Updated on February 6th, 2023 by Quinn Mohammed

Essex Property Trust (ESS) isn’t necessarily a household name when it comes to dividend stocks, but the real estate investment trust, or REIT, has produced very impressive growth in the past two decades. The trust has managed to produce a soaring share price and rapidly increasing dividends since its IPO in 1994.

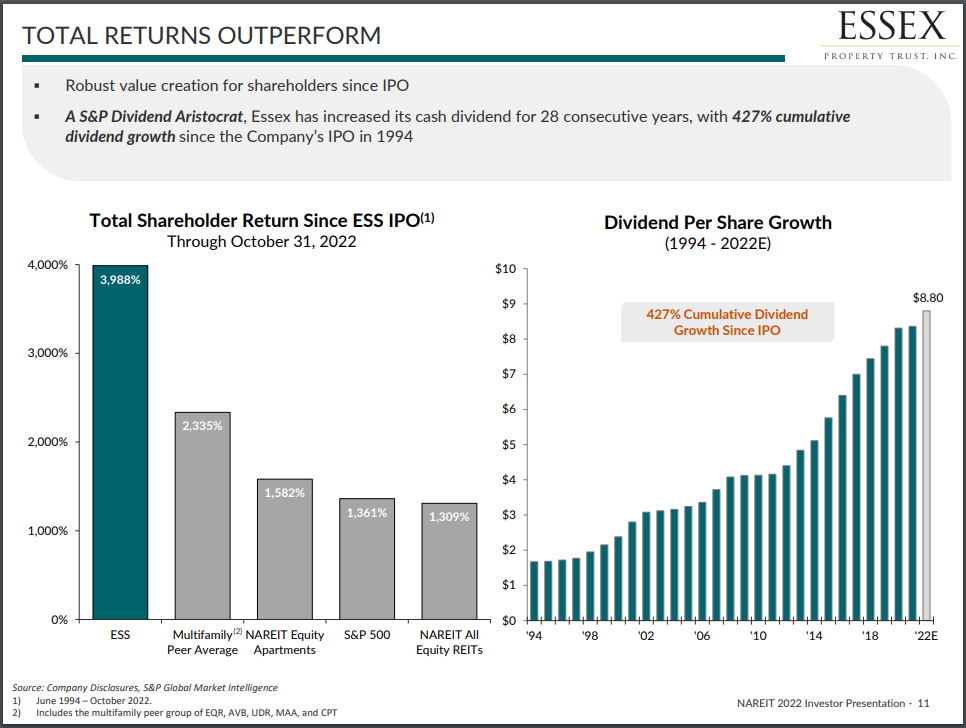

2022 marked the 28th consecutive year Essex boosted its dividend payment, making it a relatively new addition to the prestigious Dividend Aristocrats, a group of S&P 500 stocks with at least 25 consecutive years of dividend increases.

That list is now up to 68 companies that have proven to investors they can pay – and increase – their dividends in any economic climate. That characteristic is unusual for REITs, so Essex has set itself apart from the herd.

You can download an Excel spreadsheet of all 68 Dividend Aristocrats, including important financial metrics such as P/E ratios and dividend yields, by clicking the link below:

Essex faced some headwinds during the coronavirus pandemic of 2020, but the company has already made big strides in its ongoing recovery. The stock has a 3.8% yield, a leadership position in its core markets, and a long runway of growth up ahead.

Business Overview

Essex is a Real Estate Investment Trust, or REIT. It started in 1971 as a small real estate company and eventually went public in 1994. At that time, Essex had grown to 16 multifamily communities as a fully integrated REIT that acquires, develops, redevelops, and manages multifamily apartment communities located in supply-constrained markets.

