The mobile-first brokerage and (Reddit-legendary) stock trading platform Robinhood recently launched a product that no one saw coming: Robinhood brand IRAs. It was a peculiar choice given Robinhood’s history as the number one choice for /r/wallstreetbets-style meme trading and poorly thought out options trades, but Robinhood’s gone and done it anyway.

There’s no shortage of places to set up an IRA—most banks, brokerages, and other financial institutions, for instance—so Robinhood throwing its feathered cap into the ring is kind of curious.

Clearly they think they have some unique value proposition or see an opportunity to make money off of their new IRAs, but do you really want to turn to Robinhood for your retirement planning?

So what’s the deal with these Robinhood IRAs? Are they a good deal? Do they have some unique features or compelling reason for customers to invest in their IRAs, or would consumers be better off opting for an IRA from a more established financial institution?

Let’s dive in. But first, a little context.

It Stands for Individual Retirement Account

IRAs, or individual retirement accounts, are special investment accounts that help individuals save for retirement (hence the name).

Much like 401(k)s, IRAs are essentially managed investment portfolios that enjoy certain tax advantages, though there are some differences.

While 401(k)s are typically provided and managed by a person’s employer, IRAs and the investments they hold are usually managed by their owners. There are also slightly different tax implications between 401(k)s and IRAs, but we won’t get into all that here.

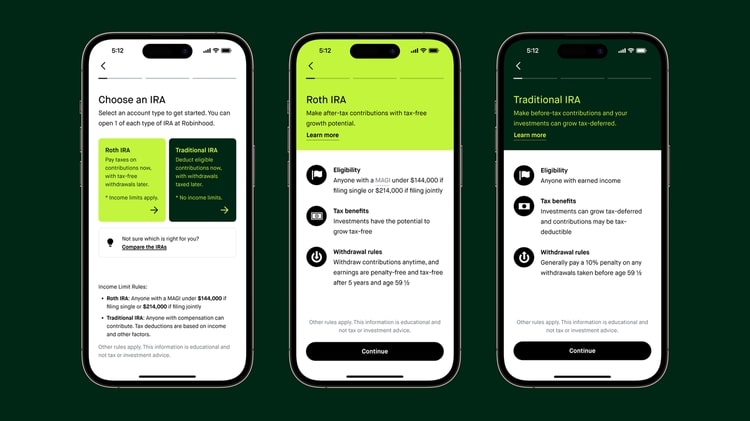

IRAs come in several flavors, though Robinhood only offers the two most common types: traditional IRAs and Roth IRAs.

Pro Tip:

When you sign up for a Robinhood IRA, you’ll get a 1% match for all funds you contribute to your retirement account up to the legally allowed contribution limit. Plus, you can earn up to $1700 per year in FREE STOCK through a Robinhood brokerage account!

Traditional IRA

A traditional IRA is essentially an investment portfolio that you can contribute certain amounts to every year.

For 2022 the limits were up to $6,000 ($6,500 in 2023) for people under the age of 50 and up to $7,000 ($7,500 in 2023) for people 50 and above. Note that these contributions apply for all IRAs that you have, as in you can only contribute up to $6,500 in total across your IRAs, not $6,500 per IRA.

Contributions below and up to the limit are tax-deductible, as are any transactions and earnings that occur inside the portfolio. When you retire you can withdraw funds from an IRA and have them taxed as regular income, though there are additional penalties associated with taking out money before retirement.

Withdrawal Age and Penalties:

You can start withdrawing money from your IRA when you turn 59 and a half.

Any funds that you withdraw will be taxed like regular income. You can technically withdraw funds from an IRA before you turn 59 and a half, but you’ll pay a 10% penalty on top of any income taxes you owe.

And while there are some circumstances that will let you avoid that 10% penalty, that gets into some thorny tax territory that would be neither useful nor interesting to get into.

Roth IRA

Roth IRAs are a little different. They’re structured and administered like traditional IRAs, any transactions that happen and earnings that accrue inside of a Roth IRA are also tax-free, and you can withdraw earnings after retirement without incurring a tax penalty.

