Published on October 19th, 2022 by Bob Ciura

Income investors are likely familiar with the Dividend Aristocrats, a select group of 65 stocks in the S&P 500 Index that have increased their dividends for at least 25 consecutive years.

But there is an even bigger group of stocks that have also raised their dividends for at least 25 years, known as the Dividend Champions. There are nearly 150 Dividend Champions right now.

The main difference between the two groups is that the Dividend Aristocrats are subject to additional criteria such as market capitalization, daily trading volume, and more. In addition, the Dividend Aristocrats must be members of the S&P 500 Index.

Therefore, there are more high-quality dividend growth stocks to choose from among the Dividend Champions.

You can download your free copy of the Dividend Champions list, along with relevant financial metrics like price-to-earnings ratios, dividend yields, and payout ratios, by clicking on the link below:

High yield Dividend Champions like the 10 on this list, could be appealing choices for investors looking to increase their income. For example, retirees looking for replacement income could consider high yield Dividend Champions.

This article will discuss the top 10 high yielding Dividend Champions, ranked according to dividend yields in the Sure Analysis Research Database.

Each of the high yield Dividend Champions below has a current yield above 5%, and has increased its dividend for at least 25 consecutive years.

Table of Contents

You can instantly jump to any specific section of the article by clicking on the links below:

High Yield Dividend Champion #10: Leggett & Platt (LEG)

Leggett & Platt is an engineered products manufacturer. The company’s products include furniture, bedding components, store fixtures, die castings, and industrial products. Leggett & Platt has 14 business units and more than 20,000 employees. The company qualifies for the Dividend Kings as it has 50 years of consecutive dividend increases.

In the 2022 second quarter, revenue of $1.33 billion rose 4.7% year-over-year. Earnings-per-share of $0.70 beat estimates by a penny. The company lowered full-year guidance, now expecting sales in a range of $5.2 billion to $5.4 billion, and earnings-per-share of $2.65 to $2.80 for 2022.

Click here to download our most recent Sure Analysis report on Leggett & Platt (preview of page 1 of 3 shown below):

High Yield Dividend Champion #9: International Business Machines (IBM)

IBM is a global information technology company that provides integrated enterprise solutions for software, hardware, and services. IBM’s focus is running mission critical systems for large, multi-national customers and governments. IBM typically provides end-to-end solutions.

The company now has four business segments: Software, Consulting, Infrastructure, and Financing. IBM had annual revenue of ~$57.4B in 2021 (not including Kyndryl).

IBM reported solid results for Q2 2022 on July 18th, 2022. Company-wide revenue increased 16% while diluted adjusted earnings per share rose 43% to $2.31 on a year-over-year basis. Diluted GAAP earnings per share rose 79% to $1.61 in the quarter from $0.90 in the prior year.

Revenue for Software increased 12% due to 9% growth in Hybrid Platform & Solutions and a 19% increase in Transaction Processing. Revenue was up 17% for RedHat, 8% for Automation, 4% for Data & AI, and 5% for Security. Consulting revenue increased 18%. The book-to-bill ratio is a healthy 1.1X.

Click here to download our most recent Sure Analysis report on IBM (preview of page 1 of 3 shown below):

