JHVEPhoto/iStock Editorial via Getty Images

Investment Thesis

Simultaneously incorporating into your investment portfolio one company that offers a relatively attractive Dividend Yield and one that provides dividend growth brings investors the benefits of blending dividend income with dividend growth.

I have applied this strategy with the recent acquisitions of Nike (NYSE:NKE) and Exxon Mobil (NYSE:XOM). Including them in The Dividend Income Accelerator Portfolio has been strategically important.

While Exxon Mobil will primarily contribute to the generation of dividend income, Nike will contribute to the generation of dividend growth. Together, both companies not only combine dividend income and dividend growth, but they also help to enhance diversification while decreasing the portfolio’s sector specific concentration risk. Through their incorporations into The Dividend Income Accelerator Portfolio, the share of the Financials Sector compared to the overall portfolio has decreased from 33.07% to 30.56%.

Nike and Exxon Mobil’s strategic incorporations help us to decrease the overall risk level of The Dividend Income Accelerator Portfolio, and to raise the likelihood of achieving positive investment results.

I am convinced that both Nike and Exxon Mobil strongly align with The Dividend Income Accelerator’s investment approach. Both companies are well-positioned within their respective industries, are financially healthy (Nike exhibits an A1 and Exxon Mobil an Aa2 credit rating from Moody’s), have strong competitive advantages, and I consider both to be currently undervalued (both companies’ P/E [FWD] Ratios stand below their average from the past 5 years).

All these characteristics align with the investment approach of The Dividend Income Accelerator Portfolio and match with its strategy to invest with a margin of safety, putting capital preservation in first place.

Before I introduce you to the two selected companies in greater detail, I would like to reiterate the characteristics of The Dividend Income Accelerator Portfolio. Those who are already aware of the portfolio’s investment approach can skip the following chapter written in italics.

The Dividend Income Accelerator Portfolio

The Dividend Income Accelerator Portfolio’s objective is the generation of income via dividend payments, and to annually raise this sum. In addition to that, its goal is to attain an appealing Total Return when investing with a reduced risk level over the long term.

The Dividend Income Accelerator Portfolio’s reduced risk level will be reached due to the portfolio’s broad diversification over sectors and industries and the inclusion of companies with a low Beta Factor.

Below you can find the characteristics of The Dividend Income Accelerator Portfolio:

- Attractive Weighted Average Dividend Yield [TTM]

- Attractive Weighted Average Dividend Growth Rate [CAGR] 5 Year

- Relatively low Volatility

- Relatively low Risk-Level

- Attractive expected reward in the form of the expected compound annual rate of return

- Diversification over asset classes

- Diversification over sectors

- Diversification over industries

- Diversification over countries

- Buy-and-Hold suitability

Nike

Nike was founded in 1964 in Beaverton and is the world’s leading sporting goods manufacturer in terms of revenue and market capitalization. Currently, Nike’s market capitalization stands at $164.43B, while Adidas’ (OTCQX:ADDYY) is presently at $36.20B.

Nike possesses a multitude of competitive advantages, reinforcing my belief that it will hold its position as the leading sporting goods manufacturer in the coming years.

Nike’s notable competitive advantages include its strong brand image: according to Brand Finance, Nike is currently the 54th most valuable brand in the world. The company also benefits from long-term contracts with top-tier sports teams and athletes, its continuous focus on innovation, enormous financial health (evidenced by an A1 credit rating from Moody’s), its growing focus in direct sales, and a global distribution network.

Nike’s excellent position within its industry is reflected in the company’s high EBIT Margin [TTM] of 11.32%, which is 50.55% above the Sector Median (7.52%). It is further evidenced by a Return on Common Equity of 33.91%, which is 197.77% above the Sector Median of 7.52%.

Nike’s Current Valuation

At this moment in time, the company exhibits a P/E [FWD] Ratio of 29.83. Its P/E [FWD] Ratio currently lies 17.25% below its average from the past 5 years (36.04). This shows us that Nike is presently undervalued.

