supersizer

A Quick Take On InnovAge Holding

InnovAge Holding Corp. (NASDAQ:INNV) reported its FQ2 2023 financial results on February 7, 2023, missing revenue but beating EPS consensus estimates.

The firm provides a healthcare service delivery platform for capitated care to high-cost, dual-eligible seniors in the U.S.

Until I see organic revenue growth start showing up in its financial results, along with a full California release of new enrollment sanctions, I’m on Hold for INNV stock.

InnovAge Overview

Denver, Colorado-based InnovAge Holding Corp. was founded to develop its InnovAge Platform to reduce unnecessary spend while focusing on the patient experience and improving outcomes.

Management is headed by president and CEO Patrick Blair, who has been with the firm since 2021 and previously was Group President of Bayada Home Health Care and held various senior positions at Anthem.

The company’s primary offerings include:

Interdisciplinary care teams

Community-based care delivery model

Multi-modal approach.

According to a 2020 market research report by Mark Farrah Associates, the top five companies accounted for 47% of the U.S. Medicaid managed care market in 2019.

The top five companies were:

Anthem (ANTM)

Centene (CNC)

Molina (MOH)

UnitedHealth (UNH)

WellCare (WCG)

InnovAge’s Recent Financial Results

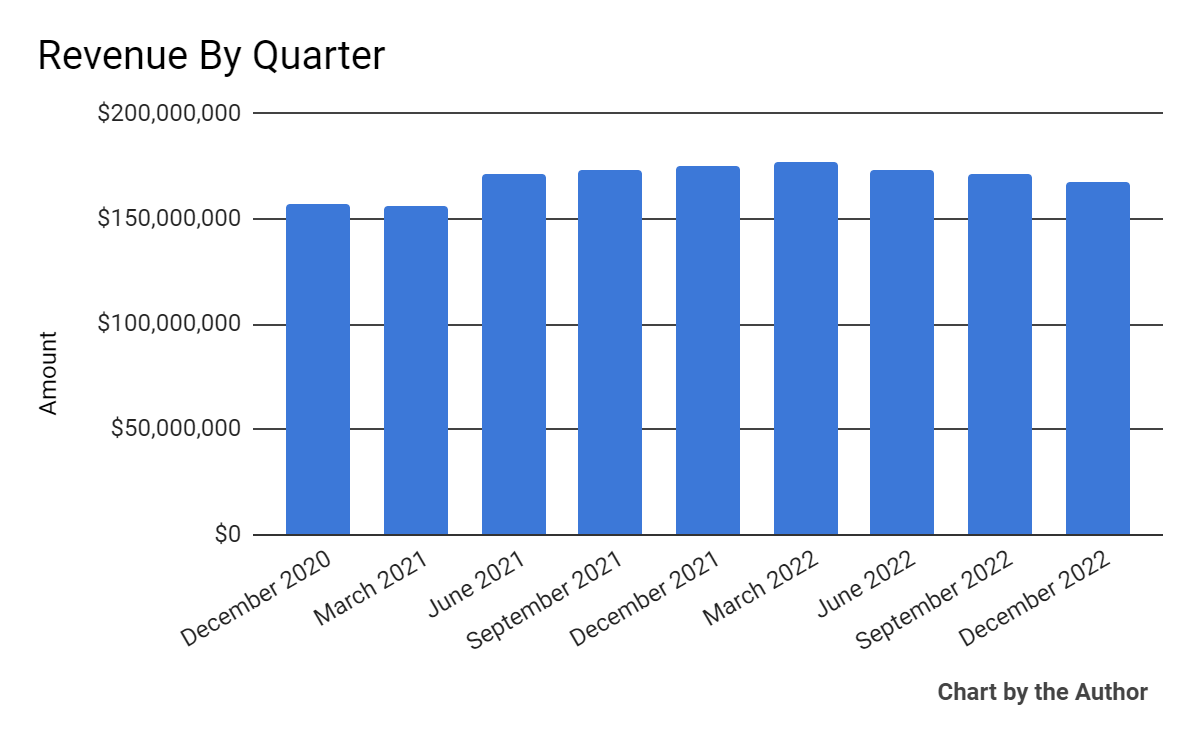

Total revenue by quarter has produced the following trajectory:

Total Revenue History (Seeking Alpha)