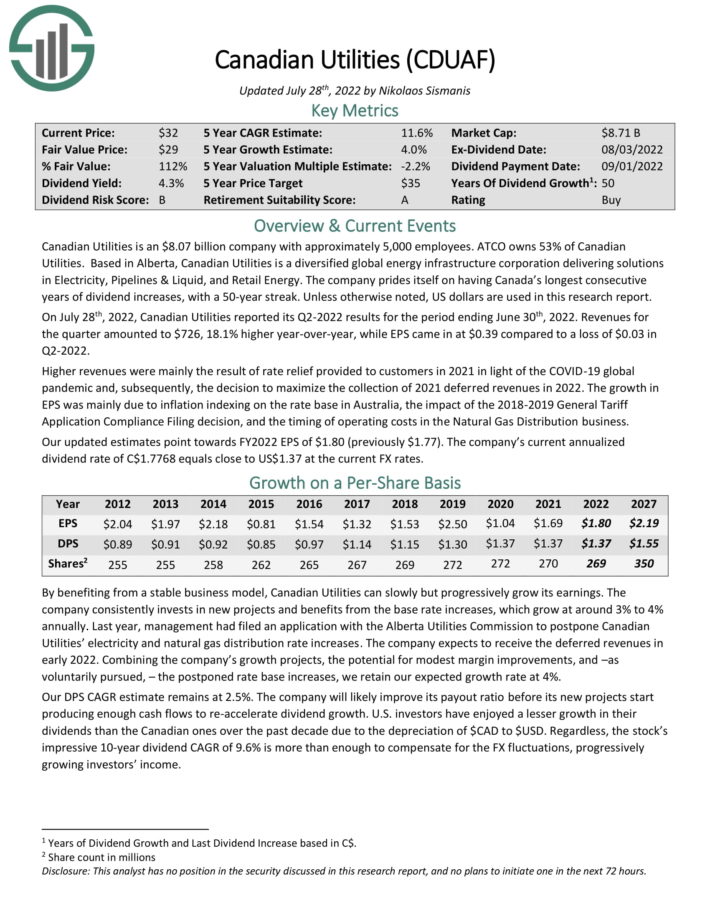

High Yield Dividend Champion #8: Canadian Utilities (CDUAF)

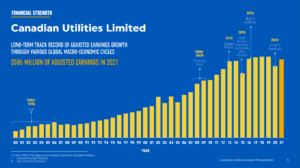

Canadian Utilities is a utility stock with approximately 5,000 employees. ATCO owns 53% of Canadian Utilities. Based in Alberta, Canadian Utilities is a diversified global energy infrastructure corporation delivering solutions in electricity, pipelines & liquid, and retail energy.

The company has a long history of generating steady growth and consistent profits through the economic cycle.

Source: Investor Presentation

On July 28th, 2022, Canadian Utilities reported its Q2-2022 results for the period ending June 30th, 2022. Revenue for the quarter amounted to $726, 18.1% higher year-over-year, while EPS came in at $0.39 compared to a loss of $0.03 in Q2-2022. Higher revenue was mainly the result of rate relief provided to customers in 2021 in light of the COVID-19 global pandemic and, subsequently, the decision to maximize the collection of 2021 deferred revenues in 2022.

The company’s competitive advantage lies in the moat surrounding regulated utilities. With no easy entry into the sector, regulated utilities enjoy an oligopolistic market with little competition threat. The company’s resiliency has been proven decade after decade.

Another competitive advantage is the company’s strong financial position. CDUAF has investment-grade credit ratings of BBB+ from Standard & Poor’s and A- from Fitch. This allows the company to raise capital at attractive terms.

Click here to download our most recent Sure Analysis report on Canadian Utilities (preview of page 1 of 3 shown below):

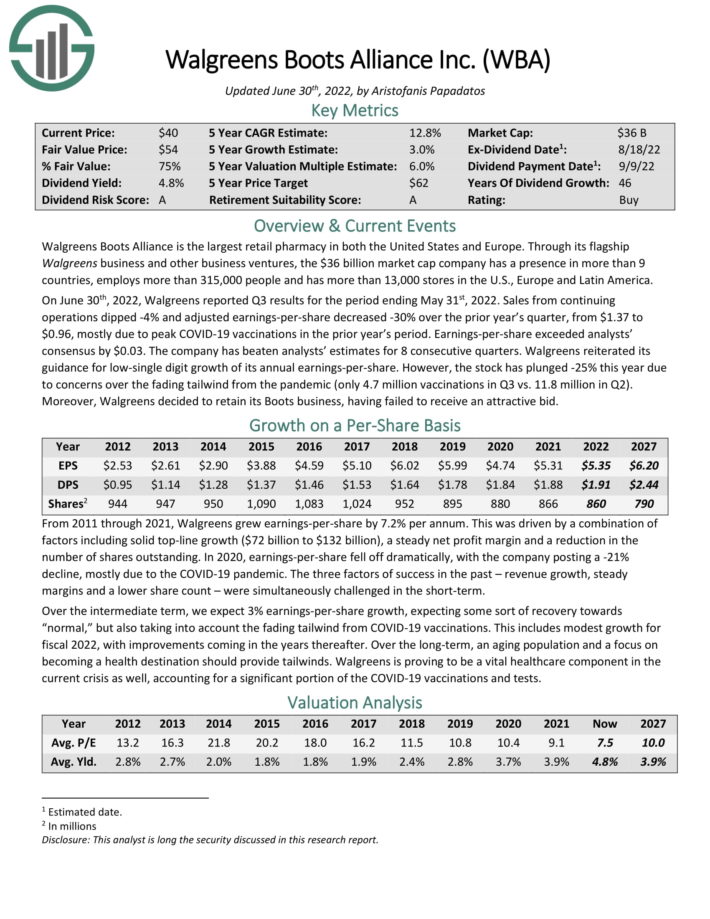

High Yield Dividend Champion #7: Walgreens Boots Alliance (WBA)

