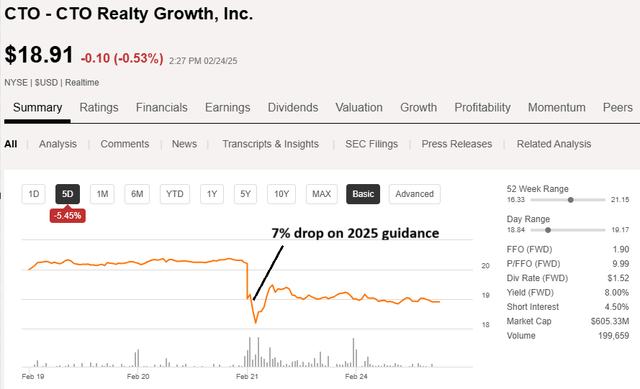

CTO Realty Development, Inc. (NYSE:CTO) has develop into extremely opportunistic because the inventory dropped 7% on wonderful earnings. This text will element why the drop occurred and present that as we dig in additional, the underlying information and fundamentals portend a powerful future for CTO.

The drop – headline quantity weak spot

Consensus estimates referred to as for CTO to earn $2.01 of AFFO/share in 2025.

S&P World Market Intelligence

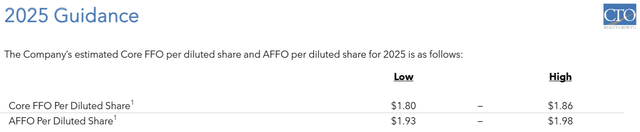

Regardless of sturdy earnings within the fourth quarter of 2024, CTO issued 2025 AFFO steering at $1.93 to $1.98.

CTO

That is a 6 cent miss on the midpoint and represents unfavorable development in 2025.

REITs are overwhelmingly traded on AFFO/share and AFFO/share development. As such, a miss of this magnitude was not acquired properly, with the inventory buying and selling down 7% on the report.

SA

The algorithms that may execute trades inside moments of a report hitting the information are wonderful at detecting beats or misses on headline numbers, so the value drop was speedy.

These algorithms, nonetheless, aren’t nearly as good at analyzing the underlying fundamentals.

The basics inform a unique story – one in all power and development.

Past the headlines

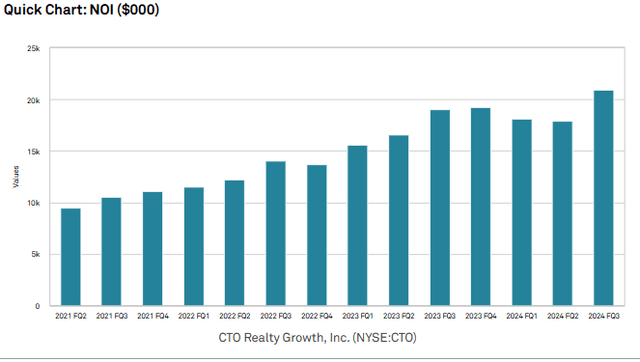

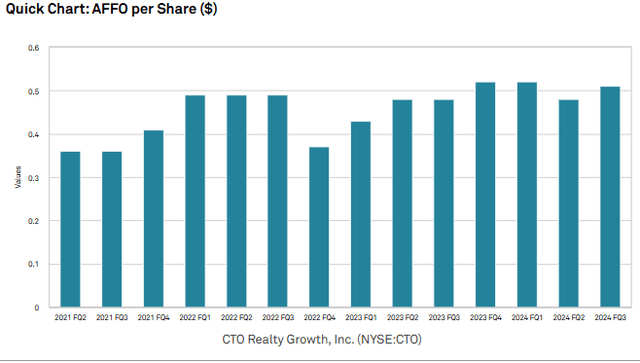

CTO has been rising properly, with will increase in web working revenue flowing by way of to stable AFFO/share features.

S&P World Market Intelligence

S&P World Market Intelligence

Whereas the charts above are up and to the best, there are some lumps resulting from timing.

Retail leases take some time to begin. Permits must be obtained. Shops must be reconfigured. Tenants want to maneuver in.

