da-kuk

Standardized efficiency (%) as of September 30, 2024

Quarter | YTD | 1 Yr | 3 Years | 5 Years | 10 Years | Since inception | ||

Class A (MUTF:MLPFX) shares inception: 03/31/10 | NAV | 3.13 | 20.42 | 27.89 | 22.32 | 13.14 | 3.71 | 6.69 |

Max. Load 5.5% | -2.49 | 13.80 | 20.90 | 20.01 | 11.85 | 3.12 | 6.27 | |

Class R6 shares inception: 06/28/13 | NAV | 3.33 | 20.78 | 28.36 | 22.70 | 13.51 | 4.05 | 5.28 |

Class Y shares inception: 03/31/10 | NAV | 3.25 | 20.76 | 28.26 | 22.63 | 13.43 | 3.97 | 6.97 |

Alerian MLP Index-GR | 0.72 | 18.56 | 24.46 | 25.47 | 13.50 | 1.82 | – | |

Whole return rating vs. Morningstar Vitality Restricted Partnership class (Class A shares at NAV) | – | – | 62% (59 of 95) | 31% (35 of 94) | 43% (45 of 92) | 22% (11 of 60) | – |

Calendar 12 months whole returns (%)

2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | |

Class A shares at NAV | 6.35 | -23.90 | 18.74 | -4.01 | -11.80 | 9.12 | -25.19 | 39.40 | 21.84 | 22.49 |

Class R6 shares at NAV | 6.68 | -23.58 | 19.02 | -3.58 | -11.64 | 9.66 | -25.02 | 39.89 | 22.18 | 22.85 |

Class Y shares at NAV | 6.51 | -23.69 | 19.06 | -3.69 | -11.68 | 9.55 | -25.18 | 40.02 | 22.02 | 22.79 |

Alerian MLP Index-GR | 4.80 | -32.59 | 18.31 | -6.52 | -12.42 | 6.56 | -28.69 | 40.17 | 30.92 | 26.56 |

Expense ratios per the present prospectus: Class A**: Internet: 6.59%, Whole: 6.62%; Class R6: Internet: 6.28%, Whole: 6.28%; Class Y**: Internet: 6.34%, Whole: 6.37%. ** Internet = Whole annual working bills much less any contractual charge waivers and/or expense reimbursements by the adviser in impact by at the very least Mar 31, 2025. The fund is structured as a C company and could also be topic to sure tax bills which can be mirrored within the expense ratio. Please seek advice from the present prospectus for extra info. Efficiency quoted is previous efficiency and can’t assure comparable future outcomes; present efficiency could also be decrease or larger. Go to Nation Splash for the newest month-end efficiency. Efficiency figures mirror reinvested distributions and adjustments in internet asset worth (NAV). Funding return and principal worth will range so that you just might have a acquire or a loss whenever you promote shares. Returns lower than one 12 months are cumulative; all others are annualized. As the results of a reorganization on Could 24, 2019, the returns of the fund for intervals on or previous to Could 24, 2019 mirror efficiency of the Oppenheimer predecessor fund. Share class returns will differ from the predecessor fund as a result of a change in bills and gross sales prices. Index supply: RIMES Applied sciences Corp. Had charges not been waived and/or bills reimbursed prior to now, returns would have been decrease. Efficiency proven at NAV doesn’t embody the relevant front-end gross sales cost, which might have decreased the efficiency. Class Y and R6 shares haven’t any gross sales cost; due to this fact efficiency is at NAV. Class Y shares can be found solely to sure buyers. Class R6 shares are closed to most buyers. Please see the prospectus for extra particulars. For extra info, together with prospectus and factsheet, please go to Invesco.com/MLPFX Not a Deposit Not FDIC Insured Not Assured by the Financial institution Could Lose Worth Not Insured by any Federal Authorities Company |

Supervisor perspective and outlook

West Texas Intermediate (‘WTI’) crude oil priced on the Cushing hub ended the quarter at $68.17 per barrel, down 16% from the tip of the second quarter and 25% decrease than one 12 months in the past. The unfold between Brent crude, a proxy for worldwide crude costs, and WTI ended the quarter at $3.60 per barrel, tightening in the course of the quarter.