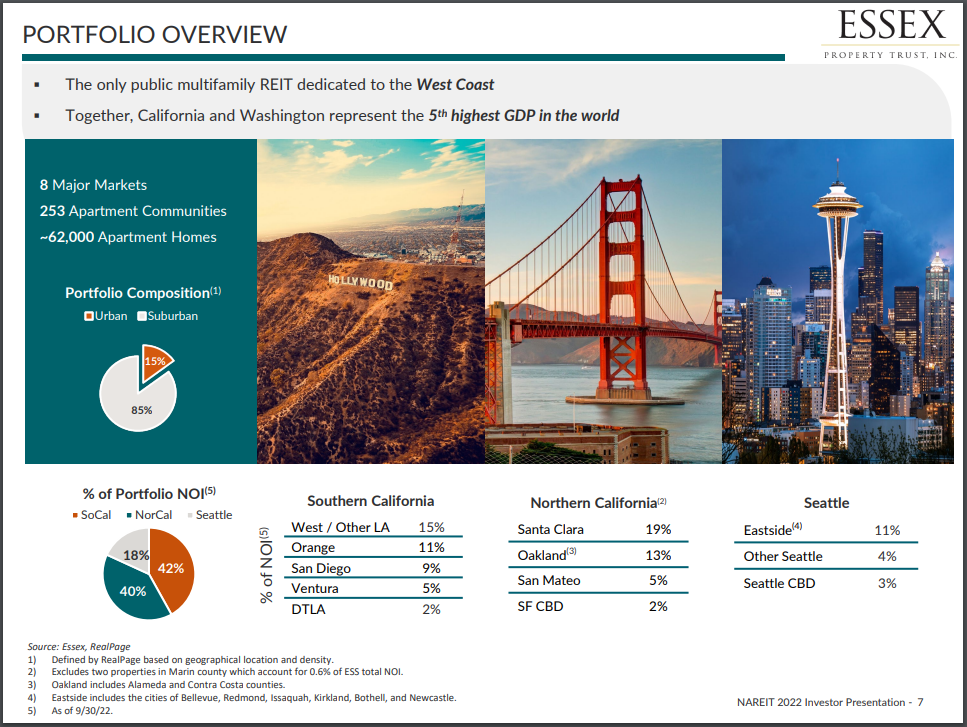

Today, Essex is concentrated on the West Coast of the U.S., including cities like Seattle and San Francisco.

Source: Investor Presentation

On October 26th, 2022, Essex reported third-quarter results. Core FFO-per-diluted share increased by 18.3% to $3.69. Same-property gross revenue increased by 12.7%, and same-property net operating income increased by 16.7% year-over-year.

Essex updated its 2022 core FFO per share guidance to $14.42 to $14.52, and we estimate the company can generate roughly $14.48 per share for the full year.

Growth Prospects

We see Essex producing 5.3% annual FFO-per-share growth in the next five years. Essex has reached the point where it is a huge player in the markets where it is present, so growth could be more difficult to come by.

However, we see some catalysts driving further improvement in FFO over time.