Nike’s undervaluation is also underscored by the company’s Price/Sales [FWD] Ratio of 3.19, which stands 19.05% below its 5 year average.

Nike’s Strong Growth Outlook

Different metrics indicate that the company is also an excellent pick in terms of growth: Nike has shown a Revenue Growth Rate [FWD] of 7.00%, which is 27.74% above the Sector Median.

In addition to that, it is worth mentioning that Nike’s EPS FWD Long Term Growth Rate [3-5Y CAGR] stands at 14.04%, which is 30.93% above the Sector Median, further underscoring my theory that the company’s growth outlook is positive.

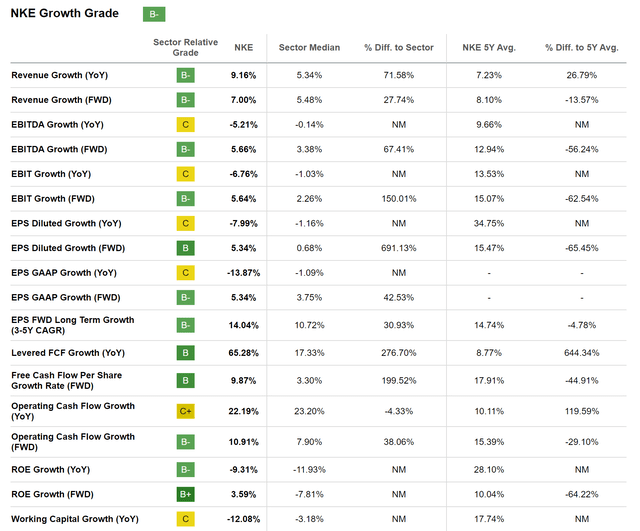

Below you can find the Seeking Alpha Growth Grade for Nike, which, once again, reaffirms the company’s promising growth prospects.

Source: Seeking Alpha

Nike’s Strength in Terms of Dividend Growth

Nike’s impressive dividend growth metrics strongly support my investment thesis, positioning the company as a key driver of dividend growth within The Dividend Income Accelerator Portfolio.

Nike has shown a Dividend Growth Rate 10Y [CAGR] of 12.32%, which is significantly above the Sector Median (8.14%).

In addition to that, the company has produced an Average Free Cash Flow Per Share Growth Rate [FWD] of 17.91%, which further underlines its potential of being a key driver of dividend growth within The Dividend Income Accelerator Portfolio.

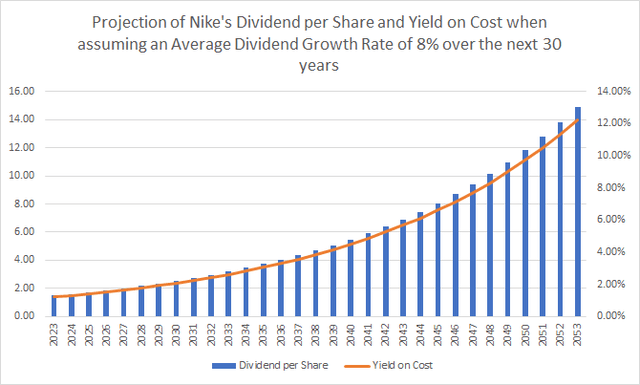

The graphic below illustrates a projection of Nike’s Dividend and Yield on Cost when assuming an Average Dividend Growth Rate of 8% for the next 30 years. The chart demonstrates that investors could potentially achieve a Yield on Cost of 2.63% in 2033, 5.67% in 2043, and 12.25% in 2053.

Source: The Author

Why I Have Chosen Nike Over Its Competitors

Nike’s excellent position within its industry is reflected in its higher EBIT Margin [TTM] (11.76%) when compared to Adidas (0.62%), Under Armour (NYSE:UA, NYSE:UAA) (5.09%) and Puma (OTCPK:PMMAF) (6.43%).

Nike also exhibits a significantly higher Return on Common Equity (36.03%) compared to any of these competitors: Adidas exhibits a Return on Common Equity of -2.29%, Under Armour’s is 5.09%, and Puma’s is 6.43%.