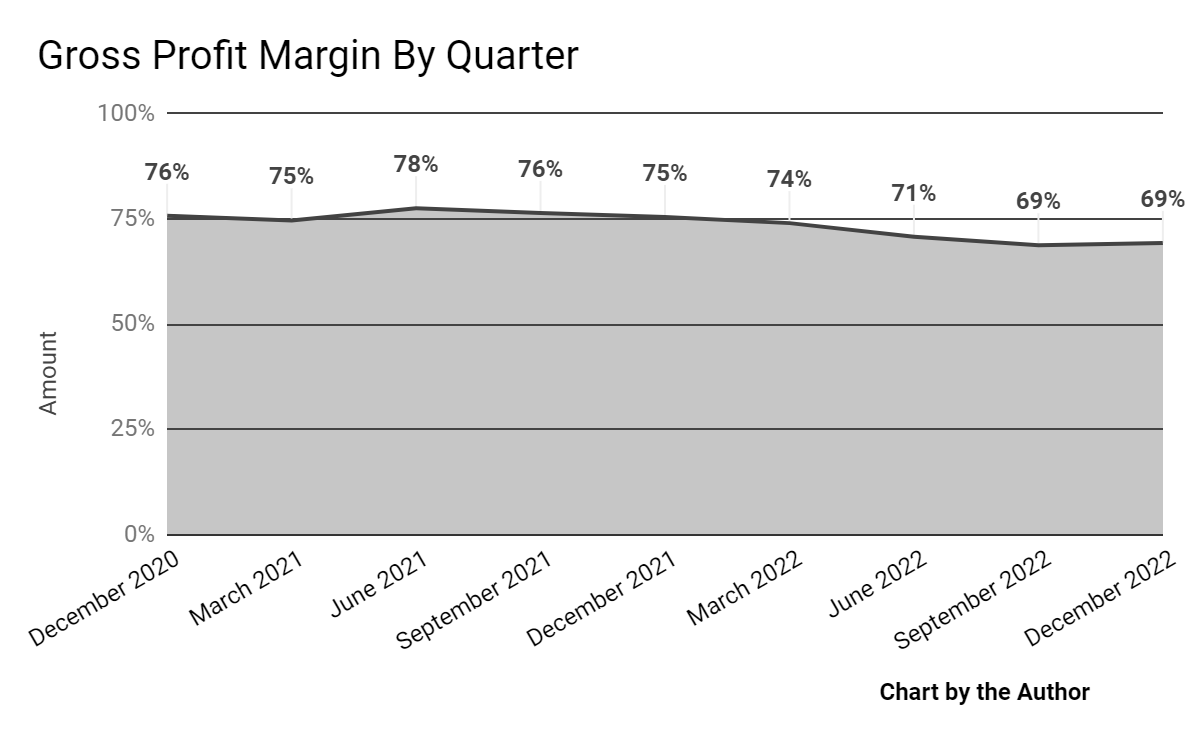

Gross profit margin by quarter has dropped in recent quarters:

Gross Profit Margin History (Seeking Alpha)