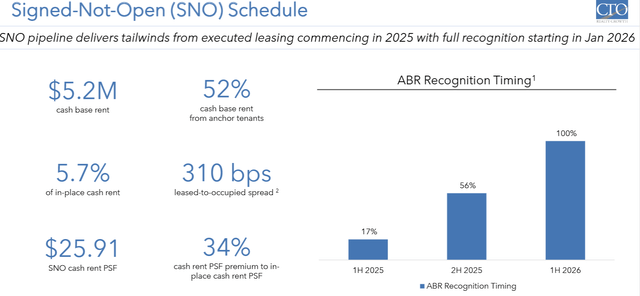

Thus, there’s typically a three-to-12-month hole between lease signing and graduation. CTO at present has $5.2 million annual base hire in contracts which are signed however not but open, in any other case generally known as SNO leases.

CTO

As there are 31.84 million shares excellent, SNO leases symbolize 16 cents per share in AFFO accretion. These 16 cents per share will begin to kick in all through 2025, however primarily hit earnings in 2026 and past. Since solely 17% of it’s within the first half of 2025, weighted common earnings for the 12 months will largely not embrace the SNO leases.

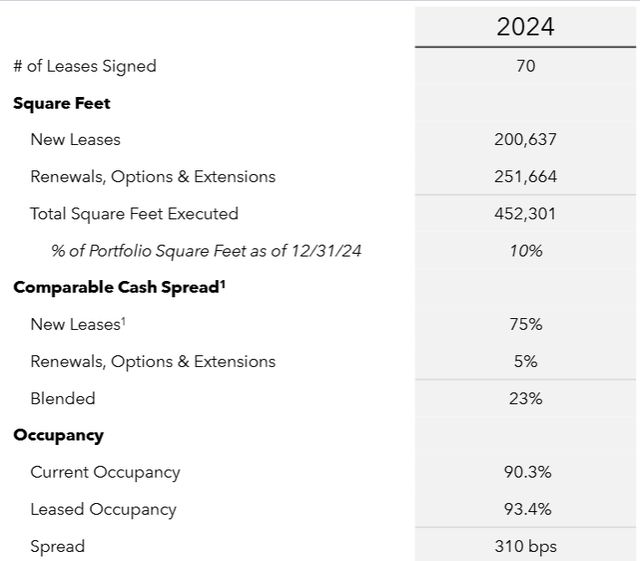

This SNO lease timing problem has been current with CTO for some time. It tends to roll. In 2024, many previously SNO leases commenced whereas new leases have been signed. Particularly, 70 leases have been signed in 2024 encompassing 452K sq. toes.

CTO

Notably, new leases have been signed at 75% greater hire than expiring leases. Blended leasing spreads have been pulled down by renewal choices which allowed tenants to increase their leases at a mean roll-up of simply 5%. General spreads got here in at 23%-plus.

Take into account that such renewal choices are a relic of a time when retail lease negotiations have been tenant-favored. Following the Monetary Disaster, retail actual property was oversupplied, so landlords simply wanted tenants to maintain their area open. This allowed tenants to barter favorable phrases corresponding to renewal choices at solely minor roll-ups.

At the moment, retail actual property is undersupplied, so negotiations are extra landlord-favored. Tenants usually don’t get renewal choices of this sort anymore. So going ahead, the next share of leases needs to be signed on the full markup to market rental charges.

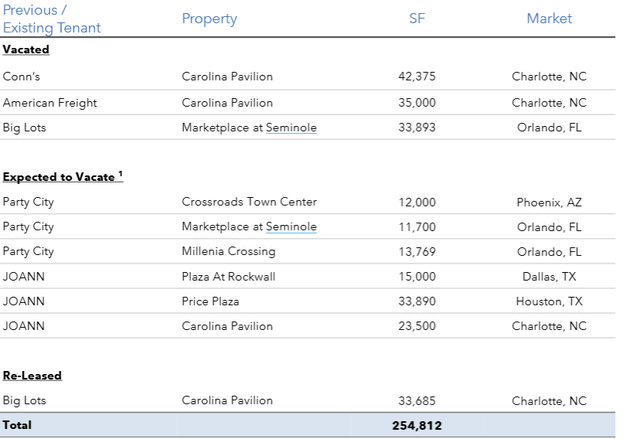

Past the standard SNO leasing, 2025 options one other substantial timing problem: the substitute of bankrupt tenants.