In addition to that, it can be highlighted that Nike has a higher Revenue Growth Rate [FWD] (6.06%) in comparison to Adidas (3.32%), and Under Armour (1.75%), reflecting the company’s superiority in terms of growth.

Nike’s 24M Beta Factor of 1.15 further indicates that an investment comes attached to a lower risk level when compared to Adidas (24M Beta Factor of 1.34), Under Armour (1.55), and Puma (1.25).

All of these metrics underline my belief that Nike provides investors with the most attractive risk/reward profile, and with the highest likelihood of achieving successful investment outcomes in comparison to its competitors. This strengthens my belief that the company is the most adequate choice for The Dividend Income Accelerator Portfolio among its peer group.

Exxon Mobil

Exxon Mobil operates in the exploration and production of crude oil and natural gas. The company operates through the following segments:

- Upstream

- Energy Products

- Chemical Products

- and Specialty Products

Exxon Mobil’s Current Valuation

Exxon Mobil currently presents a P/E Non-GAAP [FWD] Ratio of 11.01, which is 31.12% below its average from the past 5 years. This indicates that the company is presently undervalued. Exxon Mobil’s undervaluation is further evidenced by a Price/Cash Flow [FWD] Ratio of 7.32, which is below its average from the past 5 years (7.88).

Exxon Mobil’s High Free Cash Flow Yield

It can further be highlighted that Exxon Mobil presently exhibits a high Free Cash Flow Yield [TTM] of 9.15%, indicating that the company provides investors with an attractive risk/reward profile. This high Free Cash Flow Yield suggests that Exxon Mobil’s current share price is grounded in realistic growth expectations, providing investors with a significant margin of safety.

Exxon Mobil’s Dividend Yield

At this moment in time, the company provides its shareholders with a Dividend Yield [FWD] of 3.75%. A relatively low Payout Ratio of 34.87% further indicates that Exxon Mobil has the potential to not only be an attractive pick in terms of dividend income, but also in terms of dividend growth. This theory is further underlined by its 10 Year Dividend Growth Rate [CAGR] of 4.11%.

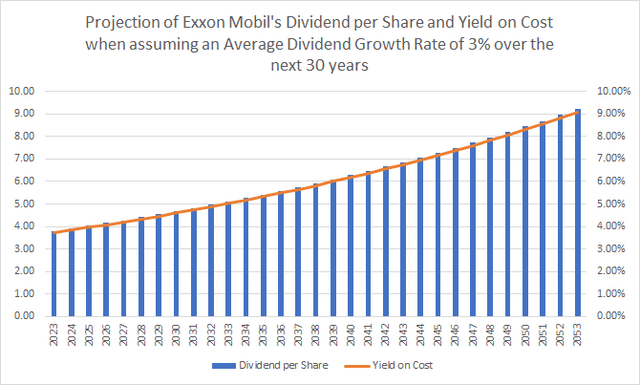

A Projection of Exxon Mobil’s Dividend and Yield on Cost

Below you can find a projection of Exxon Mobil’s Dividend and Yield on Cost when assuming an Average Dividend Growth Rate of 3% for the following 30 years. This projection illustrates a potential Yield on Cost of 5.02% by 2033, increasing to 6.75% by 2043, and to 9.07% by 2053.

Source: The Author

Why I Have Chosen Exxon Mobil Over Its Competitors

One of the principal reasons for choosing Exxon Mobil over its competitor Chevron (NYSE:CVX) is that The Dividend Income Accelerator Portfolio is already invested in SCHD (NYSEARCA:SCHD), which holds a significant stake in Chevron (the company currently accounts for 3.94% of SCHD).

Selecting Exxon Mobil over Chevron for The Dividend Income Accelerator Portfolio contributes to maintaining a reduced company-specific concentration risk, therewith increasing the likelihood of positive investment outcomes.

