panorios

We have previously covered General Motors (NYSE:GM) here as a post-FQ3’22-earnings article in November 2022. At that time, the company reported exemplary top and bottom-line growth QoQ and YoY in FQ3’22, due to its sustained gross margins of 14.1% against 14.4% in FQ3’21. These boosted its EPS to $2.25 against the consensus estimate of $1.88. However, the reduced FCF generation has also triggered a more prudent dividend payout for the quarter, potentially disappointing some investors.

For this article, we will focus on GM’s prospects in the near term, partly attributed to Tesla’s (TSLA) aggressive price cuts in early January. The latter’s move has directly impacted the automaker industry as a whole, due to the perceived fear of reduced profitability during the uncertain macroeconomics through 2023. The pessimism has naturally helped trigger the recent correction in the former’s price target by -14.8%. We shall discuss this further.

This Is Why Mr. Market Has Discounted GM’s Forward Execution

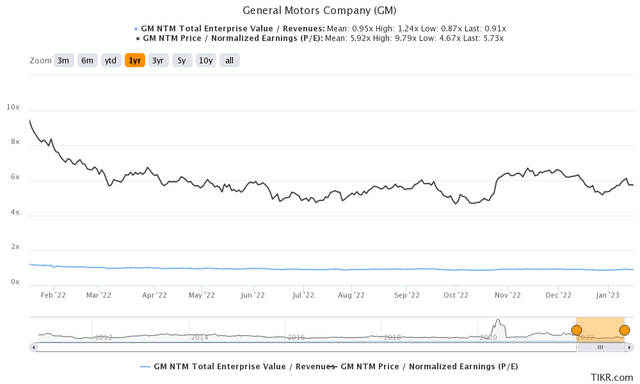

GM 1Y EV/Revenue and P/E Valuations

S&P Capital IQ

GM is currently trading at an EV/NTM Revenue of 0.91x and NTM P/E of 5.73x, lower than its 3Y pre-pandemic mean of 0.94x and 6.21x, respectively. Otherwise, it is still lower than its 1Y mean of 0.95x and 5.92x, respectively.

GM 1Y Stock Price

Seeking Alpha

Based on GM’s projected FY2024 EPS of $6.01 and current P/E valuations, we are looking at a moderate price target of $34.43. Market analysts are naturally more bullish at $43, suggesting a notable 18% upside potential from current levels. This optimism is unsurprising indeed, since the stock is currently trading at a historically low P/E valuation, indicating Mr. Market’s bearish sentiments.

However, the pessimism is warranted for now in our view, with TSLA throwing a curve ball on 13 January 2023. The latter has drastically slashed the prices of its vehicles sold in the US to qualify for the Inflation Reduction Act’s $7.5K tax rebates from 2023 onwards. Analyst, Daniel Ives of Wedbush, said:

This is a clear shot across the bow at European automakers and U.S. stalwarts (GM and Ford) that Tesla is not going to play nice in the sandbox with an EV price war now underway. Margins will get hit on this, but we like this strategic poker move by Musk and Tesla. (NPR)

TSLA’s Model Y and Model 3 now cost $52.99K and $43.99K, respectively, suggesting a drastic -19.6% and -6.4% decrease from 2022 prices of $65.99K and $46.99K. Then again, we must highlight that the automaker has also hiked the MSRP several times attributed to the rising inflationary pressures, against 2019 prices of $39K and $36.2K, respectively.

However, the market trend is not promising either, with the December CPI showing a deceleration in the new vehicle index at -0.1%, compared to 0.0% in November and 0.4% in October 2022. This is probably due to the elevated interest rates reducing the affordability of vehicles, despite the increased availability of vehicles as the global supply chain eases and automakers ramp up production.

More auto consumers in the US are paying over $1K on their monthly auto loans, attributed to the elevated interest rates of 6.5% for new autos by December 2022, compared to 4.1% in late 2021. While the group may be capped at 15% now, it is apparent that the trend is consistent, with average monthly payments for new autos growing to $717 by the end of 2022, compared to $617 in 2021 and $525 in 2018.

Notably, the average down payment for new autos has also risen to $6.78K by the end of 2022, compared to $6.02K in Q2’22 and $4.74K in Q1’21. With the Feds set to raise interest rates to over 5% by mid-2023 and a pivot only from 2024 onwards, it is no wonder market analysts appear bearish about the whole automotive market as a whole.

As A Result, Will GM Also Slash Its MSRP?

