miniseries

Thesis

Coursera (NYSE:COUR) operates in an exciting market that could help improve the education of many people in countries where access to higher education is more difficult. Their business metrics of sales and margins have improved over the past year, but there is still no guidance on when they will be profitable. So I would stay on the sidelines for now and wait until they are at least free cash flow positive. Let me take you through their latest results.

Short Introduction

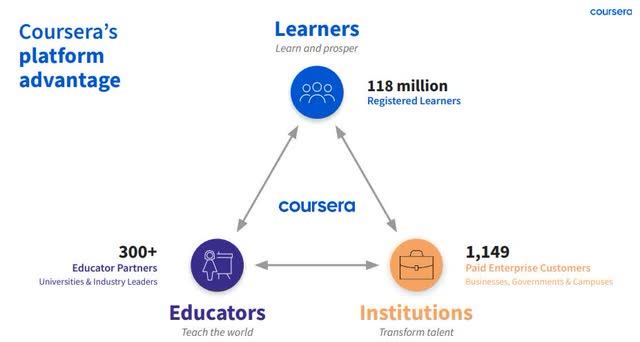

Coursera Investor Presentation

Coursera offers courses, certifications and degrees in collaboration with over 300 educator partners. They currently have 118 million registered learners, most of whom use the free courses because they operate a freemium model.

Analysis

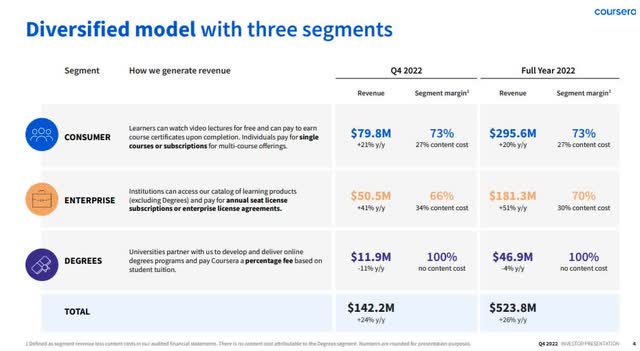

Coursera Investor Presentation

At first glance, the published results look good: 26% revenue growth in 2022 and 118 million registered learners. They also improved consumer margins from 69% in Q4 21 to 73% in Q2 22. Meanwhile, margins in the enterprise segment declined from 68% to 66% over the same period.

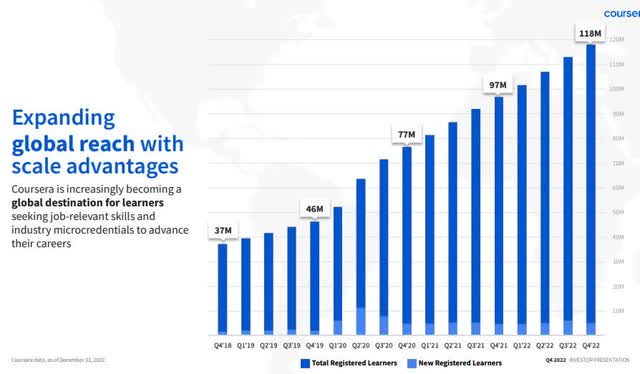

Coursera Investor Presentation

Before the pandemic, they were adding about 2 million users per quarter. In the last 9 quarters, they have added about 5 million users. This shows that they are still in a good position in terms of revenue growth and adding new users. However, the TAM for people who go on to higher education is likely to be much higher than this.

In the 10-K for the year 2022 they mentioned that their top 5 countries are: USA: 22.1 million users, India: 19 million users, Mexico: 5.7 million users, Brazil: 4.8 million users and China with 3.7 million users. There is so much more potential, especially in a country like India, and then there are countries like Indonesia, Pakistan or Nigeria with more than 100 million people, most of whom have no access to higher education at the moment.