Walgreens Boots Alliance is the largest retail pharmacy in both the United States and Europe. Through its flagship Walgreens business and other business ventures, the company employs more than 325,000 people and has more than 13,000 stores.

On June 30th, 2022, Walgreens reported Q3 results for the period ending May 31st, 2022. Sales from continuing operations dipped -4% and adjusted earnings-per-share decreased -30% over the prior year’s quarter, from $1.37 to $0.96, mostly due to peak COVID-19 vaccinations in the prior year’s period.

Source: Investor Presentation

Earnings-per-share exceeded analysts’ consensus by $0.03. The company has beaten analysts’ estimates for 8 consecutive quarters.

Walgreens reiterated its guidance for low-single digit growth of its annual earnings-per-share.

Click here to download our most recent Sure Analysis report on Walgreens (preview of page 1 of 3 shown below):

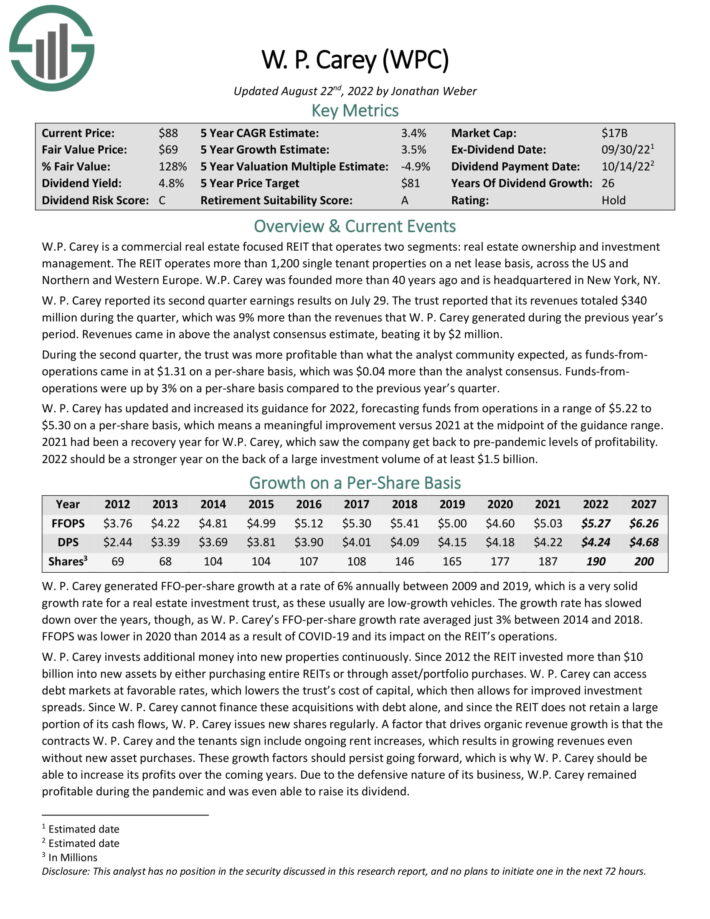

High Yield Dividend Champion #6: W.P. Carey (WPC)

W.P. Carey is a commercial real estate focused REIT that operates two segments: real estate ownership and investment management. The REIT operates more than 1,200 single tenant properties on a net lease basis, across the US and Northern and Western Europe.

W. P. Carey reported its second quarter earnings results on July 29. The trust reported that its revenues totaled $340 million during the quarter, which was 9% more than the revenues that W. P. Carey generated during the previous year’s period. Revenues came in above the analyst consensus estimate, beating it by $2 million.

During the second quarter, the trust was more profitable than what the analyst community expected, as funds-from operations came in at $1.31 on a per-share basis, which was $0.04 more than the analyst consensus. Funds-from operations were up by 3% on a per-share basis compared to the previous year’s quarter.