CTO misplaced the next tenants to chapter:

CTO

In a current article, we mentioned extensively how the chapter of retail tenants is definitely favorable for landlords within the current setting so long as the properties concerned are properly positioned.

The essential concept is that rental charges on present leases are properly beneath market charges such that chapter of the tenant affords a possibility to re-lease on the a lot greater market fee properly prematurely of the preliminary lease’s expiry.

John Albright, CTO’s CEO, mentioned the tenant bankruptcies on the 4Q24 earnings name:

“Transferring to not too long ago introduced retailer bankruptcies. Given that every one of our impacted leases have been for areas with meaningfully beneath market rents and embedded worth, we’ve been proactive in working to shortly regain them. Late within the fourth quarter, we efficiently labored by way of the court docket course of and regained 4 areas that have been occupied by our two Huge Tons, one Conn’s, and an American Freight. Moreover, we are actually engaged on agreements to get possession of our three Social gathering Metropolis areas and three JOANN areas early in 2025. Notably, we have already got LOIs or are negotiating leases with tenants for a majority of those areas.”

Moderately than making an attempt to drive the bankrupt tenants to honor the leases and pay hire, CTO is kicking them out as quick as they’ll to have the ability to lease the area to new tenants. New leases on this area are more likely to be about 50% greater hire per foot. Albright continues:

“Based mostly on present lease negotiations, we at present estimate that potential re-leasing unfold for these areas might be between 40% and 60%. Whereas we’re making speedy progress on leases with new tenants, it merely takes time for tenants to acquire permits, full their build-out and open. Accordingly, we count on hire from new tenants to begin throughout 2026.”

The previous leases of bankrupt tenants listed above paid $2.8 million ABR. That represents about 9 cents per share in misplaced income. Since these properties are to be vacant for almost all of 2025, this resulted within the gentle 2025 steering.

I feel the market is seeing this as misplaced income. I see it as a timing problem.

Based mostly on negotiations, CTO anticipates signing substitute tenants for these areas at $4.0-$4.5 million ABR. So, upon stabilization, CTO’s ABR needs to be about $1.2 to $1.7 million greater than it was with these tenants in place.

CTO steering assumes the properties are recaptured from tenants within the first quarter, so it is counting virtually no hire from former tenants of those properties in 2025. Steerage assumes new leases begin in 2026, so it’s assuming no hire from future tenants in 2025.

Stabilized run-rate AFFO/share (beats consensus by 13 cents)

There are two important parts of earnings that needs to be current in 2026 and past however not 2025.

- SNO leases – $5.2 million ABR.

- Alternative tenants for kicked-out tenants $4.25 million ABR.

Together, that means that stabilized ABR needs to be $9.45 million greater than 2025 ABR. That is 29 cents per share.

As such, we calculated CTO’s stabilized run fee AFFO/share at $2.24. That is properly above 2026 consensus estimates of $2.11.

The upper stabilized AFFO is enabled by CTO’s stellar leasing exercise in 2024 and the continued leasing exercise at market charges.

Why are market rents so excessive for CTO’s properties?

CTO’s buying facilities are in Atlanta, Phoenix, Dallas, Tampa, Daytona Seashore and different high-growth Sunbelt markets.

S&P World Market Intelligence

For different forms of actual property, these markets are excessive development and excessive provide.

Multifamily rents, for instance, are anticipated to return in roughly flat in 2025 for these markets as a result of the speedy job and inhabitants development is being balanced out by a big wave of newly constructed residences. The identical might be mentioned for industrial properties.

Procuring facilities profit from the identical demand drivers of inhabitants and job development, however have uniquely low provide. There was nearly no new web provide of buying facilities within the U.S. since 2009.

As such, the sector has greater demand with minimal provide development leading to greater occupancy and better rental charges.

CTO’s five-mile catchment areas common 203,000 folks and $143,000 common family revenue. Retailers need entry to densely populated affluence, so that they’re paying premiums to find in CTO’s facilities.

Prepared to attend

Given the timing of lease commencements, it’ll seemingly take till mid-2026 for CTO’s run fee AFFO/share to hit $2.24.

With a market value of $18.85 that is a particularly low cost valuation, and with an 8% dividend yield, I am comfortable to attend for the contracted ABR to kick in. Simply as CTO bought off when the headline AFFO got here in weak, I think the value will rise when AFFO grows on lease graduation.

")

{kind=link}