Vladimir Zakharov

(This article was co-produced with Hoya Capital Real Estate)

Introduction

I have a personal preference for actively managed equity funds outside of the Large- or Mid-Cap segments of the US stock market or in the Emerging Markets segment overseas. Index-based funds have their place, but having the freedom to not own a stock is appealing in those parts of the stock market where owning everything could place too much weight in underperforming companies. Of course, that means the investors are dependent on the manager’s skill or the “black box” they employ to pick and/or weight the fund’s holdings.

Last winter I came across a new entry in the Small-Cap Value segment that is actively managed that was doing better than the well-known index-based ETF and compared the two ETF here: DFSV Vs. VBR: New Small-Cap Value Beating Vanguard’s.

This article provides a 6-month update on the Dimensional US Small Cap Value ETF (NYSEARCA:DFSV), and compares the then-to-now allocation changes. The bottom line is the DFSV ETF is still ahead of the VBR ETF and continues to warrant a Buy rating. No strategy is foolproof and a risk analysis is provided in the closing section of this article.

In the comparison section of this article, I will include data from the Vanguard Small-Cap Value ETF (VBR), which is index-based, and the Vanguard Small-Cap ETF (VB), which covers both Value and Growth stocks in the Small-Cap segment. While DFSV is the better Value ETF, is Value where Small-Cap investors should be? A brief review is provided.

Dimensional US Small Cap Value ETF review

Seeking Alpha describes this ETF as:

The investment seeks to achieve long-term capital appreciation. The portfolio, using a market capitalization weighted approach, is designed to purchase a broad and diverse group of the readily marketable securities of U.S. small cap companies that the Advisor determines to be value stocks. The ETF version started in early 2022.

Source: seekingalpha.com DFSV

DFSV has $1.6b in AUM and comes with a 31bps cost to investors. The TTM Yield is 1.2%.

DFSV holdings review

While not tied to an index, DFSV does benchmark themselves against the Russell 2000 Value Index. Since the ETF started, its CAGR is over 900bps ahead!

According to the website, some Value measures used by the managers are:

- low relative price in relation to its book value.

- Price to cash flow or price to earnings ratios.

- High earnings from operations in relation to its book value or assets.

According to the ETF’s factsheet, DFSV uses reliable information in prices to target higher expected return securities within value stocks and is implemented with a daily flexible process to maintain consistent exposure through time.

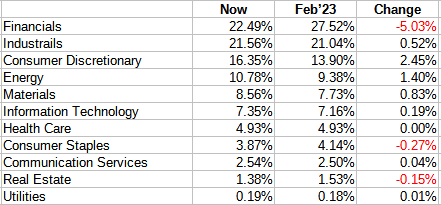

The review starts with how the sector allocations have changed since February.

dimensional.com; compiled by Author

While being reduced the most, Financials is still the sector with the highest allocation. Picking up most of that switch are Consumer Discretionary and Energy. All three changes have something in common, a belief that the economy is not going into a recession which would be a negative to all those sectors. Materials, the next biggest allocation bump, also meets that criterion. It should be noted that some of the allocation drop in Financials might not have been driven by the managers but by the banking crisis last March which was particularly hard on the smaller regional banks. The holdings report just prior to the banking crisis showed two important facts:

- None of the failed banks were in the portfolio

- The largest individual bank weight was under .6%

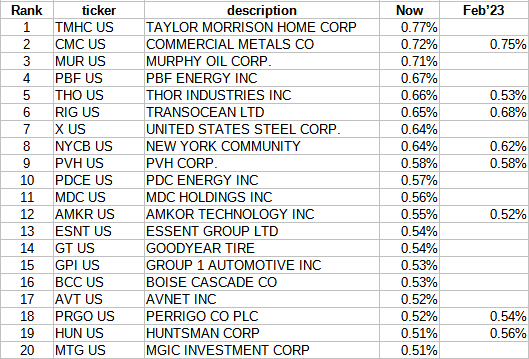

Top holdings

dimensional.com; compiled by Author

Holdings without a weight under Feb’23 means they were not in the Top 20 stocks at the time but without a complete holdings list from then, I could not determine if they were owned at the time or not. Commercial Metals (CMC) was the largest position at the time. It does show, either by price movement or holdings changes, how dynamic the holdings rankings moved over the past six months. In the case of the top holding, Taylor Morrison Home (TMHC), DFSV increased their holdings close to 50% since last winter, plus the price has climbed 56% YTD as optimism builds for that sector of the economy. With the ETF reporting a minuscule 4% turnover rate, I would say the initial stock selection process is working well. Beside saving costs, this means their selection process does not appear to be driven by one-off data events, which I also view as a positive for the process. Another major positive for investors is they don’t have to spend lots of time reviewing its holdings to spot recent transactions. All of those positives add to my confidence that DFSV earns my Buy rating.

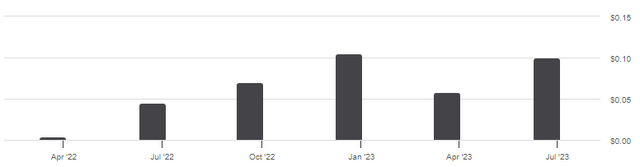

DFSV distribution review

seekingalpha.com DFSV DVDs

The ETF’s short history makes it hard to draw conclusions other than the low yield eliminates this ETF for income-seeking investors. With a yield of just 1.21%, investor owns this ETF for non-income goals.

Comparing ETFs

As mentioned above, I include the VBR ETF (SCV indexed) and the VB ETF( SC indexed) so investors see how actively managing SCV stocks affected the allocations.