W. P. Carey has updated and increased its guidance for 2022, forecasting funds from operations in a range of $5.22 to $5.30 on a per-share basis, which means a meaningful improvement versus 2021 at the midpoint of the guidance range.

Click here to download our most recent Sure Analysis report on WPC (preview of page 1 of 3 shown below):

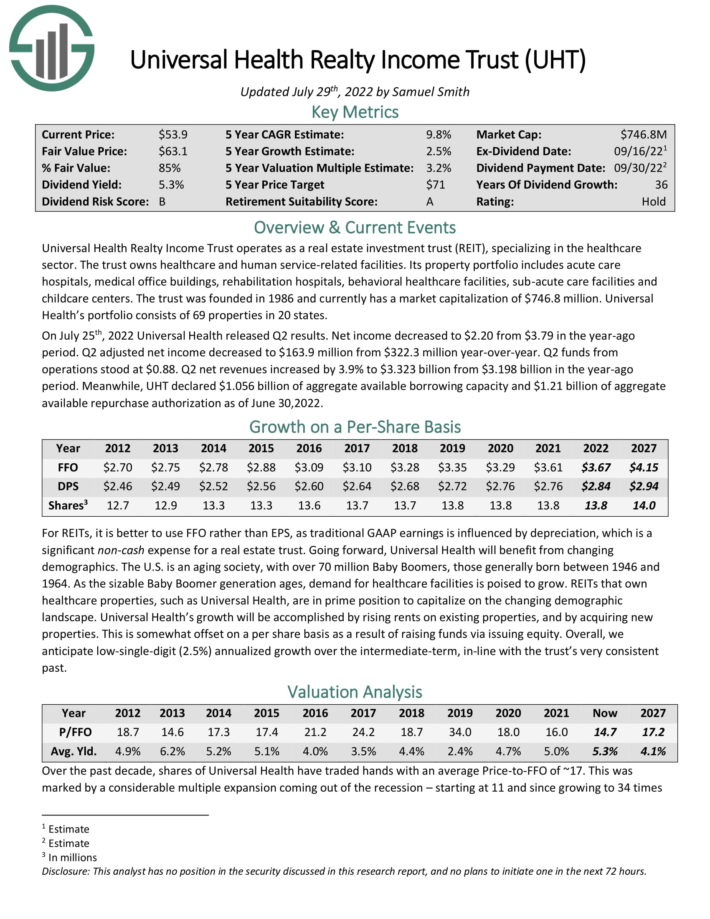

High Yield Dividend Champion #5: Universal Health Realty Income Trust (UHT)

Universal Health Realty Income Trust operates as a real estate investment trust (REIT), specializing in the healthcare sector. The trust owns healthcare and human service-related facilities. Its property portfolio includes acute care hospitals, medical office buildings, rehabilitation hospitals, behavioral healthcare facilities, sub-acute care facilities and childcare centers. Universal Health’s portfolio consists of 69 properties in 20 states.

On July 25th, 2022 Universal Health released Q2 results. Net income decreased to $2.20 from $3.79 in the year-ago period. Q2 adjusted net income decreased to $163.9 million from $322.3 million year-over-year. Q2 funds from operations stood at $0.88. Q2 net revenues increased by 3.9% to $3.323 billion from $3.198 billion in the year-ago period. Meanwhile, UHT declared $1.056 billion of aggregate available borrowing capacity and $1.21 billion of aggregate available repurchase authorization as of June 30,2022.

Click here to download our most recent Sure Analysis report on UHT (preview of page 1 of 3 shown below):

