Updated on January 26th, 2023 by Jonathan Weber

At Sure Dividend, we often talk about the merits of the Dividend Aristocrats. We believe this exclusive group of stocks broadly has strong brands, consistent profits even during recessions, and durable competitive advantages. These qualities allow the Dividend Aristocrats to raise their dividends every year, regardless of the state of the economy.

Of the 500 stocks comprising the S&P 500 Index, just 68 qualify as Dividend Aristocrats. You can download a copy of the full list of all 68 Dividend Aristocrats, complete with metrics like dividend yields and P/E ratios, by clicking on the link below:

Each year, we individually review all the Dividend Aristocrats. The next in the series is Illinois Tool Works (ITW). Illinois Tool Works has a long history of dividend growth even through recessions, which is especially impressive given the cyclical nature of its business model. This article will discuss the major factors for Illinois Tool Works’ long dividend history.

Business Overview

Illinois Tool Works has been in business for more than 100 years. It started out all the way back in 1902. A group of inventors formed with an idea to improve gear grinding, and Illinois Tool Works was born.

Today, Illinois Tool Works has a market capitalization of $70 billion and generates annual revenue of nearly $16 billion. Illinois Tool Works is composed of seven segments: Automotive, Food Equipment, Test & Measurement, Welding, Polymers & Fluids, Construction Products, and Specialty Products.

These segments have performed well against its peers, which has allowed Illinois Tool Works to achieve “best of breed” status in its industry.

Illinois Tool Works’ portfolio is concentrated in product segments that each hold above-average growth potential in their respective markets. The overarching strategic growth plan for Illinois Tool Works is to continuously reshape its business model, when necessary. The company frequently utilizes bolt-on acquisitions to expand its reach.

Growth Prospects

While 2020 was a very difficult year for the global economy, due to the coronavirus pandemic which weighed heavily on economic growth, Illinois Tool Works continued to generate steady profits. In 2021, the company continued to grow its earnings, and 2022 was even better. Final results for the fourth quarter have not been released yet, but based on the results that Illinois Tool Works generated during the first three quarters of the year, 2022 was most likely the strongest year in the company’s history.

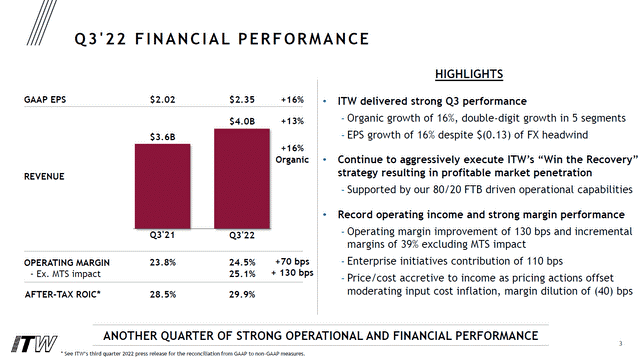

On October 25, 2022 Illinois Tool Works reported Q3 and first-nine-months results for the period ending September 30, 2022. For the third quarter, revenue came in at $4.0 billion, which was up by a compelling 13% compared to the previous year’s quarter. Positive results in Automotive, Polymers & Fluids and Construction Products was offset by declines in Food Equipment, Test & Measurement, Welding and Specialty Products.

Source: ITW presentation

Third-quarter net income totaled $2.35 per share, compared to $2.02 per share in the previous year’s quarter, which made for a compelling 16% increase year-over-year.

For the year, Illinois Tool Works has guided for revenue of $15.8 billion to $16.0 billion, which makes for a 9% to 10% increase year over year. Organic growth is seen at 11% to 12%, but currency rate movements are a headwind for Illinois Tool Works due to a strengthening US Dollar. Illinois Tool Works also guided for earnings-per-share to fall into a range of $9.45 to $9.55, which represents an attractive growth rate of 11% to 12% compared to what the company earned in fiscal 2021.

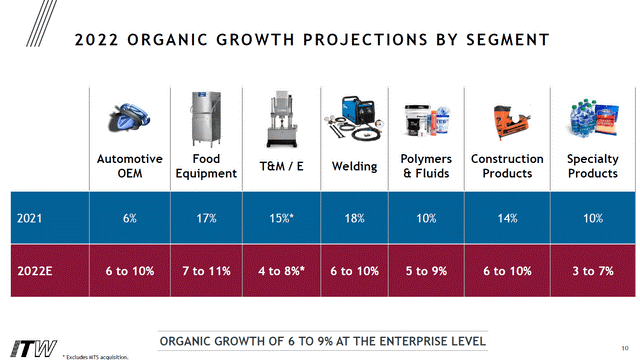

Management has forecasted that all of the company’s segments will show solid to attractive organic growth in 2022:

Source: ITW Presentation

This indicates that the business environment for the company as a whole was positive during 2022, which can be explained by the ongoing recovery from the COVID-induced economic slowdown.