This is the most important question indeed, though our best guess is unlikely. This is why. GM just raised prices for the 2023 Chevy Bolt EV by $600 to $27.8K on 03 January 2023, likely attributed to its eligibility for the full $7.5K tax credit, instead of the original $3.75K.

However, this number is reflective of the management’s effort in offering the best value, since it is notably cheaper by -$3.7K compared to the 2022 model, -$8.7K to the 2021 model, and -$9.7K to the original launch in 2017. As the model remains the cheapest EV available in the US, this naturally improves the company’s chances of success at a time of tightened discretionary spending. On the other hand, it remains to be seen how the model will affect market sentiments, as the company is only planning to ramp up production to 70K units annually in 2023.

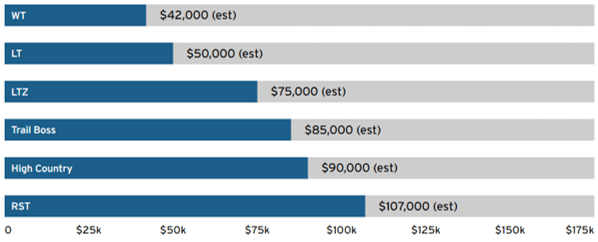

GM’s Silverado EV Introductory Price Range

Car&Driver

GM’s price hikes for other models have also matched industry trends thus far, similar to its peers such as TSLA and Ford (F). The former’s flagship truck, Chevy Silverado EV, was originally launched with an MSRP of $42K, naturally pointing to the entry-level Work Trim [WT].

However, recent announcements have shown that the 3WT will start from $72.9K and the 4WT from $77.9K onwards, with the WT not being available until later. Notably, these numbers will place it nearer to the mid-level LTZ at the previous estimated MSRP of $75K or the RST (high-end fully loaded) version at $107K.

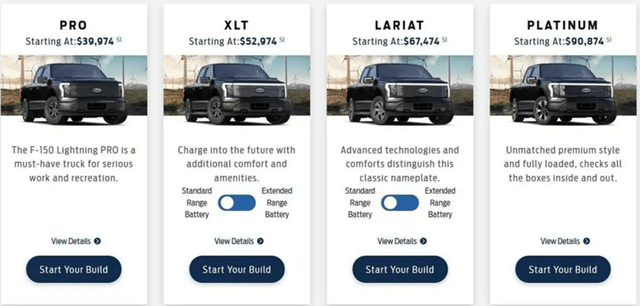

F’s F-150 Lightning Introductory Price Range

insideevs

These numbers are not too far off from F’s F-150 Lightning entry-level version as well, which has been raised by 40.1% from the introductory debut price of $40K to $56K by December 2022. The company has also raised XLT, its mid-trim level to $66.01K (+24.6%), with the Platinum, top-trim level going at $97.81K (+7.6%) now.

In addition, GM has raised its Hummer EV prices by $6.25K from the original range between $79.99K and $99.99K. These raises are naturally attributed to the rising inflationary pressure across labor and material costs, similarly experienced by many other automakers.

On one hand, GM management has been highly competent in offering EVs across different price points, to cater to a wide group of loyal fans with various spending powers. Its long-term prospects also look robust, therefore, especially if the Fed achieves its target inflation rate of 2% by mid-2024. Market analysts expect the company to deliver FY2025 revenues of $169.25B and EPS of $6.69, suggesting a decent CAGR of 7.4% and -1.4%, respectively.

However, we cannot deny that there may be some recessionary pressures through 2023, with interest rates remaining elevated in the short term. While existing reservations will still be honored accordingly, it is not hard to see why future consumer demand may temporarily taper off. These may potentially trigger more headwinds to GM’s stock valuations, significantly worsened by a potential price war.

While GM’s 2022 deliveries have been excellent, its profit margins have also been compressed. The company reported automotive gross margins of 11.3% and automotive operating margins of 4.3% over the past three quarters, against TSLA’s market-leading automotive gross margins of 29.5% at the same time.

It is apparent that GM’s financial segment has been the star of the show, contributing operating margins of 33.2% then, boosting the company’s total operating margins to 8.8%, against TSLA’s total operating margins of 17.1%. Therefore, it is unsurprising that market analysts are growingly concerned about the former’s next move, since a price cut may naturally impact its already tight automotive margins.

Therefore, we prefer to rate the GM stock as a Hold for now, due to the potential volatility ahead. In the meantime, since the company is slated to announce its FQ4’22 earnings on January 31, 2023, it would be prudent to hear more from the management as well.

")

")

{kind=link}