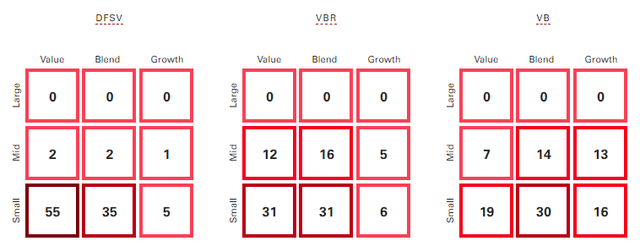

advisors.vanguard.com compare

What I see is that DFSV is truer to owning only Small-Cap stocks compared to both index-based ETFs, at least based on how Vanguard defines market-cap size. They are also purer holders of Value stocks compared to VBR. Both are critical to me when analyzing funds. If I am buying a SCV fund, I expect almost all the holdings to meet those two factors!

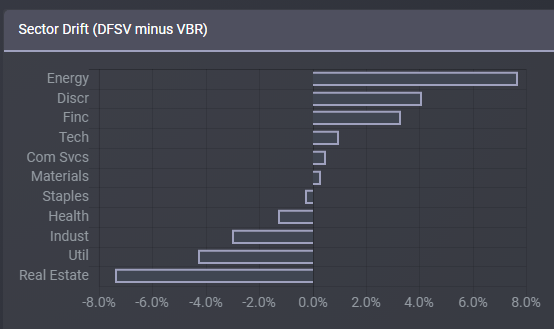

The next charts show how the sector allocations differ in weights for DFSV and the index-based VBR ETF.

ETFRC.com

The above drifts indicate how much active management affected sector allocations, which also reflects how CRSP and Dimensions might define Value plays differently. DFSV sees value in Energy and Consumer Discretionary stocks, little in terms of Utilities or Real Estate. As I see it, the value for the overweight sectors comes from their size if compared to their Large-Cap, well-known companies counterparts. Shaky economics depresses the smaller players in both sectors more so than the larger companies who can survive a downturn. As for the underweights, small Utilities face mounting climate change regulations with less assets to spread them across. Troubles across the Real Estate landscape for malls and commercial properties makes determining good from bad values in that sector harder with the unknowns that remain in the US related to the long-term effects of COVID.

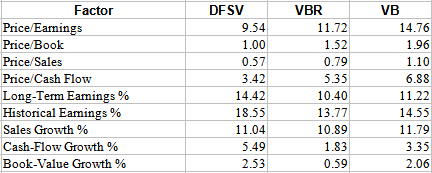

Next is a set of standard equity fund factors, all of which favor DFSV over both VBR and VB.

multiple pages; compiled by Author

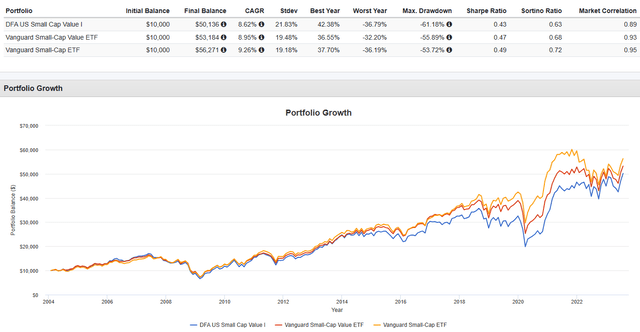

In order to gain more return data (2+ years), the next part will use the DFA U.S. Small Cap Value Portfolio Inst (DFSVX) in place of its ETF counterpart.

PortfolioVisualizer.com

Using the MF version of DFSV, we see it trailing both VBR and VB since 2004 but is on top when looking at the last five years. Since DFSV started in early 2022, its annualized CAGR is 8.74%, compared to only 4.55% for VBR and even less for VB at 2.99%. DFSV’s strategy is providing Alpha, as has the MF version in more recent times.

Portfolio strategy

Is owning Small-Cap Value stocks a winning strategy? The next chart shows how Value stocks have done since 1972, with Small-Cap coming out on top over most time periods shown.

PortfolioVisualizer.com

Within the Small-Cap segment, Value has been where to invest, not Growth.

Risk analysis

Some of these statements go beyond one’s Small-Cap Value allocation but highlights some of the risks investors need to consider.

- One major disadvantage for investors from active ETFs is secrecy. These ETFs do not go into detail how they select their stocks, which is totally understandable but leaves investors in the dark.

- The selection/weighting strategy itself starts to fail. Without strategy details, it cannot be analyzed for weaknesses.

- In order to generate excess Alpha, the managers might take exceptions to the process that then do not work out.

- The stocks in the investable universe become expensive compared to other market segments. This could cause underperformance compared to other segments or against other SCV ETFs.

- Investor interest, as reflected in fund flows, could force managers to sell or buy at times that do not benefit the ETF’s investors.

- Another unknown is how much influence the managers have building the portfolio. The more they more, the more investors need to worry about a change in the management team.

Final thoughts

Some readers wonder why an author gives a Buy rating on a ticker but doesn’t own it themself. While I like the DFSV ETF and give it a Buy rating as a potential Alpha producing ETF, I already had exposure to this part of the market with two Micro-Cap funds, which are actively managed, when I discovered this ETF. Except for total market-cap ETFs, I do not have other exposure to US stocks below Mid-Cap in size.

As expected for any portfolio strategy, not everyone, even within the Seeking Alpha community, is onboard for Small-Cap Value stocks. Read Small Cap Value Is Cursed, Large Cap Growth Is The Way Forward for a contrary viewpoint.

{kind=link}