Monty Rakusen

Friedman Industries (NYSE:FRD) 1Q25 outcomes had been according to our expectations of flat to decrease processing. The working revenue harm from decrease scorching rolled coil costs was offset by hedging.

The quarter confirms our learn of costs not affecting long-term earnings an excessive amount of, with extra significance given to volumes, which haven’t grown. Nevertheless, as of June 2024, Friedman had not hedged its bets, and coil costs have been growing, which is able to in all probability result in a worthwhile 2Q25.

Total, the valuation stays unattractive, contemplating the corporate’s long-term manufacturing capability and common profitability. I keep my Maintain ranking.

1Q25 in line

Manufacturing flat to down: A very powerful issue for Friedman’s long-term profitability is manufacturing volumes. The corporate has a processing enterprise, the place costs up or down in metal coil cancel between quarters or between working and hedge revenue.

1Q25 manufacturing was disappointing, decrease than within the earlier quarter, at a complete of 133 thousand tons processed. This compares with 143 thousand tons in 1Q24. Since 1Q24, when the corporate’s Sinton facility began working and the corporate added capability from Mitsubishi, manufacturing volumes have remained within the 130 to 140 thousand ton space.

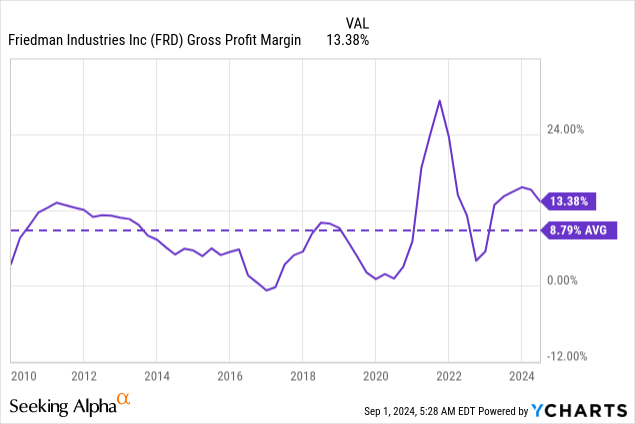

Decrease costs hedged: The corporate posted working losses for the quarter, as its gross margins contracted from 21% to about 16% this quarter. This was attributable to hot-rolled coil costs contracting by 40% from the start to the tip of the quarter. Nevertheless, the corporate recorded $5.4 million in hedging positive aspects, resulting in pre-tax earnings that, albeit a lot decrease than final 12 months (1/3), had been nonetheless constructive at $3.2 million. This additionally confirms my view that costs variations don’t make such an enormous deal in Friedman’s profitability.

OpEx enhance: Way more regarding was the increment in processing and warehousing bills (25% YoY), and deliveries (10% YoY). These bills mustn’t transfer with coil costs, and subsequently represent a greater approximation to Friedman’s true overhead. These prices had been offset by decrease G&A (-25%). In whole, overhead ex-CoGS was up 4.5% or about a million. At post-GFC common gross margins of 9%, this requires an extra $10 million in income, or about 10 thousand tons of processing at a value of about $900 per ton. As well as, you need to keep in mind that SG&A has labored as a variable expense in my earlier mannequin however is now growing even with revenues and volumes down.

2Q25 unhedged positive aspects: Trying on the firm’s 10-Q for 1Q25, we are able to observe that it left Q1 with out hedged positions. It was quick, solely 280 tons of scorching rolled coil. Which means that the corporate will profit extra from costs shifting positively between July and September (its inventories shall be bought at a better value later as completed product). We are able to observe that HRC futures began July at $650 and at the moment are buying and selling at about $714, with a peak just a few weeks in the past at $750. This may in all probability report an accrual gross margin achieve.

Valuation stays unattractive

In my earlier article, I proposed a mannequin from which I forecasted that Friedman’s long-term working earnings would hover round $20 million per 12 months or $15 million in NOPAT. As of at the moment, the corporate has an EV of about $150 million or an EV/NOPAT of 10x.

Available on the market cap facet, the corporate trades at about $105 million. In my mannequin, based mostly on each return on property minus value of debt, and working revenue minus common curiosity, I anticipated the corporate to provide internet revenue of $10 million. Once more, the a number of is round 10x.

I don’t imagine these multiples are extreme, however they’re undoubtedly not opportunistic. At present, there are a lot of firms buying and selling at comparable present yields with higher prospects for growing manufacturing and fewer commoditized merchandise.

For my part, Friedman isn’t a possibility at these costs, however I’ll proceed to observe the inventory for potential deeps (particularly if an unhedged place causes a better than anticipated operational loss).

{kind=link}