However, this is not the only reason for which Exxon Mobil could be the superior choice in comparison to Chevron: Exxon Mobil has the slightly lower 24M Beta Factor of 0.51 (when compared to Chevron’s 24M Beta Factor of 0.57). This indicates that Exxon Mobil is the choice with the slightly lower risk level, which, once again, can be seen as an indicator of an elevated probability for positive investment outcomes.

In addition to that, I see Exxon Mobil as being slightly superior when it comes to Profitability, which is reflected in the company’s slightly higher Return on Common Equity of 21.17% (compared to Chevron’s 15.68%).

Why Nike and Exxon Mobil Align With the Investment Approach of The Dividend Income Accelerator Portfolio

- Both Nike and Exxon Mobil have significant competitive advantages and are well-positioned within their industries. This aligns with the investment approach of The Dividend Income Accelerator Portfolio to invest in the top players of its respective industries.

- Furthermore, it can be highlighted that Exxon Mobil primarily contributes to the income generation of The Dividend Income Accelerator Portfolio, while Nike will predominantly contribute to the portfolio’s dividend growth. Both companies are important strategic acquisitions for the successful implementation of The Dividend Income Accelerator Portfolio, combining dividend income with dividend growth.

- Both Nike and Exxon Mobil are financially healthy, reflected by their A1 and Aa2 credit rating from Moody’s respectively. This aligns with the portfolio’s investment approach of prioritizing capital preservation.

- Nike and Exxon Mobil’s financial health is further underscored by their Return on Common Equities of 33.91% and 21.17% respectively.

- I consider both companies to currently be undervalued, aligning with the investment approach of The Dividend Income Accelerator Portfolio to invest with a margin of safety, once again, prioritizing capital preservation for investors.

- Both companies have a positive growth outlook, reflected by their Revenue Growth Rates [FWD] of 7.00% (Nike) and 7.32% (Exxon Mobil). This matches the investment approach of The Dividend Income Accelerator Portfolio to invest in companies with attractive growth prospects.

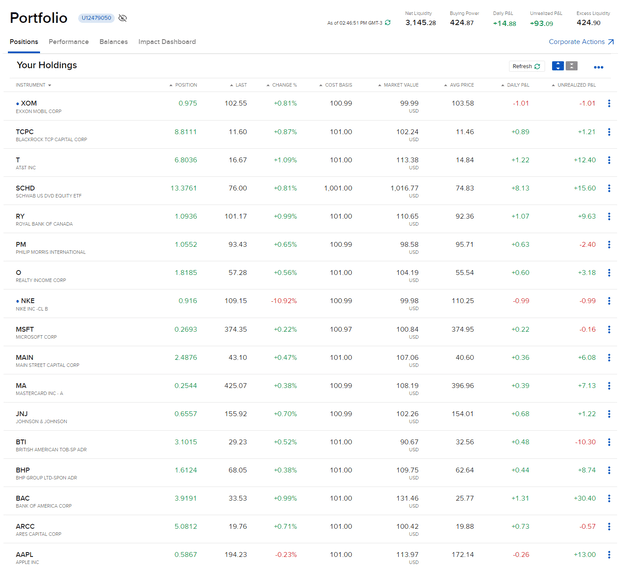

Investor Benefits of The Dividend Income Accelerator Portfolio After Investing $100 in Nike and $100 in Exxon Mobil

Below you can find an overview of the current composition of The Dividend Income Accelerator Portfolio after incorporating both Nike and Exxon Mobil.

Source: Interactive Brokers

After the incorporation of Nike and Exxon Mobil, we have further increased the portfolio’s diversification and therewith reduced its risk level.

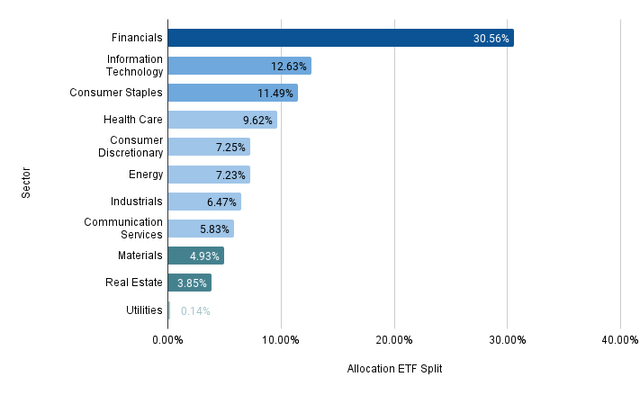

The graphic below illustrates the current sector allocation of The Dividend Income Accelerator Portfolio when allocating SCHD across the companies and sectors it is invested in.