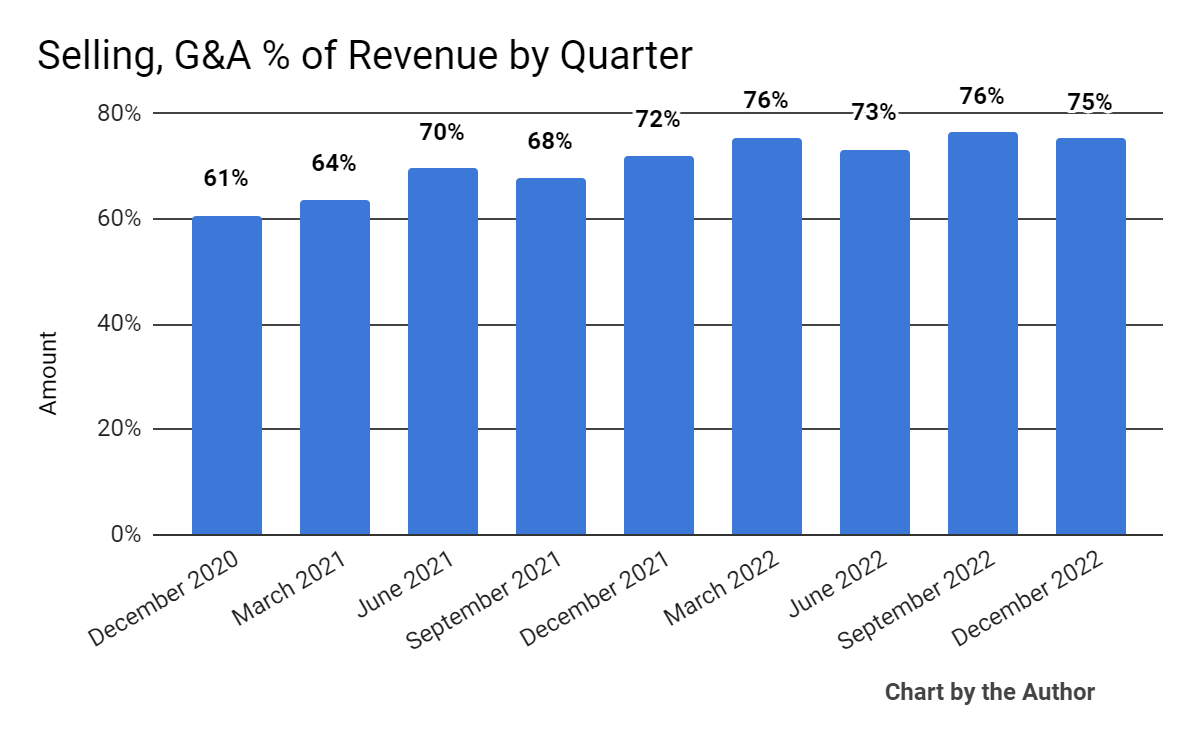

Selling, G&A expenses as a percentage of total revenue by quarter have increased recently, a negative trend:

Selling, G&A % Of Revenue History (Seeking Alpha)

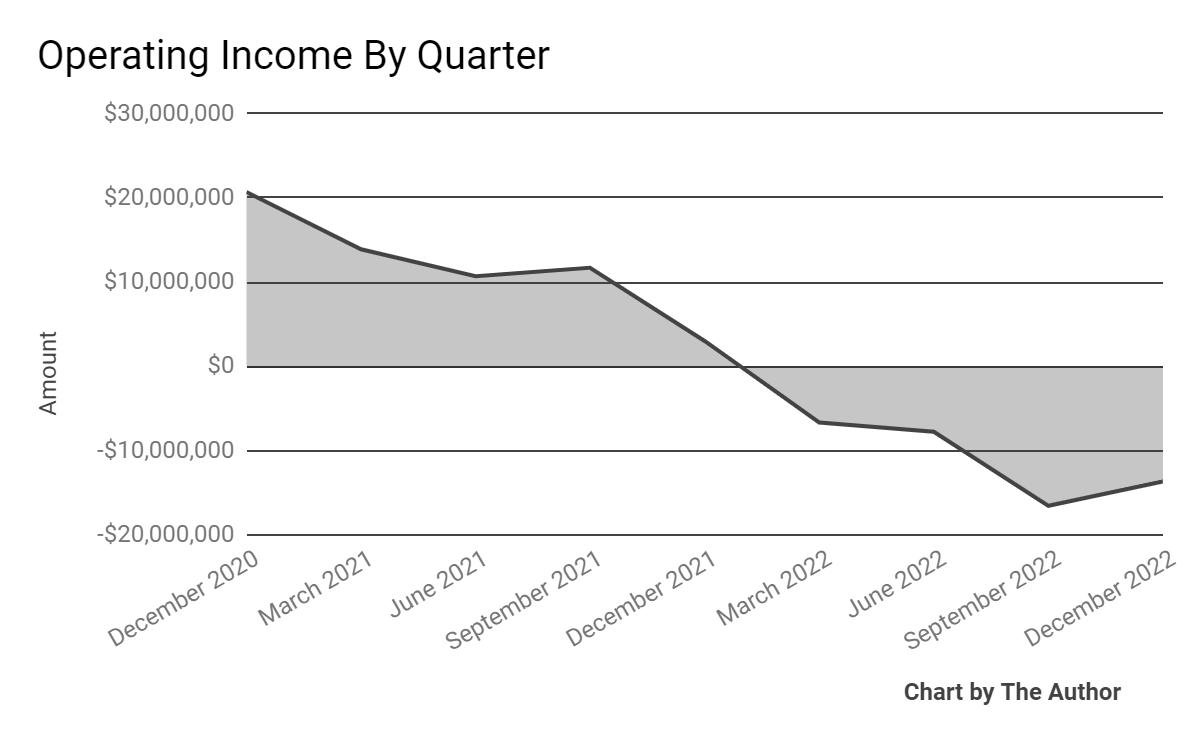

Operating income by quarter has worsened well into loss territory:

Operating Income History (Seeking Alpha)