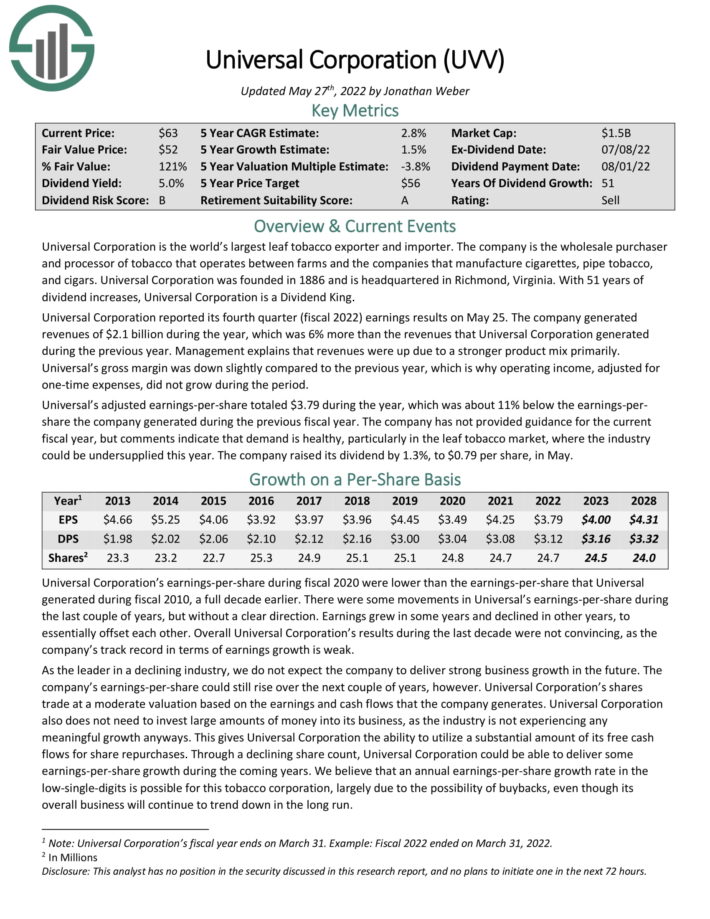

High Yield Dividend Champion #4: Universal Corp. (UVV)

Universal Corporation is a tobacco stock. It is the world’s largest leaf tobacco exporter and importer. The company is the wholesale purchaser and processor of tobacco that operates as an intermediary between tobacco farms and the companies that manufacture cigarettes, pipe tobacco, and cigars. Universal also has an ingredients business that is separate from the core leaf segment.

In the most recent quarter, revenue was up 23% year-over-year, while cost of goods rose 22%. That meant gross margins rose 70 basis points to 18.5% of revenue, and adjusted operating income was up 5% to $13.3 million. Ingredients revenue soared 46% higher year-over-year due mostly to the company’s 2021 acquisition of Shank’s Extracts.

Source: Investor Presentation, page 26

As the leader in a declining industry, we do not expect the company to deliver strong growth in the future. The company’s earnings-per-share could still rise over the next couple of years, however. Universal’s shares trade at a moderate valuation based on the earnings and cash flows that the company generates.

Universal also does not need to invest large amounts of money into its business, which gives it the ability to utilize a substantial amount of its free cash flows for share repurchases and dividends.

With a dividend payout of ~79% for the current fiscal year, we view Universal’s dividend as moderately safe, with the caveat that the company faces headwinds due to the steady decline of the tobacco industry.

Click here to download our most recent Sure Analysis report on Universal (preview of page 1 of 3 shown below):

