Shares of JM Smucker Co. (NYSE: SJM) have gained 7% over the previous 12 months. The corporate continues to face challenges from inflation and provide chain disruptions and expects these pressures to proceed within the close to time period. It continues to put money into its enterprise and reshape its portfolio as a part of its efforts to focus extra on its high-growth classes.

Gross sales and demand

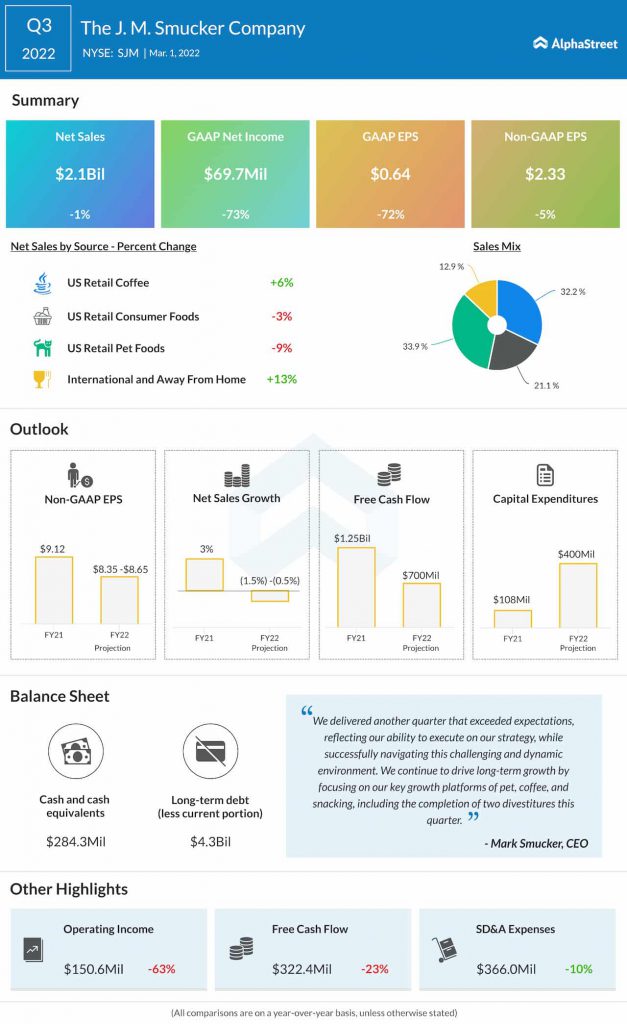

JM Smucker continues to see robust demand for its manufacturers. Whereas web gross sales decreased 1% through the third quarter of 2022, comparable gross sales elevated 4%, pushed by robust efficiency from the corporate’s main manufacturers in espresso, frozen sandwiches, pet snacks and cat meals.

The corporate continues to revamp its portfolio. The divestitures of its Non-public Label Dry Pet Meals enterprise and Pure Beverage and Grains companies in Q3 will assist it focus extra on the classes which have increased development alternatives.

Throughout the Pet Meals enterprise, development in canine snacks and cat meals was not sufficient sufficient to offset declines in pet food which led to a comparable gross sales decline of 1%. As provide chain disruptions proceed to harm this enterprise, JM Smucker is allocating provide and manufacturing to its extra worthwhile manufacturers, resembling Meow Combine cat meals.

Espresso noticed gross sales development of 6% with development in all manufacturers because the pandemic-fueled development of at-home espresso consumption continued to stay. This development was led by the Dunkin and Café Bustelo manufacturers, which noticed will increase of 12% and 15% respectively in shopper takeaway.

The Client Meals enterprise recorded comparable web gross sales development of 4%, pushed by a 30% development in Uncrustables frozen sandwiches. Uncrustables is properly on its approach to turning into a $1 billion model in annual web gross sales over the subsequent 5 years as SJM continues to speculate meaningfully on this model.

For fiscal yr 2022, SJM expects web gross sales to say no 1.5% to 0.5% from the earlier yr. Comparable web gross sales are anticipated to extend approx. 4.5% on the midpoint of the steering vary, reflecting momentum in manufacturers and advantages from increased pricing actions.

Inflation and provide chain headwinds

In the course of the third quarter, JM Smucker’s backside line was harm by increased prices. Provide chain and transportation constraints, together with labor shortages, impacted the corporate’s capacity to totally meet demand. The underside line will proceed to be pressured as a result of time lag between the pricing actions being carried out and taking impact.

In Q3, increased prices for commodities, manufacturing and transportation led to an 8% drop in adjusted gross revenue and a 6% lower in adjusted working earnings. All these elements led to a 5% decline in adjusted EPS to $2.33.

SJM expects gross revenue margin to be round 35% in FY2022 as increased value inflation is anticipated to offset increased pricing and value and productiveness financial savings. Adjusted EPS for the complete yr is now anticipated to vary between $8.35-8.65 versus the earlier vary of $8.35-8.75.

Click on right here to learn the complete transcript of JM Smucker’s Q3 2022 earnings convention name

{kind=link}