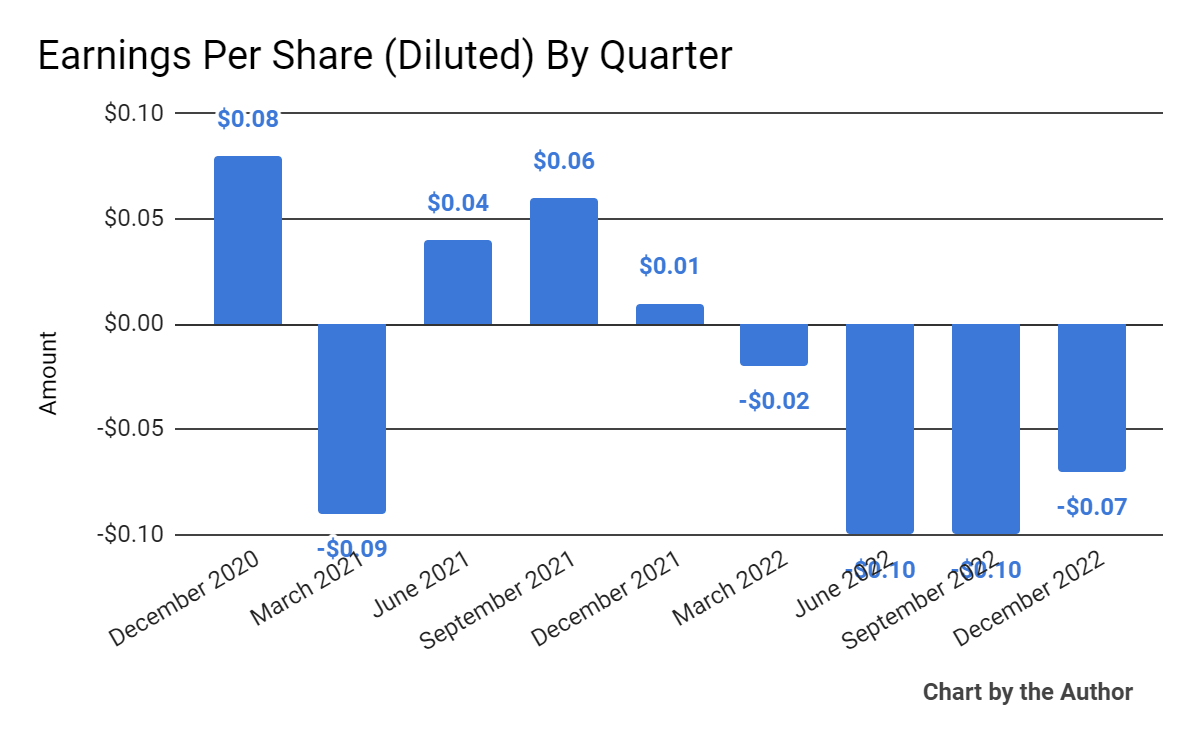

Earnings per share (Diluted) have also turned significantly negative:

Earnings Per Share History (Seeking Alpha)

(All data in the above charts is GAAP.)