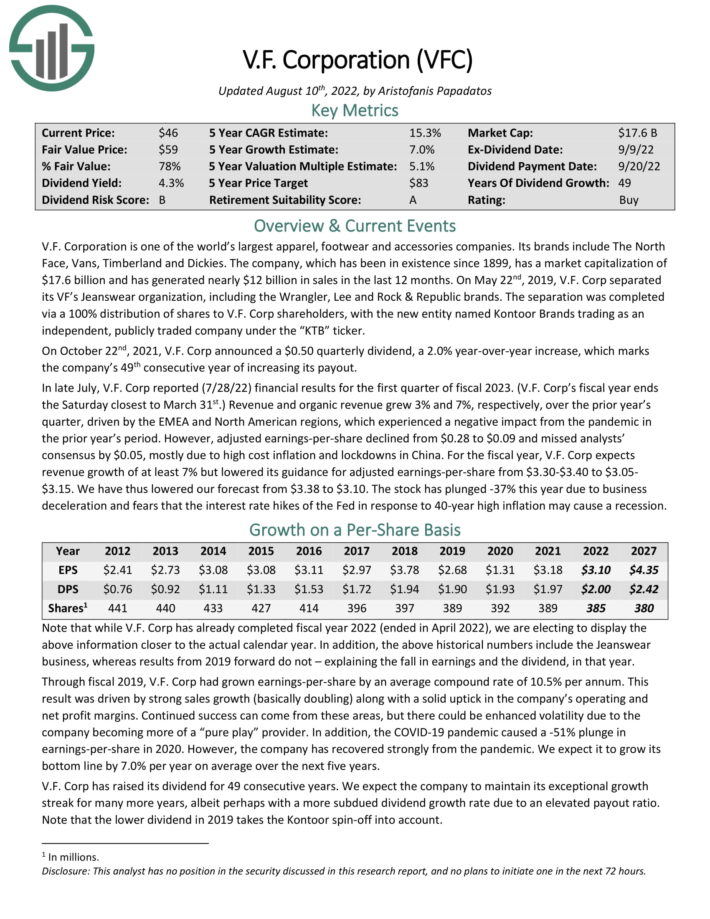

High Yield Dividend Champion #3: V.F. Corp. (VFC)

V.F. Corporation is one of the world’s largest apparel, footwear and accessories companies. The company’s brands include The North Face, Vans, Timberland and Dickies. The company, which has been in existence since 1899, generated over $11 billion in sales in the last 12 months.

In late July, V.F. Corp reported (7/28/22) financial results for the fiscal 2023 first quarter. Revenue of $2.26 billion rose 3.2% year over year and beat analyst estimates by $20 million. The North Face brand led the way with 37% currency-neutral revenue growth in the quarter.

However, inflation took its toll on margins and profits. Gross margin of 53.9% for the quarter declined 260 basis points, while operating margin of 2.8% declined 640 basis points. As a result, adjusted EPS declined 68% to $0.09 per share.

Adjusted earnings-per-share grew 67%, from $0.27 to $0.45, but missed analysts’ consensus by $0.02. For the new fiscal year, V.F. Corp expects revenue growth of at least 7% and adjusted earnings-per-share of $3.30 to $3.40.

Click here to download our most recent Sure Analysis report on V.F. Corp. (preview of page 1 of 3 shown below):

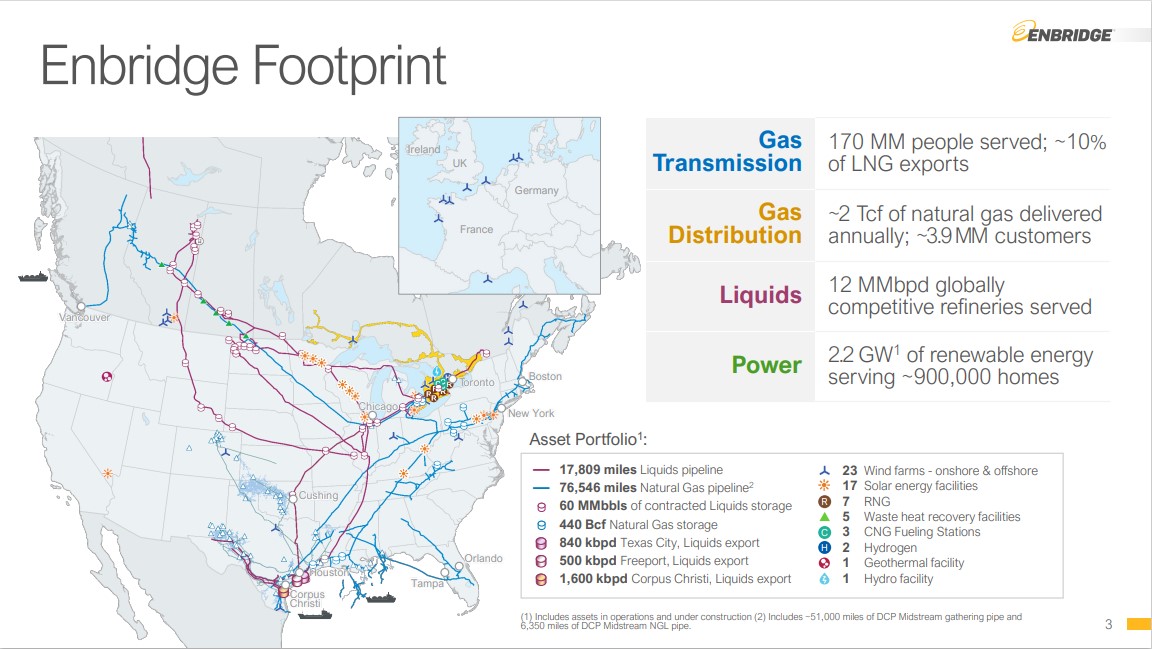

High Yield Dividend Champion #2: Enbridge Inc. (ENB)

Enbridge is an oil & gas company that operates the following segments: Liquids Pipelines, Gas Distributions, Energy Services, Gas Transmission & Midstream, and Green Power & Transmission. Enbridge bought Spectra Energy for $28 billion in 2016 and has become one of the largest midstream companies in North America.