The Difference:

There are two big differences between traditional and Roth IRAs.

- You can’t deduct any contributions you make to a Roth IRA, but you can withdraw those contributions (but not gains) at any time without incurring a penalty

- There are income limits associated with Roth IRAs

- For 2022 you can only contribute to a Roth IRA if your income is under $144,000 for a single person or under $214,000 if filing jointly

- For 2023 the income limits are raised to $153,000 and $228,000, respectively

TO SUMMARIZE:

Contributions to a traditional IRA are tax deductible, and will be taxed as regular income when you take withdrawals during retirement. Contributions to a Roth IRA are made with after-tax dollars and will not be taxed when you take withdrawals during retirement. You don’t pay taxes on your capital gains or dividend income in either account.

Now that we know a bit about IRAs, let’s talk about what Robinhood has to offer.

Robinhood IRAs

Robinhood Retirement (Robinhood’s IRA program) offers both traditional and Roth IRAs. The process for setting up either and/or both is the same: just select the Retirement option in the menu on the site or in the app and follow the prompts, and before long you’ll have your new account(s) set up.

How Many Robinhood IRAs Can You Have?

You can open one of each kind of IRA that Robinhood offers even if you have other retirement accounts elsewhere, though you’ll still have to abide by the contribution and income limits regardless of the kind and location of your IRAs.

Anyway, once you have your IRA(s) set up you can start transferring in money from your brokerage account and/or external bank accounts. If you don’t want to wait for the money to arrive you can also opt into the IRA Instant program, which lets you instantly deposit up to $1,000 and start trading while you’re waiting for your money to arrive from the bank.

That’s all the basic stuff covered. Now let’s talk about some of the other features of Robinhood IRAs, starting with the biggest one.

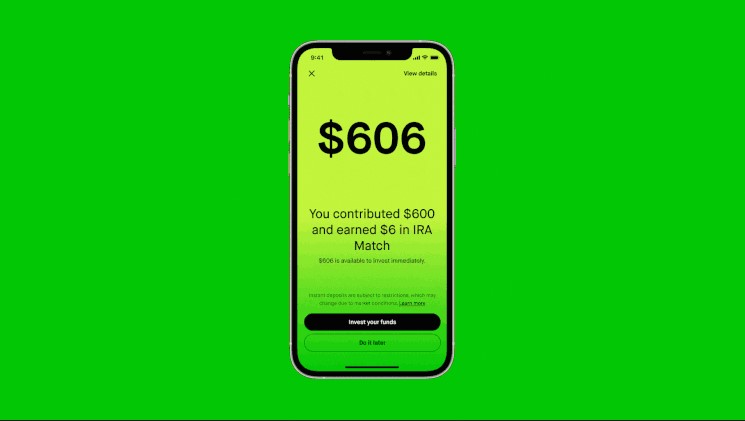

Matching Funds

Robinhood’s biggest selling point for their IRAs is that they’re willing to provide a 1% match on every dollar you contribute to one of their IRAs. You don’t need an employer or anything to receive these matching funds, and they also don’t count toward your contribution limits for the year.

You’ll start earning the 1% matching funds as soon as you start contributing money to your IRA, but only if the money comes from an external bank, not your Robinhood brokerage account.

It’s not clear why the funds have to come from an external bank. Maybe they want to make sure the money isn’t just being transferred around in their system, or maybe they only want fresh new money instead of the same old money you gave them when you opened your brokerage account. Who knows.

Whatever the case, you’ll only get that 1% matching funds if you make contributions to your IRA from an external bank.

It’s a fairly nice thing for Robinhood to do for its customers. That said, they only match 1% of your contributions. That’s a penny per dollar.

In 2023 you can earn up to $65 or $75 in matching funds if you’re under or over 50, respectively. That’s not nothing…but it’s also not huge. Either way, it’s free money!

Pro Tip:

When you sign up for a Robinhood IRA, you’ll get a 1% match for all funds you contribute to your retirement account up to the legally allowed contribution limit. Plus, you can earn up to $1700 per year in FREE STOCK through a Robinhood brokerage account!