Source: Investor Presentation

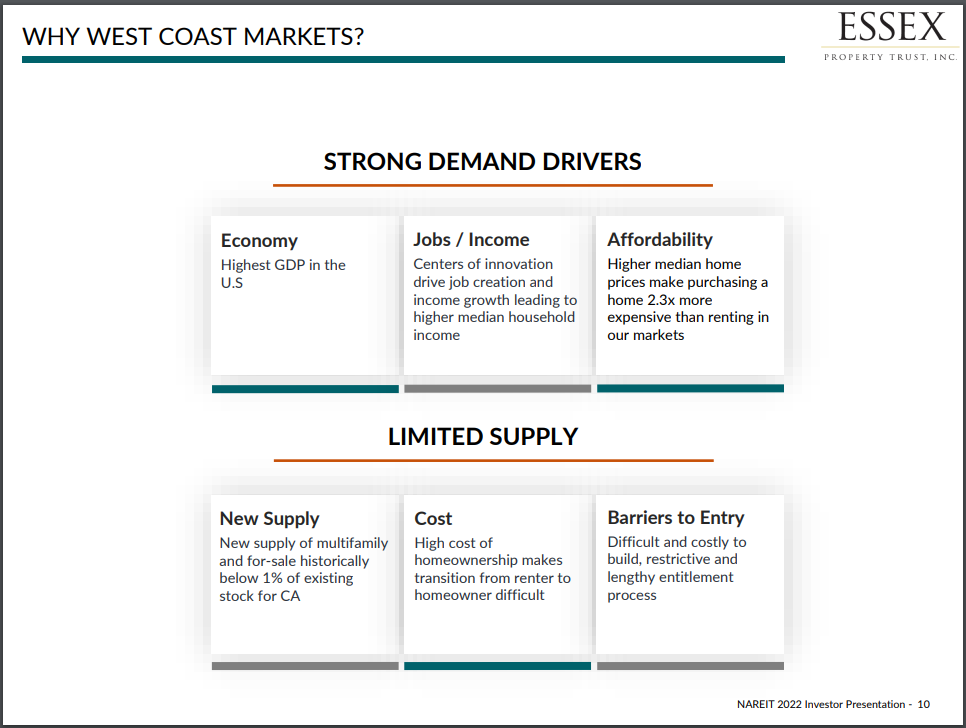

Essex concentrates on the markets on the West Coast because of favorable long-term rental prospects. That area has very high economic productivity and strong rates of job growth, both of which fuel the demand for housing supply. In addition, single-family residences are very expensive in these markets, making renting more attractive.

These markets have strong demand for rental units but also limited new supply as undeveloped land is limited, and construction is lengthy and expensive.

Essex is present in two markets with chronic housing shortage problems, which drives demand for its rental units over time. We think this tailwind will be modest but steady, adding to the trust’s FFO-per-share in the years to come via higher same-property revenue and NOI growth.

In addition, Essex has never been afraid to acquire or invest in future growth. Essex has a history of investing in properties in a variety of ways, but also in financial instruments like bonds and preferred stocks. Essex has, over time, invested its capital in the way it saw fit, irrespective of the method. We think this sets Essex up well for the long term, as it has produced solid results for the past 29 years.

Competitive Advantages & Recession Performance

Competitive advantages are difficult to come by for a REIT, given that so many competitors employ essentially identical business models. However, Essex has scale and size, unlike other apartment REITs, and a management team that is highly skilled in creating shareholder value through various methods.

The company also has a strong financial position, providing it a competitive advantage over its peers, who may be in worse financial shape. Essex has a solid BBB+ credit rating from Standard & Poor’s and currently has an interest coverage ratio of 567%, which provides a very large margin compared to their debt covenant requirement of 150% or higher.

Net debt to adjusted EBITDA is ~5.8X and has been coming down since 2020. Like many real estate businesses, Essex Property Trust uses a substantial but fair amount of leverage and maintains a relatively safe balance sheet. Its weighted average interest rate is under 3.2%, which is quite low, reflecting the trust’s strong credit metrics.

Interestingly, Essex performed very well during and after the Great Recession:

- 2007 FFO-per-share: $5.57

- 2008 FFO-per-share: $6.14

- 2009 FFO-per-share: $6.74

- 2010 FFO-per-share: $5.02

This speaks to the resilience of the markets where it is present, as 2020 and 2021 were the only years in the past decade where FFO-per-share declined. We see this recession resilience as highly favorable and adds to the stock’s attractiveness.

Valuation & Expected Returns

At roughly the midpoint of 2022 FFO-per-share guidance ($14.48 per share), Essex is trading for a multiple of 15.9. We see fair value at 18 times FFO-per-share, which introduces a 2.5% potential tailwind to annual total returns. As such, Essex is undervalued at present.

If we combine the favorable valuation, current dividend yield of 3.8%, and 5.3% forecasted FFO-per-share growth, we have total projected annual returns to shareholders of 11.1%.

Source: Investor Presentation

Essex has paid increasing dividends for 28 consecutive years. According to the company, it has cumulatively raised its dividend by 427% since its IPO.

For obvious reasons, dividend growth investors likely find this an attractive quality, and we expect Essex to continue to raise the payout each year for the foreseeable future.

Unfortunately, this alone is not enough to warrant a buy recommendation, as we are cautious about the valuation.

Final Thoughts

Essex has undoubtedly been a world-class REIT since it went public and began paying dividends over a quarter-century ago. The trust has favorable long-term demographics working in its favor and a management team keen to unlock shareholder value. We think Essex will produce moderate long-term growth and continue to increase its dividend each year.

Furthermore, shares are undervalued in our view, which means the stock’s total returns are expected to be excellent. The stock is appealing to investors looking for dividend safety and steady dividend growth over time.

If you are interested in finding more high-quality dividend growth stocks suitable for long-term investment, the following Sure Dividend databases will be useful:

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly:

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

{kind=link}