Source: Investor Presentation

Enbridge reported its second quarter earnings results on July 29. During the quarter, Enbridge still managed to grow its adjusted EBITDA by 12% year over year, to CAD$3.7 billion, up from CAD$3.3 billion during the previous year’s quarter. This was possible thanks to stronger contributions from the liquids pipelines segment primarily.

Enbridge was able to generate distributable cash flows of US$2.1 billion, or US$1.04 on a per-share basis, which was up by 10% year over year in CAD. Enbridge is forecasting distributable cash flows in a range of USD$4.12 at the midpoint of the guidance range, which would easily be a new record for the company.

Enbridge raised its dividend by 3% (in CAD), which was the 27th yearly dividend increase in a row. High yield Dividen Champions like Enbridge are appealing due to their annual dividend growth, even during recessions. This is especially rare for the oil and gas industry, which is cyclical by nature.

Click here to download our most recent Sure Analysis report on Enbridge (preview of page 1 of 3 shown below):

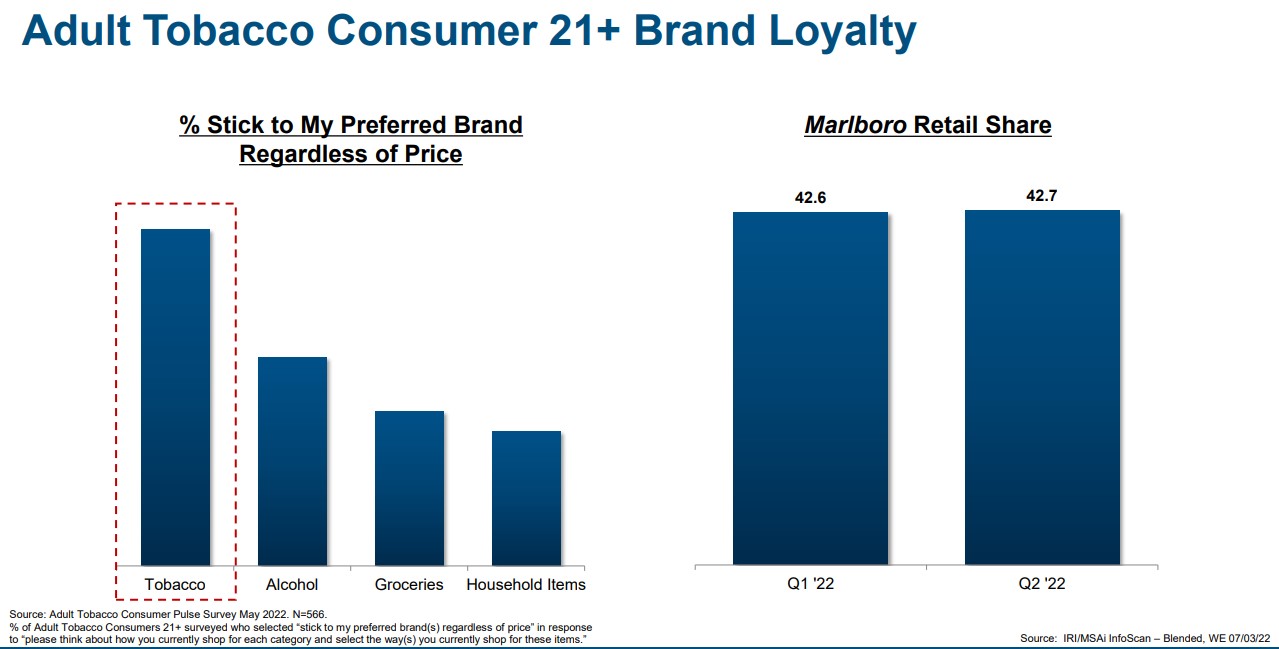

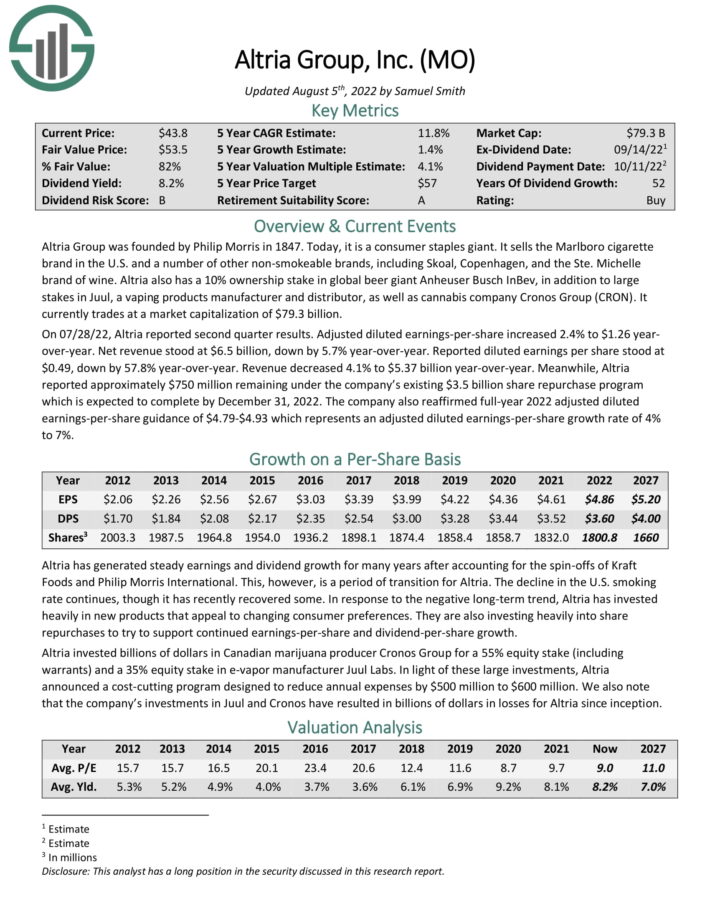

High Yield Dividend Champion #1: Altria Group (MO)

Altria Group was founded by Philip Morris in 1847. Today, it is a consumer staples giant. It sells the Marlboro cigarette brand in the U.S. and a number of other non-smokeable brands, including Skoal and Copenhagen.

The flagship brand continues to be Marlboro, which holds over 40% retail market share in the U.S.

Source: Investor Presentation

Altria also has a 10% ownership stake in global beer giant Anheuser-Busch InBev, in addition to large stakes in Juul, a vaping products manufacturer and distributor, as well as cannabis company Cronos Group (CRON).