Source: The Author, data from Seeking Alpha and Morningstar

By adding Nike and Exxon Mobile, the share of the Financials Sector compared to the overall portfolio has decreased from 33.07% to 30.56%. This indicates that we have managed to increase the diversification while reducing the sector specific concentration risk of The Dividend Income Accelerator Portfolio. The Consumer Discretionary Sector has increased from 3.77% to 7.25% and the Energy Sector has increased from 3.51% to 7.23%.

After the inclusion of Nike and Exxon Mobil, it can be highlighted that the Weighted Average Dividend Yield [TTM] of the portfolio has only slightly decreased from 4.56% to 4.40%. The portfolio’s 5 Year Weighted Average Dividend Growth Rate [CAGR] has slightly decreased from 9.12% to 8.95%. Despite this decrease, The Dividend Income Accelerator Portfolio continues to provide investors with an attractive mix of dividend income and dividend growth.

Conclusion

I consider both Nike and Exxon Mobil to be important strategic acquisitions for The Dividend Income Accelerator Portfolio.

With their inclusion, we successfully balance dividend income and dividend growth within The Dividend Income Accelerator Portfolio. In addition to that, both companies boast notable competitive advantages and have strong market positions within their respective industries. Moreover, both are financially healthy (evidenced by Nike and Exxon Mobil’s A1 and Aa2 credit rating from Moody’s), and I consider both companies to be undervalued (their current P/E [FWD] Ratio is below their 5 Year Average).

In addition to that, with the inclusion of Nike and Exxon Mobil, we have managed to increase the level of diversification of The Dividend Income Accelerator Portfolio. This is the case since we have managed to reduce the share of the Financials Sector compared to the overall portfolio from 33.07% to 30.56%.

Through their incorporation, the proportion of The Consumer Discretionary Sector and the Energy Sector have increased from 3.77% to 7.25% and from 3.51% to 7.23% respectively, once again, indicating an increased level of diversification for the overall portfolio.

Due to Nike and Exxon Mobil’s notable competitive advantages, their attractive Valuations, and their relatively low investment risk levels, I am convinced that both companies boast an attractive risk/reward profile. This makes them compelling choices for investors in general and for The Dividend Income Accelerator Portfolio in particular.

Exxon Mobil’s Free Cash Flow Yield [TTM] of 9.15% reinforces my view that the company offers investors a favorable balance of risk and reward.

Given Nike and Exxon Mobil’s attractive risk/reward profile, I am convinced that both are important strategic acquisitions, positioned to significantly contribute to The Dividend Income Accelerator Portfolio’s aim of achieving an attractive Total Return with a high likelihood.

In addition to that, I consider the companies’ dividends to be relatively safe, evidenced by Nike and Exxon Mobil’s Payout Ratios of 41.98% and 34.87% respectively. Their relatively low Payout Ratios indicate that the probability of a dividend cut is relatively low for both, further underscoring their low risk level.

In January 2024, I will add additional companies to The Dividend Income Accelerator Portfolio, which will help us to elevate the portfolio’s diversification further and reduce its risk-level. Doing so will allow us to continuously maintain a high probability of successful investment results for those who implement the investment approach of The Dividend Income Accelerator Portfolio.

Author’s Note: Thank you for reading! I would appreciate hearing your opinion on my selection of Nike and Exxon Mobil as the latest acquisitions for The Dividend Income Accelerator Portfolio. Feel free to share any thoughts about The Dividend Income Accelerator Portfolio or to share any suggestion of companies that would fit into its investment approach! I wish you and your families all the best for 2024!

")

{kind=link}