In the future, Illinois Tool Works will grow its earnings-per-share via several drivers. First, ongoing organic business growth should add to profits overtime. On top of that, the company can grow via M&A, and efficiency and scale advantages could lead to some margin growth as the company grows. Last but not least, share repurchases will add to the company’s earnings-per-share as well. Overall, we expect 7% annual EPS growth over the next five years.

Competitive Advantages & Recession Performance

Illinois Tool Works has a significant competitive advantage. It possesses a wide economic “moat”, which refers to its ability to keep competition at bay. It does this with a massive intellectual property portfolio. Illinois Tool Works holds over 17,000 granted and pending patents.

Separately, another competitive advantage is Illinois Tool Works’ differentiated management strategy. The company has employed a management process called “80/20”. This is an operating system that is applied to every business line at Illinois Tool Works. The company focuses on its largest and best opportunities (the “80”) and seeks to eliminate costs or divest its less profitable operations (the “20”).

At the same time, Illinois Tool Works has a decentralized, entrepreneurial corporate culture. This also sets the company apart from the competition. Illinois Tool Works empowers its various businesses with significant flexibility, to customize their own approaches to serving customers in the best way possible.

One potential downside of Illinois Tool Works’ business model is that it is vulnerable to recessions. As an industrial manufacturer, Illinois Tool Works is reliant on a healthy global economy for growth.

Earnings-per-share performance during the Great Recession is below:

- 2007 earnings-per-share of $3.36

- 2008 earnings-per-share of $3.05 (9% decline)

- 2009 earnings-per-share of $1.93 (37% decline)

- 2010 earnings-per-share of $3.03 (57% increase)

That said, the company remained highly profitable during the Great Recession. This allowed it to continue increasing its dividend each year during the recession, even when earnings declined. And, thanks to its strong brand portfolio, the company recovered quickly. Earnings-per-share soared 57% in 2010. By 2011, earnings-per-share surpassed 2007 levels.

A similar pattern was seen in 2020 as the coronavirus pandemic caused an economic recession. Illinois Tool Works’ earnings-per-share declined in 2020, but the decline was manageable and the company continued to raise its dividend, while its earnings-per-share recovered quickly in 2021 and hit a new record high in that year.

Valuation & Expected Returns

Using the current share price of ~$230 and the midpoint for earnings guidance of $9.45 for the year, Illinois Tool Works trades for a price-to-earnings ratio of 24.3. Given the company’s cyclical nature, we feel that a target price-to-earnings ratio of 19 to 20 is appropriate. This is roughly in line with the company’s 10-year historical average.

As a result, Illinois Tool Works is currently overvalued. Returning to our target price-to-earnings ratio by 2028 would reduce annual returns by around 4% over this period of time. Aside from changes in the price-to-earnings multiple, future returns will be driven by earnings growth and dividends.

We expect 7% annual earnings growth over the next five years. In addition, Illinois Tool Works stock has a current dividend yield of 2.3%.

Total returns could consist of the following:

- 7% earnings growth

- -4% multiple reversion

- 2.3% dividend yield

Illinois Tool Works is expected to return around 5% per year through 2028. This isn’t too compelling, which is why we rate Illinois Tool Works a “hold” today, although the company’s ability to raise dividends through multiple recessions is impressive. The company now has 58 consecutive years of dividend growth after increasing its dividend again in 2022.

Final Thoughts

Illinois Tool Works is a high-quality company and an even better dividend growth stock. It has a strategic growth plan that is working well, and shareholders have been rewarded with rising dividends over 58 years.

The stock has a decent but not spectacular 2.3% dividend yield today. Shares are not attractively priced at the moment, which is why we do not deem Illinois Tool Works as a “buy” at current prices.

Illinois Tool Works is a classic example of a great company, but not a stock to buy right now. Despite its status as a Dividend Aristocrat and King, we suggest investors wait for a better entry point prior before purchasing shares of Illinois Tool Works.

Additionally, the following Sure Dividend databases contain the most reliable dividend growers in our investment universe:

If you’re looking for stocks with unique dividend characteristics, consider the following Sure Dividend databases:

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly:

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

{kind=link}