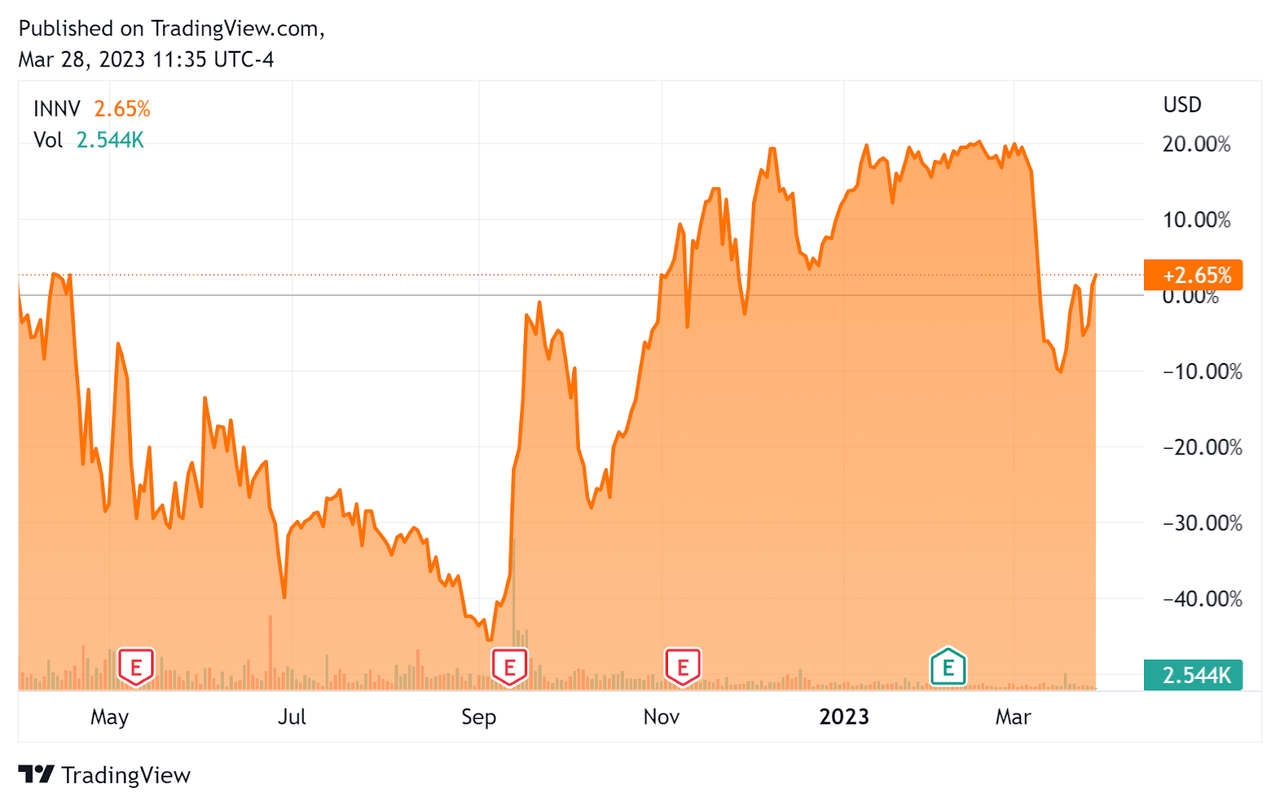

In the past 12 months, INNV’s stock price has risen 2.65%, as the chart indicates below:

52-Week Stock Price Chart (Seeking Alpha)

As to its FQ2 2023 financial results, total revenue fell 4.5% year-over-year and gross profit margin dropped 6 percentage points.

Selling, G&A as a percentage of total revenue rose 4.63%, a negative trend, while operating income worsened further into negative territory, generating a loss of $13.7 million for the quarter.

For the balance sheet, the firm ended the quarter with $144.9 million in cash, equivalents and short-term investments and $70.3 million in total debt.

Over the trailing twelve months, free cash used was $67.5 million, of which capital expenditures accounted for a hefty $41.2 million. The company paid only $4.3 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For InnovAge

Below is a table of relevant capitalization and valuation figures for the company:

Measure [TTM] | Amount |

Enterprise Value / Sales | 1.2 |

Enterprise Value / EBITDA | NM |

Price / Sales | 1.2 |

Revenue Growth Rate | 1.9% |

Net Income Margin | -5.6% |

GAAP EBITDA % | -4.4% |

Market Capitalization | $836,630,000 |

Enterprise Value | $818,430,000 |

Operating Cash Flow | -$26,270,000 |

Earnings Per Share (Fully Diluted) | -$0.29 |

(Source – Seeking Alpha.)

Future Prospects For InnovAge

In its last earnings call (Source – Seeking Alpha), covering FQ2 2023’s results, management highlighted the removal of enrollment restrictions in the state of Colorado, which represented 44% of the company’s total census as of the end of 2022.

In California, the firm was released from sanctions by the Federal CMS but is still awaiting a determination by the California Department of Healthcare Services.

In both instances, the company will need to continue to effect post-release corrective actions.

Looking ahead, management is focused on igniting “responsible growth” in its non-sanctioned markets, which to me means growth at a reasonable rate while trying to rebuild its sullied reputation.

The company’s financial position is still reasonably solid, although INNV has used a substantial amount of cash over the trailing twelve months and must reduce its use of cash in the future.

The primary risk to the company’s outlook is the uncertainty around receiving a release from new enrollment sanctions by the state of California, a large market for the firm.

A potential upside catalyst to InnovAge Holding Corp. stock could include news of such a release.

However, the company has a long road ahead of it for generating responsible growth, as CEO Patrick Blair characterizes it.

Until I see that growth start showing up in its financial results, along with a full California release of new enrollment sanctions, I’m on hold for InnovAge Holding Corp.

")

Finally Here")

")

{kind=link}