales in markets like Europe before COVID, with the pandemic shifting those sales temporarily to Asia due to travel restrictions. That trend is unwinding again, with management noting that overall Chinese customer demand remains robust:

So starting with the Chinese cluster. As far as the Chinese are concerned, I mentioned in July that if you look at the right way, i.e., globally, organically and over 2 years in order to overcome the fluctuations in a comparison base in 2022, we were about growing in the Fashion & Leather division about 40% with most of our brands there. We have slight discrepancies, but most of our brands were growing about 40% over 2 years. It’s exactly the same in Q3.

Jean-Jacques Guiony, CFO LVMH Moët Hennessy Louis Vuitton, Q3 Trading Update Call

Growing wealth in Greater China is a major part of the bull case here, as Chinese sales percolate throughout the globe. This is why European sales were a robust 16% in Q3, despite local customers not being in particularly good shape:

As far as European is concerned, I would say that most — we’ve seen notable change in Q3. Most nationalities in Europe used to be high single digit to low double digit. They are now mid-single digit down in Q3. So that’s the main change. Yet bear in mind that as far as Europe is concerned, the weight of locals is much lower than it is in other countries and particularly the weight of touristic flows remains extremely high and is pretty close to what it was prior to the pandemic.

Jean-Jacques Guiony, CFO LVMH Moët Hennessy Louis Vuitton, Q3 Trading Update Call

LVMUY Stock Can Deliver Good Long-Term Returns

With EPS still growing and the ‘LVMUY’ ADSs having fallen around 7% over the past year, the stock’s valuation has de-rated, and I now view it as attractive. Based on TTM EPS through H1 2023 (~$7 per ADS), the stock trades on a P/E of 21.4. That is down from around 29x TTM EPS 12 months ago.

Source: Seeking Alpha

The luxury market is expected to grow at a circa 5% CAGR through 2030, around a point lower than its prior historical rate. Given the strength of brands like Louis Vuitton, I expect LVMH to be able to price ahead of this in its Fashion & Leather Goods segment, leading to high single-digit annualized sales growth. The rest of its business groups should grow at around 5%, in line with the wider global luxury market. I expect the company to be able to leverage this into high single-digit annualized underlying EBIT growth overall.

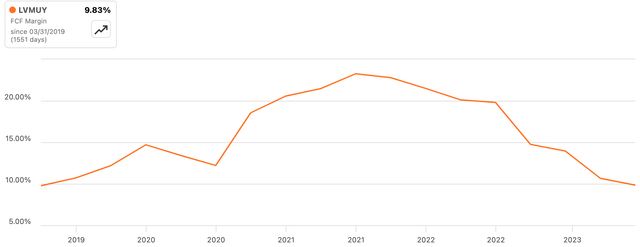

LVMH generates substantial free cash flow, which in its recent history has landed at a double-digit share of revenue and for a cash conversion of over 1x (i.e. greater than net income).

Source: Seeking Alpha

This fell a little in H1 2023 (the last period for which there is consolidated financial data), as the firm was making heavy investments in its alcohol and jewelry businesses, but should be robust over the long run. The dividend currently amounts to $2.75 per ADS, for a current yield of 1.8% on a circa 40% payout ratio. This leaves substantial surplus FCF to further grow EPS. The company’s balance sheet is also in sound health, with net financial debt of €12.5 billion equating to less than 0.5x annual EBITDA. This can support cash returns to shareholders via M&A, buybacks and so on.

LVMH has been a serial acquirer over the years, and I expect M&A to continue to form part of the mix going forward. It has also been dipping its toe into buybacks, with European firms still relatively ‘new’ to this compared to American firms. Together, I expect this to add to EPS growth, with 9-10% annualized growth achievable over the long-run. With 1.8% from the dividend, that gets us to around 11-12% in total, enough to prudently bake in around 1-2% from long-term P/E multiple contraction and still come out with around 10% annualized returns overall. I consider that attractive for a high quality business that conveys ownership of prestige consumer brands, and I attach a Buy rating to the stock.

Risks

The main risks to LVMH are macro and brand related. Chinese consumers are a key part of LVMH’s customer base and form the core of its long-run growth prospects. A continuation of robust per-capita GDP growth in Greater China is implicit in my growth forecasts, which could prove too optimistic if economic development in the region stalls. Core brands like Louis Vuitton could also fall out of favor with consumers, blunting long-term volume growth and pricing power. Finally, I would note that the luxury sector remains cyclical, with the potential for near-term volatility regardless of long-term growth prospects. This could also make the stock a particularly volatile investment over shorter timeframes.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

")

{kind=link}