I recently caught up with a good friend of mine over coffee.

He ordered a medium black coffee. I ordered a hot latte with almond milk.

I’ve known him since he graduated from business school. He once worked as an intern for me.

One thing about him, he always had a big smile. But today, he looked glum and tired.

For years his hedge fund knocked the lights out and he was managing more than $1 billion.

But so far in 2023, Mr. Market has left him eating dust.

His approach is to only buy stocks when they’re trading at pennies on the dollar.

If it’s not a bargain, he won’t buy it.

And this year, there haven’t been many stocks trading at bargain prices.

This year, investors are caught up in “FOMO” (the fear of missing out).

A handful of stocks are soaring higher based on momentum.

Or to put it simply, they are buying them because they are going up.

Many companies that are trading at bargain prices haven’t moved.

And that’s why he’s underperforming the stock market.

One of his biggest investors was on his case about underperforming.

He started to explain how the stocks in his portfolio haven’t been moving … but the company’s fundamentals continue to soar higher.

The investor cut him off mid-sentence.

“What does the company have to do with whether or not the stock is going up?”

As if the company and the stock price have nothing to do with each other.

You could see why he was down in the dumps.

I told him I feel his pain … but cheer up, FOMO isn’t new.

I’ve seen this many times since I started my career on Wall Street in 1983.

I saw investors chase dot-com stocks in the late 1990s, and watched them bid up stocks to the moon in 2020.

I sat on the sidelines during both those times because valuations were nutso.

There were more companies trading at 100X earnings than you can shake a stick at.

From 2020 to 2021, there were dozens of companies that never made a nickel … that had market caps in the billions.

And it always ends poorly for investors following the herd.

It seems they forget that, at the end of the day, every stock ticker has a real business behind it.

And that the stock price follows the fundamentals of the business … not the other way around.

And now, here are the effects of FOMO — more obvious than in Big Tech companies like Nvidia.

Carried Away

This year, chipmaker Nvidia has been riding a wave of artificial intelligence hype to astronomical valuations. The stock is up more than 217% year to date:

(Click here to see Nvidia’s stock price surge up.)

Shares are now trading at around $465, with a total market capitalization of about $1 trillion.

Now let’s make believe we had $1 trillion. And we decide to use that money to buy the whole company at its present valuation.

What would our return be on our $1 trillion investment?

Well, that’s easy to calculate.

It would be all the company’s earnings, which over the past 12 months was around $5 billion.

So we would have invested, in our make-believe world, $1 trillion to earn $5 billion … or a .50% return.

Kind of silly considering a 90-day Treasury bill is yielding 5.50% … with zero risk.

That means investors paying $465 per share are saying: “I’m willing to get a one-half of 1% return on my money.” That’s a pretty low return considering the yield on Treasury bills.

This is what happens when you overlook a crucial fact of stock investing — that stocks are pieces of a business.

And when you buy a piece of a business, you have to have some idea what the business is worth. Or else you are flying blind.

Even if Nvidia hits all its guidance numbers over the next five years … the stock would still be way overvalued. Investors are paying a very expensive price for something that might happen in the future.

That’s not a game I play.

It’s times like these — when investors forget to ask “how much?” — that can be very dangerous for investors.

Because it’s so easy to give in to FOMO … to get sucked into paying huge valuations, since that’s what everyone else is doing.

It can be extremely hard to sit on your hands and be as selective as you need to be.

Overlooked Opportunity

While large-cap stocks have soared in 2023, a number of small- and microcap stocks are still trading at attractive prices.

And that’s because investors are throwing money at companies they are familiar with — regardless of valuations.

Meanwhile, microcaps — many of which are great businesses with outstanding founders/CEOs — are trading for pennies on the dollar.

When you can partner with a rock-star CEO and buy shares at an attractive price, it’s hard not to make money.

These smaller stocks are off the radar for big index funds. Most are even completely off-limits to Wall Street’s big investors.

Exactly like the one I talk about in a new presentation. You can watch it here.

Regards,

Charles Mizrahi

Founder, Alpha Investor

Real Estate: A Major Risk to China’s Economy

Yesterday I mentioned that inflation in China was dead on arrival … and that the country was actually flirting with deflation.

Well, let’s dig a bit deeper.

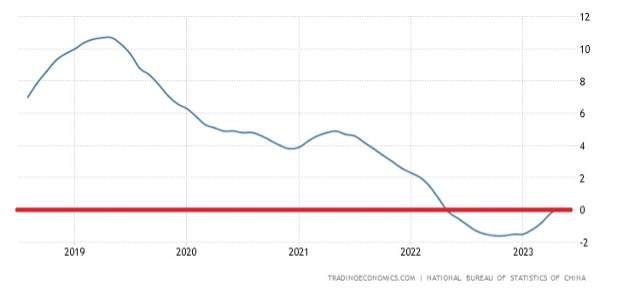

In China, as in the United States, housing is a major component in inflation statistics. And Chinese home prices have been decelerating since early 2019.

This predates the COVID-19 pandemic and has a lot more to do with the major overbuilding in the sector over the past 20 years. But the pandemic and its aftermath certainly didn’t help much.

At the beginning of 2019, Chinese home prices were appreciating at a 10% annual clip. Two years later, prices were still rising … but at a 4% rate. And by the second quarter of last year, prices actually fell.

Real Residential Property Prices in China

As of June 2023, Chinese property prices were flat, with prices unchanged over the previous year. But remember, we’re comparing to a lower base. Prices fell last year and have essentially stayed at those prices.

Property busts are absolutely devastating. Just think back to the 2008 meltdown and its aftermath. Falling property prices led to a wave of defaults on mortgages, which in turn led to a collapse of the banking system in the U.S. and Europe.

China’s economy has a much larger degree of state control than ours, so it is possible that it will avoid a 2008-style meltdown. But government decree cannot undo the laws of economics indefinitely.

Faced with declining home values, Chinese homeowners will be “trapped” in underwater mortgages. They will be less likely to upgrade their homes, buy furniture and appliances or do any of the infinite things that homeowners do to pour money into their homes. After all, why would you invest in a depreciating asset?

We’ll keep an eye on this. Because a hard landing in Chinese real estate is another major risk to the Chinese economy … which is in turn a major risk to the bottom line of America’s multinationals.

Regards, Charles SizemoreChief Editor, The Banyan Edge

Charles SizemoreChief Editor, The Banyan Edge

stay resilient towards tariff headwinds this yr?")

")

")

{kind=link}