Related: 2022 Marijuana Stocks List | The Best Marijuana Stocks To Invest In Now

On 07/28/22, Altria reported second quarter results. Adjusted diluted earnings-per-share increased 2.4% to $1.26 yearover-year. Net revenue stood at $6.5 billion, down by 5.7% year-over-year. Reported diluted earnings per share stood at $0.49, down by 57.8% year-over-year. Revenue decreased 4.1% to $5.37 billion year-over-year.

Meanwhile, Altria reported approximately $750 million remaining under the company’s existing $3.5 billion share repurchase program which is expected to complete by December 31, 2022. The company also reaffirmed full-year 2022 adjusted diluted earnings-per-share guidance of $4.79-$4.93 which represents an adjusted diluted earnings-per-share growth rate of 4% to 7%.

Altria takes the #1 spot among high yield Dividend Champions, as it has a current yield above 8%. With a target dividend payout ratio of 80% of its annual adjusted EPS, the dividend appears safe.

Click here to download our most recent Sure Analysis report on Altria Group (preview of page 1 of 3 shown below):

Final Thoughts & Additional Reading

High yield Dividend Champions are attractive for income investors, not just for their high yields, but also for their long track records of growing their dividends. Still, investors should assess each of the high yield Dividend Champions before buying. That said, these 10 high yield Dividend Champions appear to have safe dividends.

The high yield Dividend Champions list is not the only way to quickly screen for stocks that regularly pay rising dividends.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

")

{kind=link}