Henry Hub pure gasoline costs ended the quarter at $2.92 per million British thermal items (MMbtu), up 12% from the tip of the second quarter and flat in comparison with one 12 months in the past. Fuel pricing within the Permian Basin ended the quarter decrease than the tip of the second quarter and skilled weak point (even buying and selling at destructive costs) in the course of the interval, as pipeline upkeep continued to strain already-constrained takeaway capability.

Pure gasoline liquids (NGLs) priced at Mont Belvieu ended the quarter at $24.86 per barrel, down 16% from the tip of the second quarter and 17% decrease than one 12 months in the past. Costs for the NGL purity merchandise had been blended at quarter finish, with butane and ethane buying and selling larger whereas propane, isobutane and pure gasoline traded decrease. Frac spreads, a measure of pure gasoline processing economics, settled at $0.37 per gallon, down 25% from the tip of the second quarter and 24% decrease than one 12 months in the past.

Portfolio positioning

Prime fairness issuers (% of whole internet belongings)

Fund | Index | |

MPLX LP (MPLX) | 7.04 | 10.24 |

Vitality Switch LP (ET) | 7.03 | 10.00 |

Western Midstream Companions LP (WES) | 5.97 | 9.82 |

Williams Cos Inc/The (WMB) | 4.85 | 0.00 |

Antero Midstream Corp (AM) | 4.82 | 0.00 |

Kinder Morgan Inc (KMI) | 4.81 | 0.00 |

Enterprise Merchandise Companions LP (EPD) | 4.75 | 9.87 |

Targa Assets Corp (TRGP) | 4.73 | 0.00 |

Sunoco LP (SUN) | 4.69 | 10.04 |

EnLink Midstream LLC (ENLC) | 4.63 | 9.28 |

As of 09/30/24. Holdings are topic to alter and should not purchase/promote suggestions. | ||

For the third quarter of 2024, grasp restricted partnerships (MLPs), as measured by the Alerian MLP Index (AMZ), had been down 1.05% on a value foundation and up 0.72% when together with distributions. For the quarter, the S&P 500 Index gained 5.53% on a value foundation and returned 5.89% together with distributions.

Many sector contributors continued to purchase again inventory as enticing valuations continued. Buyback disclosures traditionally sometimes accompany earnings stories, which path the quarter finish by a number of weeks (roughly $1.3 billion of buybacks had been disclosed with second quarter earnings stories).

We estimate MLP-focused funding autos, together with closed-end funds, open-end funds and index-linked merchandise, skilled roughly $313 million of internet inflows in the course of the quarter.

MLP capital funding included an estimated $5.0 to $6.0 billion of natural capital spending. As producer progress plans have remained average, midstream capital spending necessities have lessened, rising the free money out there to sector contributors for debt retirement, unit repurchases and distribution will increase in present and future intervals. Company mergers and acquisitions (M&A) remained wholesome, with a number of transactions introduced in the course of the quarter.

The ten-year US Treasury yield was 3.78% at quarter finish, down 0.62% from the tip of the second quarter. The MLP yield unfold, as measured by the implied yield of the AMZ Index relative to the 10-year Treasury yield, widened by 0.72%, ending the quarter at 3.38%. The long- time period common for the MLP yield unfold (2000 by the third quarter of 2024) is 4.39%. At quarter finish, the AMZ Index’s yield was 7.16%.

We consider that regardless of a number of years of outperforming the S&P 500 Index, midstream equities are properly positioned to offer buyers with a lovely yield and whole return expertise over the approaching years. Valuations have remained in our view enticing and fundamentals help expectations for money move progress for many sector contributors, significantly these with enterprise segments centered on key producing basins and people who help actions to export crude oil, refined merchandise, liquified petroleum gases (LPGs) and/or liquified pure gasoline (‘LNG’).