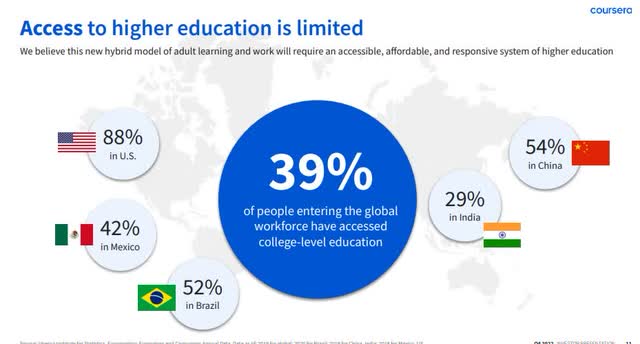

Coursera Investor Presentation

The more education that the people of these countries can get, the better it will be for the world as a whole. A company like Coursera is truly trying to improve the lives of many people. Better education can lift more people out of poverty.

Coursera Investors Presentation

In their last earnings call, they said they wanted to expand their catalogue of entry-level professional certificates because they saw a demand for it. And as you can see, they work with some of the world’s biggest and best-known companies. Asked about this Chat GPT / Open AI risk and what impact it will have, given the number of AI / data science / data analyst courses they have, they said that the bar for what humans can offer in these areas will likely rise, but with new technologies there will also be new skills that can be learned and taught.

The need to learn new things throughout life is also likely to increase. So this should be a positive aspect of future growth for education companies. Perhaps the education system will be transformed by AI if it can provide personalized feedback to learners and a way to have conversations about topics to help them understand them better. The development has been from passive learning on YouTube to active learning on Coursera with videos and questions on the topics. So the next step could be the personalized learning experience.

One thing they will be focusing on in the future is their Leadership Academy, because leadership is something that AI is unlikely to replace because it lacks the skills of human interaction and context.

Investors Presentation

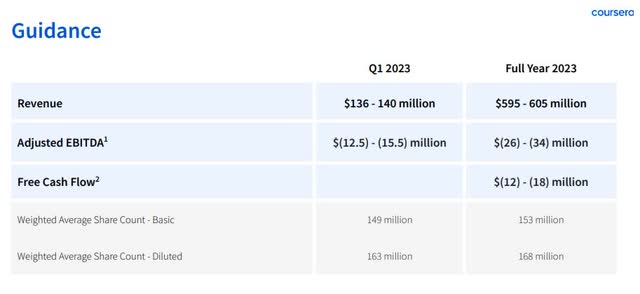

The guidance for 2023 is for sales growth in the range of 14%-15% and slightly negative free cash flow. A big problem is the share count, which is rising again. Shareholders are being diluted every year. Comparing SBC to revenue, SBC is 21.95% of revenue in 2021 and 21.15% of revenue in 2022.

Coursera 10-K 2022

In addition, revenues increased by only 26% in 2022, while total operating expenses increased by 30%. This is not very favorable for a company that has accumulated deficits of $661.1m as of 31 December 2022.

Coursera 10-K 2022

So even with the excessive use of SBC, they still have negative free cash flow and there is no clear path to profitability. Fortunately, they have a strong balance sheet with ~780m in cash and no debt. But depending on the cash burn over the next few quarters, this safety net could shrink quickly. But for now, they have half of their own market cap in cash. With a price-to-sales ratio of around 3, they are not cheap, but unlike some other unprofitable tech companies, this valuation is not excessive.

Competition

Comparing Coursera to Udemy (UDMY), we see that the latter has a more favorable price-to-sales ratio of ~2, but Coursera has clear advantages in terms of revenue growth and cash. In summary, the advantages on both sides are not clear enough to declare a clear winner at the moment. Bot are growing companies that need to become profitable.

Conclusion

As the online education business is new, we do not know if it will be profitable in the future and what the return on investment will be when it is more mature. So it is more of a speculative investment. It could be a market with no real competitive advantage, where competitors slowly erode each other’s margins. Or it could be a wonderful market with wonderful margins and really strong free cash flows. But I think it is too early to know for sure. So I would take a wait-and-see approach.

")

{kind=link}