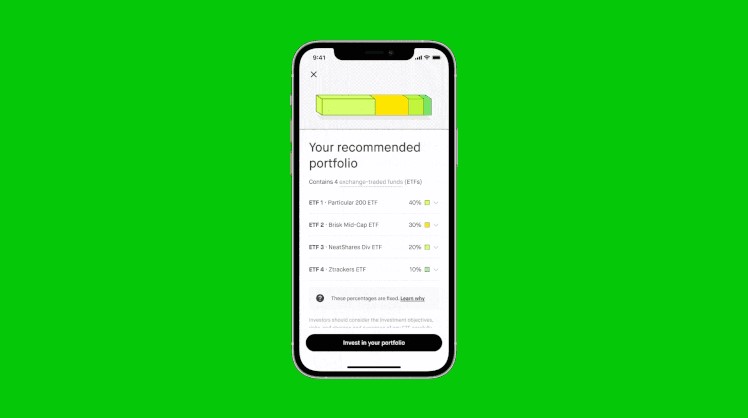

IRA Portfolios

If you open an IRA with Robinhood you’ll be given the choice between a pre-built recommended portfolio or a more self-directed experience.

The recommended portfolios are comprised of five to eight ETFs that are chosen by Robinhood’s algorithm based on the answers you give on a short questionnaire.

It’s not exactly clear what their criteria or methodology are for choosing the ETFs to populate your portfolio, though you can probably assume it has something to do with your investment goals, risk tolerance, and whether or not you have ESG-style priorities for your investments.

If you go to the self-directed route, on the other hand, you have a choice of pretty much everything that you can trade on Robinhood. That means you have a whole ton of stocks, ETFs, and options to choose from, but it also means you only have stocks, ETFs, and options to choose from.

Now, stocks, ETFs, and options are great. No one’s disputing that.

But for the more risk-averse clientele out there, Robinhood’s limited and volatile selection of securities may leave something to be desired. There’s no fixed income, no currencies, no alternative assets, nada.

And as much as those more volatile assets can appeal to younger investors with greater risk tolerance, a huge swath of potential investors may choose to open an IRA at a bigger institution with a more varied offering.

Is Robinhood Retirement Safe?

With all the recent commotion around the banking system (we’re looking at you, SVB), you might be wondering: are Robinhood IRAs safe?

In short: yes, Robinhood IRAs are safe.

The accounts are backed by protection by the Securities Investor Protection Corporation (SIPC), which protects your account up to $500k, half of which can be uninvested cash in your account.

Keep in mind that the SIPC does not protect you from losing money if your stocks go down in value. It protects you if your brokerage fails and you are unable to claim your rightfully owned securities and cash in your brokerage account.

Pro Tip:

When you sign up for a Robinhood IRA, you’ll get a 1% match for all funds you contribute to your retirement account up to the legally allowed contribution limit. Plus, you can earn up to $1700 per year in FREE STOCK through a Robinhood brokerage account!

Conclusion

Robinhood’s foray into the world of individual retirement accounts is interesting, to say the least. It’s easy enough to open an IRA, roll over any existing retirement accounts, and manage an IRA using Robinhood, but it may not be the best place to turn for your retirement planning.

Sure, Robinhood’s 1% match is nice. It’s more than most IRA providers would give you.

At the same time, though, those matching funds also come with the industrial-sized caveat of not being able to invest in anything beyond equities and options.

If you’re okay with being limited to just those securities, great! You’ll probably have a great time with Robinhood’s IRAs. If you’re more interested in having a well-diversified portfolio that doesn’t hinge on some of the most volatile securities out there, on the other hand, you may want to stay away.

Before you trust a brokerage to hold onto your hard-earned retirement earnings until you turn 59 and a half, you might want to get to know them a little better. And that’s totally understandable.

If you want to do some more research into whether or not Robinhood is safe and reliable, that’s a great idea.

To help you along the way, here are some articles answering the questions: Is Robinhood Safe? and Is Robinhood a Scam? Or if you want to learn more about how you can earn up to $1700 per year in free stock by referring friends, read our article about Robinhood Free Stock.

")

")

")

{kind=link}