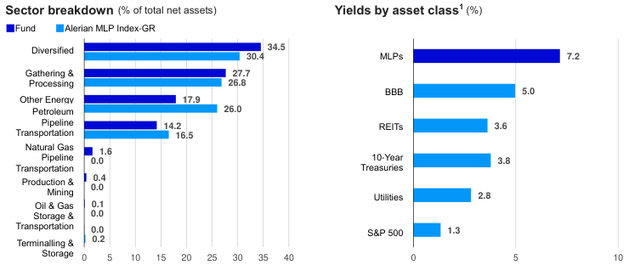

1 Supply: Bloomberg. Knowledge as of September 30, 2024 and is calculated utilizing the newest annualized distribution. MLPs are represented by the Alerian MLP Index (AMZ). Actual Property Funding Trusts (REITs) are represented by the FTSE NAREIT Fairness REIT Index. BBB Bonds (BBB) are represented by the U.S. Company Bond BBB yields. Utilities are represented by the Dow Jones Utilities Index. 10-Yr Treasuries are represented by the U.S. Treasury Bond 10-year yield. S&P 500 Index is an unmanaged capitalization-weighted index of 500 shares listed on numerous exchanges. Index efficiency is proven for illustrative functions and doesn’t predict or depict efficiency of the Fund. The indexes are unmanaged and can’t be bought instantly by buyers. Previous efficiency doesn’t assure future outcomes. |

Efficiency highlights

The pure gasoline pipelines sub-sector and the petroleum pipelines sub-sector supplied the very best relative efficiency in the course of the quarter. The pure gasoline pipeline group probably benefited from an outlook for rising pure gasoline demand pushed by LNG exports and information facilities. The propane and marine sub-sectors had the bottom common returns in the course of the quarter. Every sub-sector was hampered by idiosyncratic elements affecting sure sub- sector contributors.

Contributors to efficiency

Targa Assets Corp. (TRGP)

TRGP outperformed after reporting better- than-expected monetary and working outcomes and elevating 2024 money move steerage. The corporate is collaborating within the Blackcomb Pipeline three way partnership, taking a direct fairness stake within the subsequent pure gasoline egress resolution out of the Permian Basin, which is predicted to be in service within the second half of 2026.

ONEOK Inc. (OKE)

OKE outperformed after reporting monetary and working outcomes that had been above consensus expectations. Through the quarter, OKE introduced it’s going to purchase each Medallion Midstream, a personal crude gathering and transportation system, and World Infrastructure Companions’ fairness curiosity in EnLink Midstream (ENLC).

Kinder Morgan (KMI)

KMI outperformed in the course of the quarter regardless of reporting monetary outcomes that had been beneath expectations. KMI’s administration commentary highlighted strong progress in pure gasoline demand, partly pushed by information heart energy demand. KMI additionally introduced a 1.2 billion cubic ft/day growth on one in every of its interstate pure gasoline pipelines.

Detractors from efficiency

Genesis Vitality LP (GEL)

GEL items underperformed in the course of the quarter after administration decreased 2024 EBITDA steerage as a result of a decrease anticipated contribution from its soda ash enterprise. Regardless of the steerage discount, we consider GEL’s diversified asset base gives a secure revenue margin profile that’s anticipated to generate constant future money flows.

Western Midstream Companions LP (WES)

WES items underperformed in the course of the quarter after its sponsor, Occidental Petroleum (OXY), bought a block of shares at a reduction to the latest buying and selling value. The partnership reported monetary and working outcomes that had been according to expectations and signed a number of new long-term contracts with clients. WES is a crude and pure gasoline gathering and processing midstream firm centered on the Denver-Julesberg and Permian basins.

Sunoco LP (SUN)

SUN items underperformed in the course of the quarter regardless of continued power in gas margins supporting robust quarterly outcomes and market contributors showing to typically help its latest NuStar acquisition. SUN’s various geographic footprint, wholesome steadiness sheet and concentrate on the wholesale gas distribution enterprise is predicted to offer regular long-term operational outcomes.

Authentic Publish

Editor’s Word: The abstract bullets for this text had been chosen by In search of Alpha editors.

Editor’s Word: This text discusses a number of securities that don’t commerce on a serious U.S. change. Please concentrate on the dangers related to these shares.

")

{kind=link}